Cryptocurrency ramblings

Roth IRA Cryptocurrency: Your 2026 Tax-Free Guide

Crypto has moved from fringe speculation into mainstream portfolio conversations, and retirement planning hasn’t kept up. Cryptocurrency adoption among Americans rose from 5% in 2019 to an estimated 16% in 2023, a more than threefold increase, according to Retirement Living’s bitcoin IRA statistics overview. That matters because the typical crypto holder and the typical IRA holder still look nothing alike. One is generally younger and more comfortable with risk. The other is older and more conservative.

That mismatch created a blind spot. Many investors understand Bitcoin, Ethereum, DeFi, Layer 2 networks, smart contracts, and tokenized assets far better than they understand the retirement wrapper that can hold them. In practice, roth ira cryptocurrency strategy sits at the intersection of tax law, custody design, and crypto market behavior. Get it right, and the structure can be powerful. Get it wrong, and the operational mistakes can be brutal.

This guide takes the practitioner view for 2026. It covers the upside, the setup process, and the part many providers soften or skip entirely: custody, insurance gaps, and what happens when your “secure platform” runs into real-world stress.

Table of Contents

- The Crypto Retirement Wave Is Here

- What Is a Crypto Roth IRA Really

- The Ultimate Tax Advantage for Crypto Investors

- Choosing Your Path Crypto IRA Custodians Explained

- How to Set Up Your Roth IRA for Cryptocurrency

- The Hidden Risks Beyond Market Volatility

- Best Practices and Future Outlook for 2026

- Frequently Asked Questions

The Crypto Retirement Wave Is Here

Crypto ownership moved from the fringe into the mainstream in just a few years. That shift is why roth ira cryptocurrency is now a serious retirement-planning question, not a niche tax strategy for early adopters.

You can see the change in investor behavior. A younger cohort that already follows Bitcoin cycles, Ethereum upgrades, Layer 2 growth, tokenization, and AI-linked blockchain projects is no longer debating whether crypto belongs in a portfolio. The main question is where it belongs, and under what rules.

I have seen the same pattern repeatedly. Investors start by focusing on upside and tax-free growth. Then they realize the harder part is not picking Bitcoin or Ethereum. It is choosing a structure that does not trap them in high fees, weak custody terms, limited trading windows, or vague insurance language.

That last point gets skipped too often.

In a taxable account, every sale can create tax friction. Inside a Roth IRA, the tax treatment can be far better for long holding periods. But the retirement wrapper introduces a different set of risks. You are adding custodians, administrators, platform rules, and operational constraints between you and the asset. For crypto investors who are used to self-custody, that trade-off is bigger than it looks on a provider homepage.

Strong bull markets make this decision more urgent. When momentum returns, investors often revisit the drivers behind the move before reallocating fresh capital. If you want context on current market strength, Coiner Blog’s analysis of why Bitcoin is rising is a useful companion.

Why this matters now

The retirement conversation is changing because crypto is no longer isolated from the rest of digital finance. Bitcoin now sits beside stablecoins, tokenized real-world assets, DeFi infrastructure, and smart contract networks that many investors view as part of a broader capital stack.

Crypto inside a Roth IRA makes the most sense when you treat it as long-duration capital, not as casino chips with a tax shelter attached.

Traditional retirement advice still treats digital assets as a side bet. That framing misses what has changed in 2026. The serious question is not whether crypto is legitimate enough to discuss in retirement planning. The serious question is whether the account structure, custodian setup, and insurance protections are strong enough to justify putting long-term wealth there. That is where smart investors need to be skeptical.

What Is a Crypto Roth IRA Really

The phrase crypto Roth IRA sounds like a special government-approved account type. It isn’t.

It is a structure, not a special IRS account

A crypto Roth IRA is typically a self-directed Roth IRA that allows cryptocurrency exposure through a custodian that supports digital assets. The important point is structural. You’re still dealing with Roth IRA rules, but the account holds crypto through an approved framework rather than through your personal wallet.

According to Cardinal Point Wealth’s explanation of Roth IRA crypto structure and restrictions, gains from buying and selling cryptocurrencies such as Bitcoin or Ethereum inside a self-directed Roth IRA are not subject to annual capital-gains realization, but the account must be held through an IRS-compliant custodian and the assets can’t be personally possessed.

