Cryptocurrency ramblings

Decentralized Finance Protocols: An In-Depth Guide for 2026

$84.53 billion in capital sat inside decentralized finance protocols as of 2026, after a cycle that once pushed the sector to nearly $180 billion in late 2021, according to Fensory's DeFi market analysis. That number changes how you should think about DeFi. This isn't a fringe experiment anymore. It's an operating financial layer built from smart contracts, mostly on blockchain networks such as Ethereum, with growing spillover into the broader Web3 stack and Layer 2 ecosystems.

The interesting part isn't only the scale. It's the design trade-off. Decentralized finance protocols replace many human intermediaries with code, but they also remove many of the safety nets people assume are there. You gain open access, composability, and transparent execution. You also take on a very different kind of operational risk.

That mix of innovation and irreversibility is what makes DeFi worth understanding properly.

Table of Contents

- What Are Decentralized Finance Protocols

- The Core Building Blocks of DeFi

- Major DeFi Protocol Examples in Action

- How to Interact with DeFi Protocols

- Navigating Security and Regulatory Risks

- How to Evaluate a DeFi Protocol

- The Future of Decentralized Finance

What Are Decentralized Finance Protocols

Decentralized finance protocols are blockchain applications that deliver financial functions such as trading, lending, borrowing, collateral management, and synthetic asset issuance through smart contracts rather than through banks, brokers, or centralized exchanges.

A useful way to frame them is by comparing who enforces the rules. In traditional finance, institutions enforce balances, approvals, margin calls, and settlement behind closed systems. In DeFi, smart contracts enforce those same rules on a public blockchain. If the contract says a loan is undercollateralized, liquidation can happen automatically. If a swap meets the pool's pricing formula, it clears without a human dealer stepping in.

That shift matters because it changes both access and failure modes. A user with a wallet can often reach these systems without opening an account or asking an intermediary for approval first. But if funds are sent to the wrong address, a contract contains a bug, or collateral is liquidated during a sharp market move, there is often no help desk with the power to reverse the outcome.

If you want a technical refresher on the mechanism behind that automation, this guide to how smart contracts work covers the logic layer DeFi depends on.

Code instead of counterparties

The clearest difference between DeFi and ordinary fintech is where trust sits. A polished fintech app may feel modern, but a company still controls the ledger, user permissions, and transaction processing in the background. In DeFi, the ledger is shared across the network, and the application logic is published as code.

That changes several things at once:

- Access is usually open: Anyone with a compatible wallet and supported assets can interact with the protocol.

- Execution is visible: Transactions and contract state changes are recorded onchain and can be inspected publicly.

- Products can connect to each other: One protocol can use another protocol's liquidity, collateral, or price data.

- Users carry more responsibility: Self-custody gives control over assets, but mistakes and security failures are often irreversible.

Practical rule: DeFi doesn't remove trust. It relocates trust from institutions and staff to code, oracle systems, governance processes, and your own operational habits.

The main protocol layers people use

Most users do not interact with DeFi as one unified system. They use a specific tool for a specific job. A decentralized exchange handles token swaps. A lending protocol lets them post collateral and borrow against it. A derivatives platform gives them synthetic exposure to an asset they do not hold directly. Yield products often sit on top of multiple protocols and route funds wherever the strategy dictates.

That breadth is part of why DeFi can sound more abstract than it is. The better way to view it is as financial infrastructure broken into software modules. Each module performs a narrow task, and the modules can be combined. That modularity is powerful, but it also creates chain reactions. If a price oracle fails, a lending market can misprice collateral. If liquidity disappears, a strategy employing borrowed funds can unwind fast.

The case for DeFi is practical, not ideological. It offers continuous market access, programmable settlement, and financial products that can interoperate without a central operator coordinating every step.

The trade-off is just as practical. Openness does not guarantee fairness, inclusion, or safety. Fees can still be too high for small users, governance can drift toward insiders, and many protocols still depend on offchain data, front-end operators, and concentrated token holders. DeFi expands access in some ways, but it also asks users to absorb risks that traditional finance usually hides behind institutions, insurance, and legal recourse.

