Cryptocurrency ramblings

Automated Market Makers the DeFi Engine Explained (2026)

You're probably seeing AMMs everywhere right now. You swap a token in MetaMask, route through a DEX aggregator, bridge into a Layer 2, or check a new DeFi pair before it ever touches a centralized exchange. The interface looks simple. Click swap, confirm, done. The mechanism underneath is not.

That matters because automated market makers aren't just a crypto convenience feature. They're one of the core market structures that made Web3 usable without brokers, listing committees, or a traditional order book. If you trade, provide liquidity, farm yields, analyze tokenomics, or follow the tokenization of real-world assets, you're already interacting with AMM logic whether you realize it or not.

The part most guides miss is the economic tug-of-war inside the pool. AMMs aren't only about the famous formula. They're about who earns from order flow, who absorbs volatility, and why arbitrage is both necessary and costly at the same time. That's where the core lesson starts.

Table of Contents

- The DeFi Revolution Without Gatekeepers

- The Core Concept What Is an Automated Market Maker

- AMM Pricing Formulas and Mechanics Unpacked

- A Tour of Major AMM Implementations

- The Risks Every Liquidity Provider Must Understand

- Smart Strategies for LPs and Traders

- The Future of Automated Market Makers

- AMM Frequently Asked Questions

The DeFi Revolution Without Gatekeepers

A few years ago, trading a brand-new token often meant waiting for a centralized exchange to care. If the token wasn't listed, your options were ugly. Find a niche venue, trust thin liquidity, deal with delays, and hope someone on the other side of the market wanted what you wanted at the same time.

That old model created gatekeepers. Exchanges decided which assets got visibility. Professional market makers controlled much of the liquidity. Smaller projects had to fight for attention before users could even trade them efficiently.

Automated market makers changed that by turning liquidity into code. Instead of waiting for matching buy and sell orders, users trade against a smart-contract pool. That sounds technical, but the practical impact is simple. New markets can launch without asking permission, traders can access long-tail assets directly from wallets, and everyday users can supply liquidity instead of leaving that role to large firms.

That shift became one of DeFi's defining breakthroughs. Pioneered by Uniswap in 2018, the AMM model has become foundational to DeFi. By June 2026, Uniswap alone had processed over $1.2 trillion in total volume across more than 10 million unique users, according to this market maker overview. That scale tells you AMMs are no longer an experiment. They're infrastructure.

If you want a broader primer on why markets care so much about tradability, this overview of cryptocurrency liquidity is a useful companion.

Why AMMs arrived at the right moment

AMMs fit the logic of Web3.

- Wallet-native access: You don't need a brokerage-style account structure to participate.

- Smart contract settlement: Rules live onchain, where anyone can inspect them.

- Permissionless market creation: Tokens can become tradable without traditional listing pipelines.

- Composable finance: Lending apps, aggregators, yield protocols, and cross-chain tools can plug into the same liquidity base.

AMMs didn't just make token swaps easier. They changed who gets to be the market maker.

That's the revolution. The formula matters, but the removal of gatekeepers mattered first.