That last part changes how many crypto investors think. In regular crypto investing, self-custody is often the gold standard. In an IRA, self-custody can create compliance problems because the account has to maintain separation from your personal control.

Why the custody detail matters

The cleanest analogy is this: the Roth IRA is the tax wrapper, and the custodian is the legal gatekeeper. You direct the investment choices, but you don’t personally take the coins into your own MetaMask, Phantom, Ledger, or exchange account.

Here’s the practical difference:

| Account type | Who controls custody | Tax treatment on trades | Personal wallet allowed |

|---|---|---|---|

| Taxable exchange account | You and the exchange relationship | Taxable events can arise when you sell or exchange | Yes |

| Self-directed Roth IRA with crypto | IRA custodian and approved platform structure | Trades inside the IRA are not subject to annual capital-gains realization | No |

That’s why roth ira cryptocurrency planning is less about “how do I buy BTC in retirement?” and more about “how do I hold digital assets without breaking IRA rules?”

Practical rule: If a provider makes it sound like you can blur the line between your personal crypto activity and your IRA crypto activity, slow down. The line needs to stay sharp.

This is also why some investors end up preferring simpler exposure, while others want direct spot holdings inside a specialized setup. The tax benefits can be compelling, but the compliance mechanics are less forgiving than a normal exchange account.

The Ultimate Tax Advantage for Crypto Investors

Crypto is one of the few asset classes where the Roth wrapper can feel almost custom-built. The reason is simple. High-volatility assets can create enormous gains, and the tax treatment on those gains matters.

Why volatile assets fit the Roth wrapper

The most cited real-world illustration of Roth power is not crypto at all. Peter Thiel’s Roth IRA grew from less than $2,000 in 1999 to over $5 billion by 2021, and that structure could have saved him roughly $1 billion in taxes, based on Swan Bitcoin’s discussion of Roth compounding and high-growth assets.

Crypto is a different asset class, but the same tax logic applies. The same source notes that Bitcoin moved from $15,480 in November 2022 to $126,230 in October 2025, an approximately 715% gain. That’s exactly the kind of move that makes investors care about where the asset sits.

If a high-upside asset compounds inside a Roth IRA and withdrawals are qualified, the structure can preserve far more of the long-term upside than a taxable account.

What tax drag looks like outside the IRA

A taxable crypto account creates friction in places many investors underestimate:

- Active rebalancing: Selling one asset to buy another can trigger tax consequences.

- Cycle management: Taking profits during euphoric phases and rotating back in later can add reporting complexity.

- Altcoin churn: Moving between narratives like Layer 2 tokens, AI-related coins, DeFi governance tokens, and infrastructure plays can create a messy tax trail.

Inside the Roth wrapper, the appeal is cleaner. You can rebalance, reduce exposure, or rotate between approved assets without annual capital-gains realization at the account level.

That doesn’t mean roth ira cryptocurrency is automatically the best home for every strategy. It’s usually strongest when your thesis is long-term appreciation, not endless short-term experimentation.

The tax shelter becomes more valuable as volatility rises and holding periods lengthen.

For investors who think in multi-cycle terms, that’s the core case. If you believe Bitcoin, Ethereum, select Web3 infrastructure, or tokenized financial rails will appreciate over a long horizon, the Roth structure gives you a rare chance to separate the thesis from recurring tax drag.