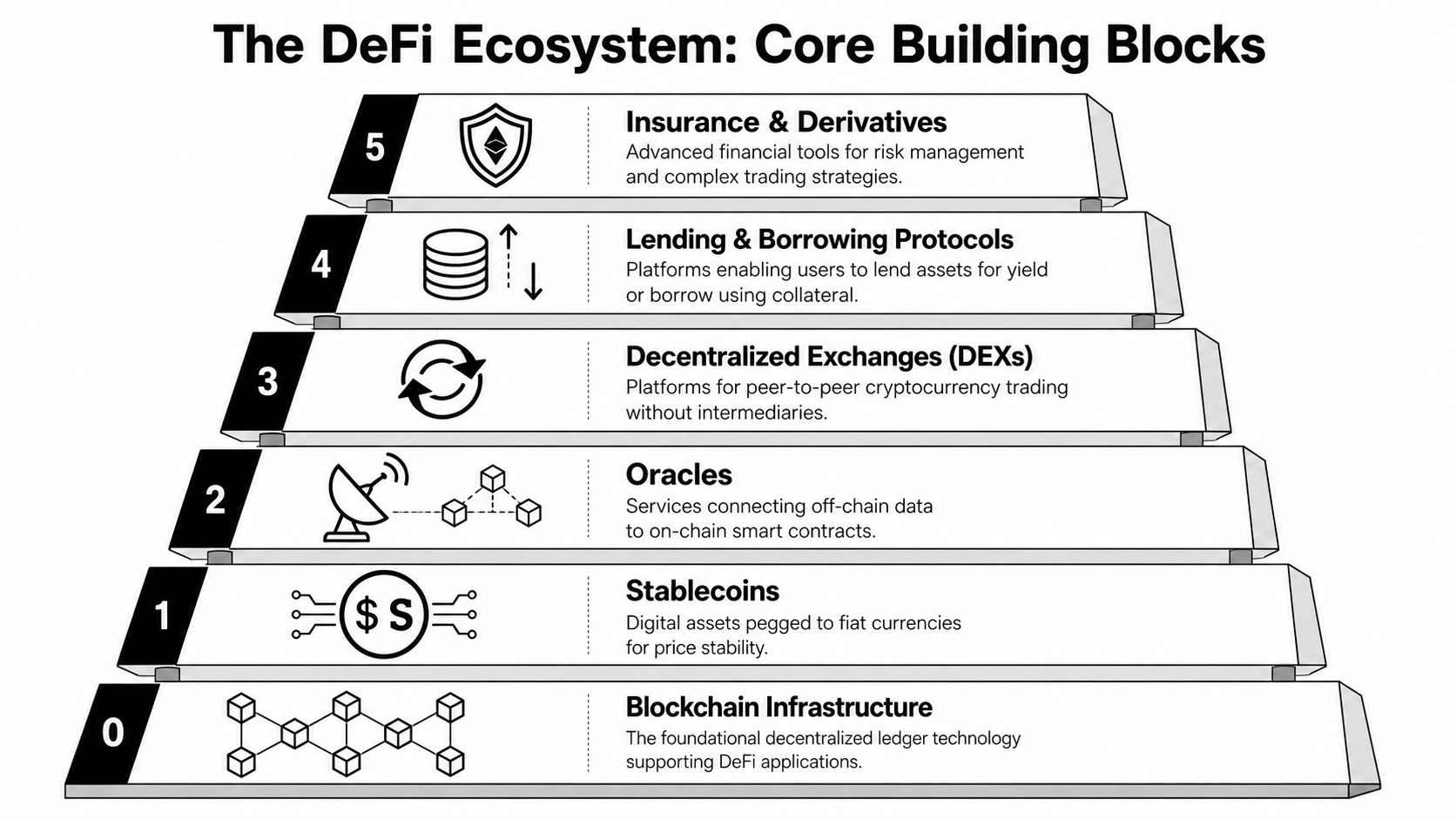

The Core Building Blocks of DeFi

The DeFi stack works because several components fit together like machine parts. If one part fails, the rest can wobble. If the pieces are designed well, they form a financial system that runs continuously and settles in public.

Code instead of counterparties

The foundation is the blockchain itself. Ethereum remains the reference point for many DeFi applications because it made smart contracts widely usable, but many protocols also operate across other chains and Layer 2 networks to reduce fees and improve throughput. If you need a primer on how the logic layer works, Coiner Blog's guide to what a smart contract is is a useful technical refresher.