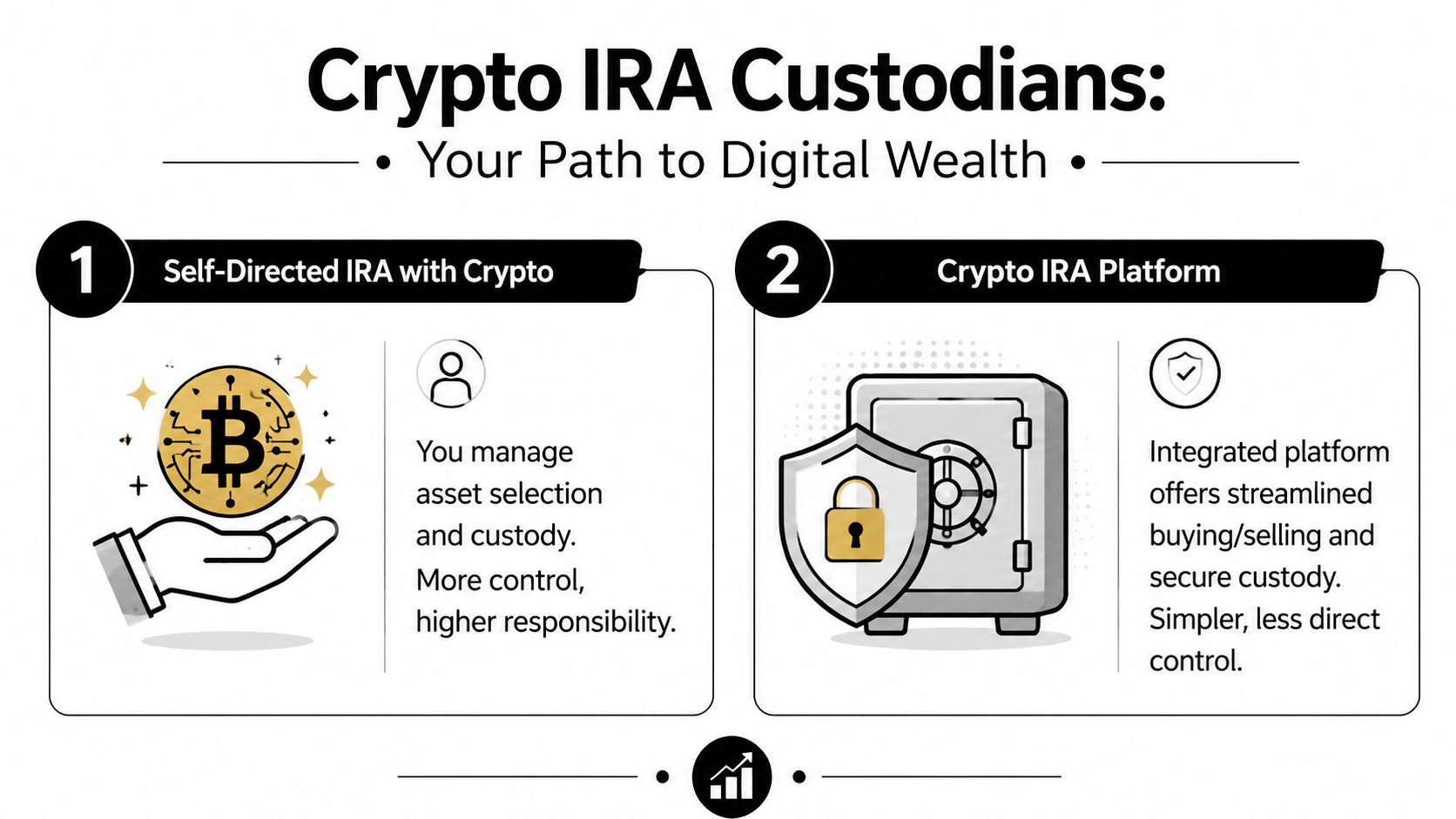

Choosing Your Path Crypto IRA Custodians Explained

Provider choice shapes almost everything. Fees, execution, available coins, onboarding friction, and withdrawal mechanics all start here.

Crypto IRA platforms

This is the more efficient route. You open an account with a provider that combines custodial administration with an integrated trading interface. The experience feels closer to a brokerage product, even though the underlying legal structure is still retirement-account driven.

The upside is convenience. You usually get a simpler dashboard, a predefined list of supported assets, and fewer moving parts. For investors who want BTC, ETH, maybe a handful of large-cap coins, this route is often the easiest way to get compliant exposure.

The downside is constraint. Coin selection may be narrow. Trading windows, spread behavior, and withdrawal procedures can be less flexible than what experienced crypto users expect. If you’re used to native DeFi, onchain staking, or fast-moving altcoin rotations, many platforms will feel restrictive.

If you’re also thinking about the cash movement side of the setup, Coiner Blog’s guide to crypto-friendly banks helps clarify what tends to work smoothly with crypto-adjacent funding workflows.

More open self-directed structures

Some investors want broader control. They’re willing to accept more paperwork, more responsibility, and more operational friction in exchange for a wider asset universe or more bespoke setup options.

These structures can be attractive if you care a lot about flexibility. But flexibility cuts both ways. More moving parts means more opportunities for errors in custody, reporting, execution, or prohibited transactions. That’s not a theoretical concern. In retirement accounts, process mistakes can matter as much as market mistakes.

How to compare providers without getting sold to

Don’t start with marketing language. Start with a checklist.

- Asset menu: Are you buying only major spot assets, or do you need broader token exposure?

- Custody model: Does the provider explain who holds keys, how storage works, and how assets are segregated?

- Fee stack: Look for trading fees, monthly fees, custody fees, transfer fees, and spread behavior.

- Distribution mechanics: Can the account distribute only cash, or are there in-kind options?

- Reporting quality: Statements and transaction records need to be usable, not decorative.

If a provider can’t explain custody, pricing, and transfer procedures in plain English, they haven’t earned your retirement capital.

A lot of roth ira cryptocurrency decisions come down to this trade-off. Simplicity works well for many people. Control appeals to experienced investors. The right choice is the one whose operational burden you can manage for years.

How to Set Up Your Roth IRA for Cryptocurrency

Opening the account is usually easier than understanding the rules behind it. The process looks straightforward, but the details matter.

Step 1 and Step 2 choose and open the account

First, pick the custodian model that fits your tolerance for complexity. Investors who want a cleaner experience often prefer an integrated platform. Investors who want a more customized structure usually spend more time on due diligence before they open anything.

Then complete the account application, identity verification, beneficiary setup, and any linked banking instructions. Expect KYC and AML checks. Crypto IRAs are retirement accounts, so providers aren’t casual about onboarding.

A lot of beginners confuse wallet setup with account setup. They are not the same thing. If you want a refresher on consumer wallet mechanics, Coiner Blog’s explainer on what Phantom Wallet is is useful context, but your IRA assets don’t work like personal wallet assets.

Step 3 fund it the compliant way

Funding usually happens through a contribution, a rollover, or a transfer from another retirement account. The exact method depends on your tax situation and your source account.

One rule is mandatory. According to iTrustCapital’s explanation of crypto Roth IRA mechanics, spot-listed cryptocurrencies in these accounts can only be acquired with cash inside the IRA account. Direct deposits from external wallets or exchanges are prohibited under IRS guidelines to avoid prohibited-transaction issues related to personal use or self-dealing. The custodian reports holdings and transactions to the IRS on forms such as Form 5498-SA.

That’s why “I already own BTC, I’ll just move it into the Roth” doesn’t work the way many people assume it should.

Funding mistakes that trip people up

- Mixing personal and IRA assets: Personal wallet coins and IRA coins must stay separate.

- Rushing a rollover: Retirement transfers need clean documentation and approved handling.

- Ignoring platform restrictions: Some providers support only certain transfer pathways or approved assets.

After you understand the compliance side, this walkthrough helps visualize the basic flow:

Step 4 place the trade and document everything

Once the account is funded in cash, you place the crypto purchase through the provider’s approved trading path. Keep confirmations, monthly statements, and transfer records. If your strategy includes Bitcoin, Ethereum, or a limited set of approved digital assets, simplicity usually wins.

For roth ira cryptocurrency investors, the best operational habit is boring documentation. Keep every approval, every transfer record, and every account statement. When retirement structures meet crypto infrastructure, clean records are part of risk management.

The Hidden Risks Beyond Market Volatility

Most crypto education stops at price swings. That’s not enough for retirement accounts.

Custody risk is the part most investors underestimate

Traditional brokerage IRAs train investors to assume a familiar protection model. Crypto IRAs don’t sit on equally settled ground. As noted in Binance Square’s discussion of crypto IRA custodial risk and insurance gaps, cryptocurrency held in self-directed IRAs operates in a regulatory gray zone, unlike traditional brokerage IRAs with FDIC or SIPC protection. The same source states that no standard insurance coverage extends to smart contract failures, exchange hacks, or custody provider insolvency, which leaves investors with limited legal recourse.

That changes the risk profile in a big way. If the custodian, exchange partner, or related service layer fails, your problem isn’t just market drawdown. Your problem may be access, recovery, and legal ambiguity.

Many polished provider landing pages often appear thin in this regard. “Cold storage” sounds reassuring, but it doesn’t answer the hard questions. Neither does vague mention of insurance.

Questions to ask before you fund anything

Ask these in writing, and don’t settle for broad reassurance:

- What exactly is insured: Theft, internal fraud, external hack, operational error, or only a narrow subset?