On top of that base, protocols usually rely on a few recurring building blocks:

- Stablecoins: These act as the accounting units of DeFi. Traders price assets in them, lenders denominate positions in them, and liquidity pools often pair volatile assets against them.

- Oracles: Smart contracts can't natively “see” outside data. Oracle systems deliver price feeds and other external inputs to onchain applications.

- Liquidity mechanisms: These power token swaps and market making without a traditional order-book operator.

- Collateral systems: These enforce lending rules, margin requirements, and liquidation logic.

The main protocol layers people actually use

A helpful way to organize DeFi is by protocol family. According to research on DeFi protocol taxonomies, DeFi protocols are broadly categorized into liquidity pools such as Uniswap, pegged and synthetic tokens such as MakerDAO's DAI, and aggregator protocols such as Yearn Finance. Each category carries distinct risk profiles.

Those labels sound academic, but the practical functions are intuitive.

| Building block | Plain-language analogy | What it does | Typical risk |

|---|---|---|---|

| Liquidity pools | Robotic currency kiosk | Lets users swap one token for another | Smart contract bugs, liquidity concentration |

| Pegged or synthetic tokens | Digital wrapper or mirrored asset | Creates stable or reference-based onchain assets | Oracle dependence, collateral stress |

| Aggregators | Automated portfolio router | Moves funds across strategies or venues | Strategy complexity, hidden dependency chains |

Liquidity pools are often where users first encounter DeFi. Instead of matching buyers and sellers directly, they use pooled assets and algorithmic pricing. Synthetic and pegged token systems do a different job. They create onchain units that aim to track another asset or maintain a peg, which is central for stable-value settlement and borrowing. Aggregators sit one layer higher and optimize between protocols, which is convenient for users but adds another layer of code and governance risk.

A good mental model is this: DeFi isn't one product. It's a financial operating system made from specialized modules, each solving a narrow task and inheriting the risks of the layers beneath it.

One reason DeFi feels powerful to experienced users is composability. A stablecoin can be deposited into a lending market. The receipt token from that deposit might then be used elsewhere. An aggregator may route capital through several protocols before the user even notices. That modularity is efficient, but it also means failures can propagate.

Major DeFi Protocol Examples in Action

Abstract categories only get you so far. It helps to look at recognizable protocols and see what role each one plays inside the machine.

Uniswap and the logic of automated markets

Uniswap is the canonical example of a decentralized exchange built on liquidity pools. Instead of asking a centralized platform to hold customer balances and match trades internally, Uniswap lets users trade against pooled reserves inside smart contracts. That model is the basis of the AMM, or automated market maker.

If you want a deeper dive into the mechanics behind that design, Coiner Blog's explainer on automated market makers is a good companion. The key idea is simple. A trader doesn't need a direct human counterparty at the exact moment of execution. The pool itself acts as the trading venue.

For ordinary users, that means token swaps can happen quickly and permissionlessly. For liquidity providers, it means they can deposit assets into a pool and earn fees when others trade. The trade-off is economic rather than procedural. Pool providers take on risks that don't exist in a standard savings account, including exposure to relative price movements between the paired assets.

Aave and the mechanics of onchain credit

Aave shows what lending looks like when software enforces the rules. Users deposit assets into pools, borrowers post collateral, and smart contracts track whether each position remains solvent. There's no loan officer and no negotiation. The terms are encoded.

Research on DeFi lending mechanics notes that protocols like Aave enforce solvency through overcollateralization, requiring users to lock assets worth more than the amount they borrow. If the collateral value drops below the required threshold, smart contracts trigger liquidations automatically, which removes traditional counterparty credit risk but introduces liquidation risk for the borrower, as discussed in this analysis of DeFi lending design.

A separate line of research also explains that borrowing rates in lending protocols such as Aave V2 rise with asset utilization. When a large share of available liquidity is already borrowed, rates move higher to discourage pool depletion and compensate lenders, according to the BIS working paper on DeFi lending rates. That's one of the more elegant parts of DeFi. Pricing isn't negotiated manually. The market logic responds automatically to pool conditions.

Where oracle networks fit

Oracle networks sit off to the side until something breaks. Then everyone remembers how essential they are. Lending markets need reliable price feeds to decide whether positions are healthy. Synthetic assets need external reference data. Many other smart contracts depend on fresh offchain information to function correctly.

Chainlink is the best-known example in this category. Its role is less visible to end users than a DEX or lending app, but it's foundational. If the oracle layer fails, many of the higher-level applications start making bad decisions.

The same pattern appears in flash loans, another protocol primitive often discussed in security circles. Research notes that AAVE flash loans charge a fixed 0.09% per transaction, while dYdX has offered flash loans with no fees, as described in this study of flash loan mechanisms. The feature is technically clever. It also shows how specialized and composable DeFi has become.

Comparison of Major DeFi Protocol Types

| Protocol Category | Primary Function | Leading Example | Core Concept |

|---|---|---|---|

| Decentralized exchange | Token swapping | Uniswap | Liquidity pools replace centralized order matching |

| Lending protocol | Collateralized borrowing and lending | Aave | Overcollateralization and automated liquidations |

| Oracle network | External data delivery | Chainlink | Offchain data feeds trigger onchain decisions |

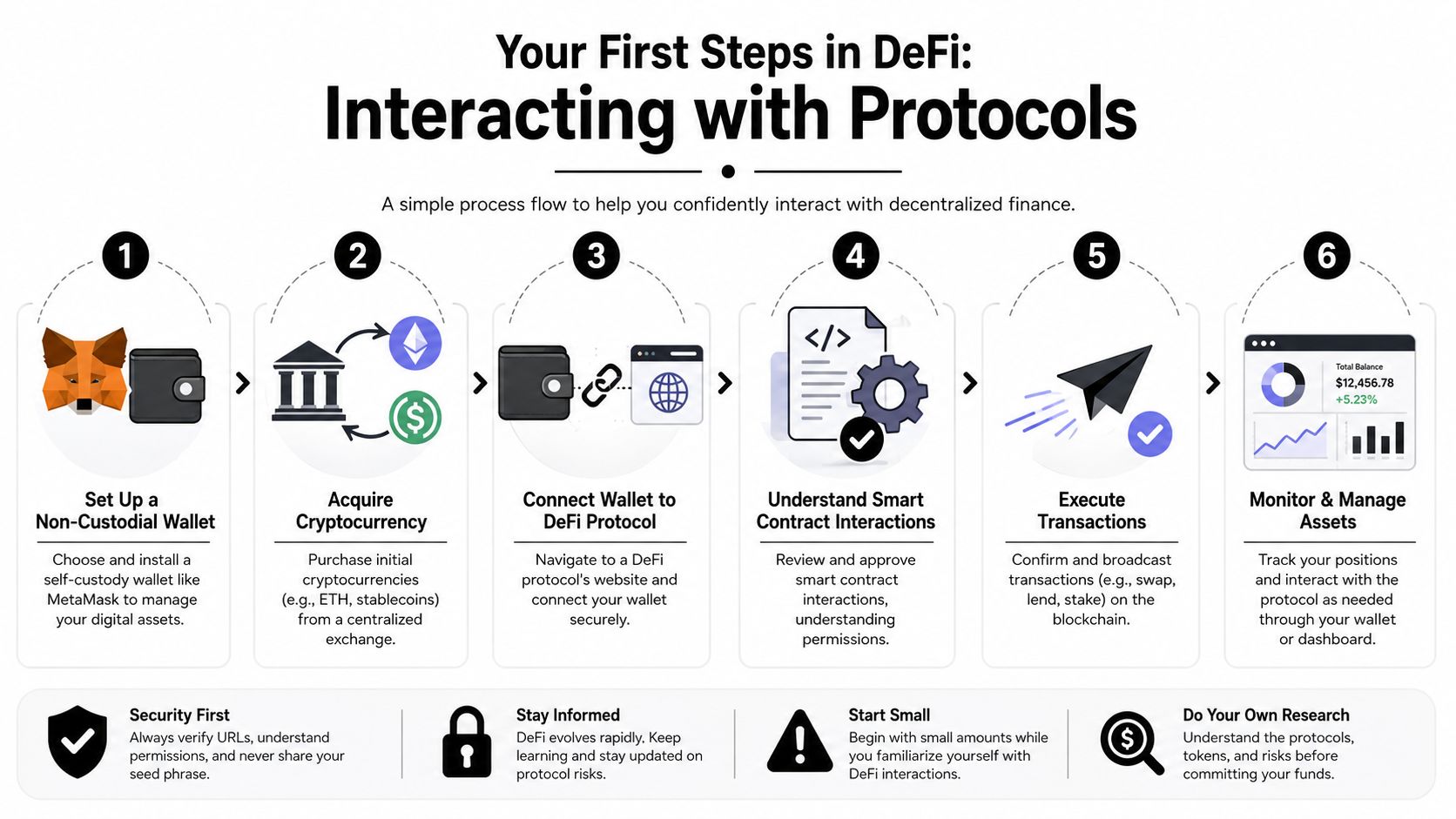

How to Interact with DeFi Protocols

For most users, the first contact with DeFi isn't reading whitepapers. It's opening a wallet, connecting to a dApp, and wondering whether the next signature request is harmless or dangerous.

A basic first workflow

A typical path looks like this:

- Install a self-custody wallet: MetaMask is still the gateway product many people start with for Ethereum and EVM-compatible networks.

- Fund the wallet: Users usually buy ETH, stablecoins, or another supported asset on a centralized exchange and transfer it into their wallet.

- Visit the protocol directly: The safest habit is to proceed with caution to the official app rather than using random search results.

- Connect the wallet: The site requests a connection so it can read your address and prompt transaction signatures.

- Approve token access if needed: Some actions require granting a smart contract permission to use a token in your wallet.

- Sign and submit the transaction: The wallet shows network fees and transaction data before broadcasting it onchain.

MetaMask's reach helps explain why this workflow has become familiar. It exceeded 100 million total users and maintained 30 million+ monthly active users in 2025, according to MEXC's DeFi user overview. That doesn't remove friction, but it does show that the wallet-first model is no longer niche.

What usually confuses first-time users

The most common misunderstanding is the difference between connecting, approving, and executing.

- Connecting a wallet usually lets the app view your public address and balances.