- Who is the legal custodian: A named entity matters more than a branded front end.

- Are assets segregated or pooled: Recovery outcomes may differ depending on the setup.

- What happens in insolvency: How are client assets treated if the provider or partner fails?

- What is the incident process: Who contacts you, what freezes, and how do distributions or transfers work under stress?

For investors tracking the deeper security side of digital assets, Coiner Blog’s look at the future of cryptography adds useful context around how security assumptions in crypto continue to evolve.

Don’t confuse “institutional-grade” marketing with a clearly documented recovery framework.

There’s also a strategic implication here. The more substantial the allocation, the less acceptable vague custody answers become. A small speculative sleeve can tolerate some uncertainty. A major retirement allocation should not.

Best Practices and Future Outlook for 2026

The best roth ira cryptocurrency plans are usually the least dramatic. They’re deliberate, documented, and sized so the investor can stay rational through ugly market conditions.

What works for beginners

For many, a simple playbook works better than a clever one:

- Start with liquid majors: Bitcoin and Ethereum are easier to evaluate than thin, fast-cycling altcoins.

- Prefer understandable custody: If the provider’s operating model feels opaque, keep looking.

- Treat it as a sleeve: Your retirement plan should still stand without crypto carrying the whole outcome.

- Rebalance with discipline: Don’t let one narrative take over the account just because the market got loud.

Advanced investors may want exposure to infrastructure tied to Web3, tokenomics, or scaling. Even then, retirement wrappers reward selectivity. A Roth isn’t the best place to chase every new token launch.

Where the market may be heading

The next phase of crypto retirement investing likely won’t be limited to BTC and ETH. Investors are already watching tokenization of real-world assets, more mature Layer 2 ecosystems, and compliant forms of DeFi participation. AI-linked crypto infrastructure is also attracting attention as onchain data, automation, and smart contract execution converge.

That doesn’t mean every trend belongs in your IRA. It means the menu is expanding, and the due diligence burden is growing with it.

For readers mapping broader market scenarios, Coiner Blog’s outlook on crypto predictions for 2025 is a helpful way to pressure-test your longer-term view.

A Roth IRA works best when you use it to hold convictions that may need years to play out.

In 2026, that’s the frame. Use the structure for patient upside, not constant experimentation.

Frequently Asked Questions

What are the 2026 contribution limits for a Roth IRA

IRS contribution limits and Roth IRA income phase-outs can change year to year. For 2026, confirm the current numbers before you fund the account.

That matters even more with crypto because many investors mix annual contributions with rollovers, transfers, and conversions, then assume the rules are interchangeable. They are not. A regular contribution is subject to annual limits and income rules. A rollover or trustee-to-trustee transfer follows a different set of procedures, and a Roth conversion can create a tax bill in the year you do it. I have seen investors get the investment thesis right and still create avoidable paperwork problems by funding the account the wrong way.

Are staking rewards or airdrops inside my IRA taxable

This area still needs careful review. Tax treatment for staking rewards, airdrops, and other crypto income inside an IRA is not as straightforward as the marketing pages make it sound.

The first question is often operational, not tax-related. Many crypto IRA custodians do not support staking or airdrops at all.

That can feel restrictive, but it also limits one of the least discussed risks in this market: activity the platform advertises, but the custody and reporting setup cannot handle cleanly. If a provider offers yield inside an IRA, ask who controls the keys, how rewards are booked, whether assets are rehypothecated, and what insurance covers. Insurance language is often narrow. It may cover theft from specific systems, not losses tied to protocol failure, validator mistakes, third-party insolvency, or administrative errors. For retirement money, those details matter more than the headline APY.

Can I take a loan from my crypto Roth IRA

IRAs generally do not allow participant loans. If you need short-term access to cash, a crypto Roth IRA is a poor source of liquidity.

The bigger risk is prohibited use. You cannot treat IRA crypto like coins in a personal wallet, move it around for convenience, or use it for your own benefit without risking serious tax consequences. That line is easy to cross by accident if you are used to self-custody outside retirement accounts.

Keep IRA crypto in the category it belongs in: long-term retirement capital, held with a custodian you have vetted for security, reporting quality, and insurance limitations. If there is a real chance you will need the money early, hold that portion outside the IRA.