- Approving a token gives a contract permission to move a certain asset under specified conditions.

- Executing a transaction changes onchain state, such as swapping, lending, or staking.

Those aren't the same thing, and treating them as identical is how users get into trouble.

Before you confirm anything, read the wallet prompt as if it were a payment authorization, because that's what it often is.

Gas fees also trip people up. On Ethereum mainnet, users pay network fees in ETH for computation and settlement. On Layer 2 networks, the same interaction pattern often exists with lower cost and faster confirmation, which is one reason DeFi activity keeps spreading beyond Ethereum mainnet itself.

Regional funding rails matter too. If you're moving from fiat into crypto before using a wallet, local on-ramps can make the difference between a smooth experience and a frustrating one. Readers comparing crypto platforms using South African Rand may find that kind of regional guide useful before they even touch a DeFi app.

Navigating Security and Regulatory Risks

DeFi's upside is easy to explain. The downside takes more work, because the risks aren't all visible in the interface.

The risk most newcomers underestimate

The hardest truth in DeFi is that mistakes often can't be reversed. A critical risk in DeFi is the finality of transactions. There's no central intermediary to reverse a mistaken transfer or offer recourse if a smart contract is hacked or malfunctions, as the European Central Bank discussed in its DeFi risk analysis. If funds leave your wallet or a protocol breaks, there may be no practical path to recovery.

That sounds obvious to experienced crypto users, but many retail participants still approach DeFi with the instincts of online banking. In online banking, fraud departments, chargebacks, account freezes, and support teams exist. In non-custodial DeFi, those buffers usually don't.

Hard truth: Self-custody gives you control and removes many gatekeepers. It also removes many forms of recourse.

Technical and market structure risks

Technical risk starts with smart contracts. A bug in contract logic can lock funds, misprice collateral, or expose a pool to exploitation. Even audited code can fail under unusual conditions or interact badly with another protocol.

Economic risk is different. It comes from the design of the system rather than a coding mistake.

- Liquidation risk: Borrowers can lose collateral quickly during sharp price moves.

- Oracle risk: If an app depends on faulty price data, it can liquidate or settle incorrectly.

- Liquidity risk: A market may appear usable until volatility hits and depth disappears.

- Composability risk: One weak protocol can infect another if they're tightly connected.

For users thinking about broader crypto security, it also helps to remember that not every threat lives onchain. Exchange accounts, KYC databases, and centralized service providers can become attack surfaces too. Reports discussing 2023 Binance account leak findings are a reminder that custody and identity exposure don't disappear just because a user plans to move funds into DeFi later.

Here's a useful explainer before going further:

Why regulation matters even in permissionless systems

“Permissionless” doesn't mean “outside policy forever.” It means the application layer is open by design. Regulators still care about the people, entities, interfaces, and tokens connected to it.

Stablecoins are a good example because they're central to trading, settlement, and collateral, yet they touch banking, payments, disclosure, and reserve questions all at once. Anyone trying to understand that fault line should spend time on the topic of stablecoin regulation, because it sits close to the center of DeFi's legal future.

The practical takeaway is sober. DeFi users don't just need market awareness. They need operational discipline, contract awareness, and a realistic expectation that law and code often move on different timelines.

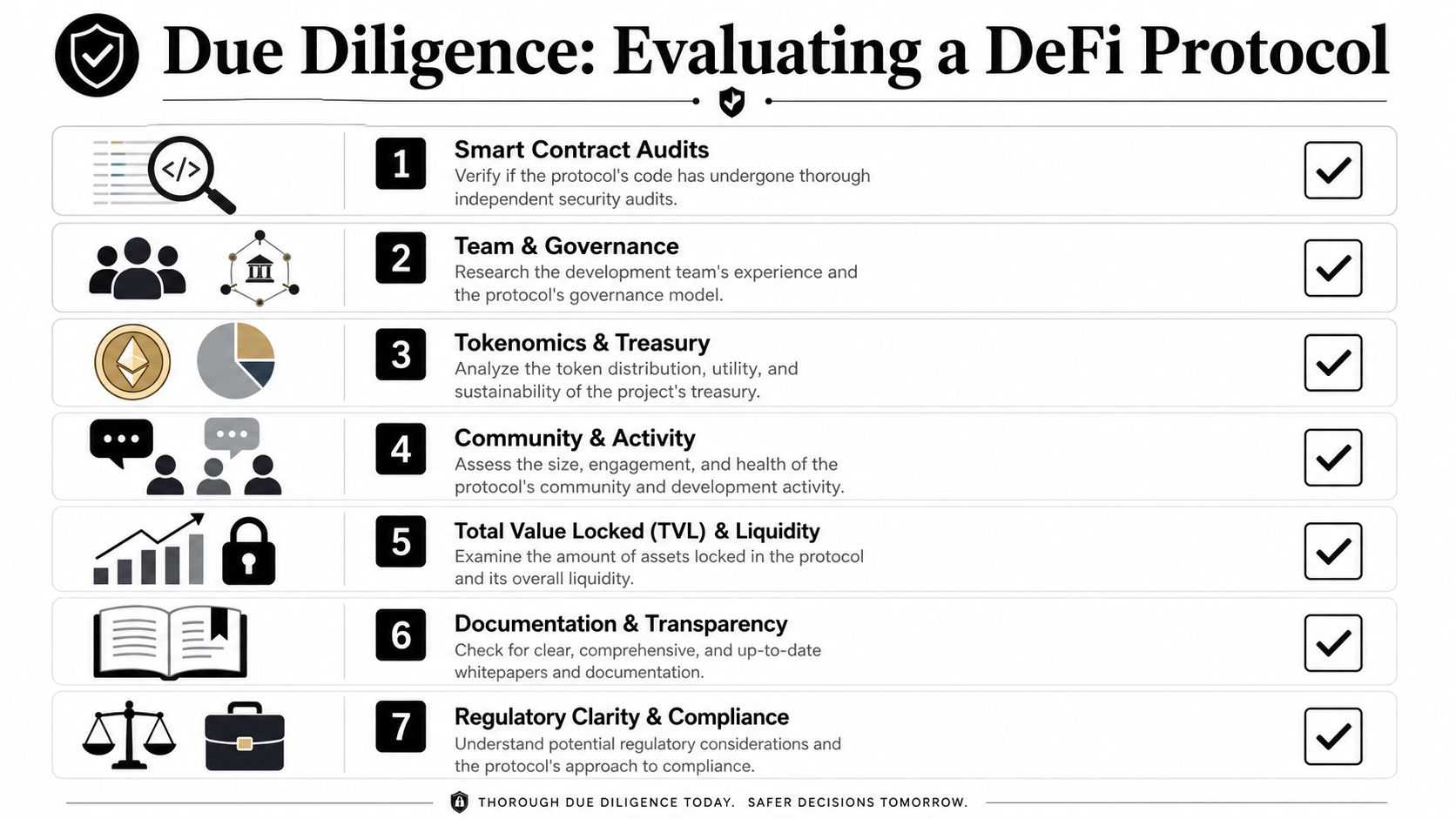

How to Evaluate a DeFi Protocol

Most mistakes in DeFi happen before the first deposit. They happen during selection. People choose a protocol because the interface looks polished, the APY looks attractive, or social media sounds confident. None of those are sufficient.

A working due diligence checklist

Before committing funds, I'd treat protocol review as a minimum checklist rather than an optional extra.

- Audit status: Find out whether the contracts were independently audited, and then read the audit summary instead of stopping at the badge.

- Documentation quality: Strong protocols explain architecture, risks, collateral rules, governance, and upgrade paths clearly.

- Admin controls: Check whether multisigs, upgrade keys, or pause mechanisms still give a small group unusual power.

- Token design: Tokenomics should make economic sense. If incentives depend on constant emissions with weak utility, caution is warranted.

- Liquidity reality: Deep liquidity and credible usage matter more than attention on social platforms.

- Governance quality: Look for signs that proposals are discussed seriously rather than rubber-stamped.

- Dependency map: Identify what external protocols, bridges, or oracle systems the app relies on.

What a serious reviewer looks for

The strongest signal isn't perfection. It's transparency. Teams that document limitations, disclose assumptions, and explain failure modes usually deserve more trust than teams that market only upside.

A few practical habits help:

| Check | Why it matters | What to look for |

|---|---|---|

| Contract transparency | You're trusting code | Public repos, clear deployments, readable docs |

| Risk disclosures | Honest teams explain downside | Liquidation rules, oracle dependencies, upgrade risks |

| Governance process | Control may still be concentrated | Proposal records, voting participation, emergency powers |

| Product fit | Complexity should match your skill level | Simple use case first, advanced strategies later |

If you can't explain where yield comes from, who can change the rules, and what happens when markets gap lower, you're not ready to size the position.

Total value locked can be a useful clue during evaluation because it hints at market trust and liquidity, but it isn't a safety certificate. Large protocols can still fail, and smaller ones can still be well designed. TVL matters most when read alongside code quality, dependencies, governance, and actual product behavior.

The Future of Decentralized Finance

The next phase of DeFi probably won't be defined by one killer app. It'll come from infrastructure improvements that make existing use cases cheaper, faster, and easier to trust.

Where the next improvements are likely to come from

Layer 2 networks are already part of that story. Lower fees and faster settlement make ordinary DeFi actions more usable, especially for smaller accounts that can't absorb high mainnet costs. Real-world asset tokenization is another major frontier because it tries to connect onchain liquidity with offchain claims and financial products. That bridge is technically and legally hard, but it's where DeFi starts to matter to markets beyond native crypto.

AI and crypto may also intersect in narrower, practical ways before they produce anything profoundly impactful. Think strategy automation, risk monitoring, anomaly detection, and smarter routing across protocols rather than a magical autonomous money manager. Useful systems usually arrive as tools, not slogans.

The uncomfortable inclusion question

The harder question is whether DeFi is moving toward its original social promise. Despite the narrative of democratizing finance, data suggests DeFi has largely failed to reach the global unbanked. OECD research from 2024 highlights that regulatory gaps and high technical barriers mean DeFi currently serves experienced speculators more than the financially excluded, according to the OECD's review of DeFi's limits for financial inclusion.

That doesn't mean the experiment failed. It means the marketing story often outran the product reality.

DeFi is still one of the most important ideas in blockchain because it proves that financial logic can run in open, composable software. But if it wants to become more than a powerful toolkit for existing crypto users, it has to solve usability, safety, dispute resolution, and compliance in ways that don't destroy the openness that made it valuable in the first place.

If you want more balanced analysis on crypto markets, Ethereum infrastructure, DeFi mechanics, tokenomics, Web3 trends, AI and crypto, and the practical risks that come with them, visit Coiner Blog. It's a strong resource for readers who want clear explanations without the hype.