The Core Concept What Is an Automated Market Maker

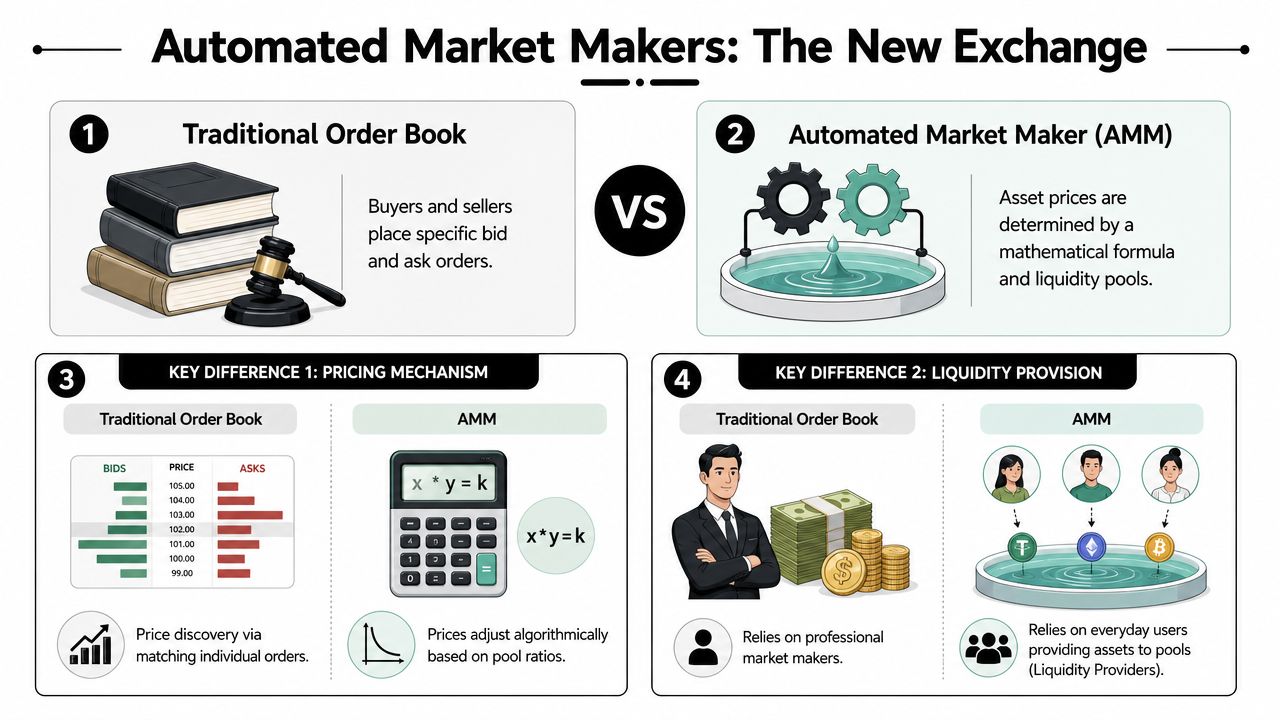

Trading is commonly understood through the order book model. Buyers post bids. Sellers post asks. If prices meet, a trade happens. That's how many stock exchanges and centralized crypto exchanges work.

An AMM replaces that matching process with a liquidity pool and a pricing rule. It functions as a self-balancing scale with two buckets. One bucket holds token X, the other holds token Y. When a trader adds one asset to the pool and removes the other, the scale tilts. The AMM responds by adjusting the exchange rate automatically.

From order books to pools

In practical terms, here's the difference:

| Market structure | What you trade against | How price is formed | Who supplies liquidity |

|---|---|---|---|

| Traditional order book | Another user's order | Matching bids and asks | Usually professional market makers and traders |

| AMM | A smart-contract pool | Formula-driven reserve ratios | Liquidity providers depositing assets |

That pool is funded by liquidity providers, often called LPs. They deposit assets into the pool, and the protocol uses those reserves to serve swaps for other users. In return, LPs earn fees from trading activity.

A simple mental model helps here. An AMM is like a vending machine that never closes, but the snack price changes depending on what's left inside. If everyone keeps taking one snack and stuffing in the other, the machine reacts by making the scarce item more expensive.

Later in this article, I'll get into LP economics and why that fee income isn't free money. For now, the key is that AMMs let markets function continuously without a human quote on the other side of your trade.

A quick visual walkthrough can help if you prefer video before the deeper mechanics:

Why the formula matters

The best-known AMM rule is the constant product function. Uniswap describes it clearly in its explanation of automated market makers: the product of the quantities of token X and token Y remains invariant after every trade, expressed as x * y = k.

In plain English:

- x is the amount of the first token in the pool

- y is the amount of the second token

- k is the constant product that must remain unchanged after a swap

If a trader removes some of token Y, the pool must receive enough token X so the product still fits the rule. That's why the price changes as reserves change. The pool isn't looking at headlines, charts, or your intent. It's only reacting to balances.

A common point of confusion for beginners is that the formula doesn't “know” the fair market price. It only creates an internal price based on the current reserve ratio. External traders and arbitrageurs later push that pool price back toward the broader market.

Practical rule: In an AMM, price is not posted first and traded second. Trading changes reserves, and reserves create price.

If you're trying to connect this to broader market behavior, this guide to price discovery helps frame why onchain and offchain pricing keep interacting.

AMM Pricing Formulas and Mechanics Unpacked

A trader sees ETH at one price on a centralized exchange and a slightly different price in an AMM pool. They hit swap. The pool reprices mid-trade. An arbitrage bot notices the gap a second later and trades too. What looks like a simple formula is really a live auction between traders, liquidity providers, and arbitrageurs.

That economic tug-of-war is the true engine behind AMM pricing.

The constant-product model stays popular because it can quote a price at any moment. But that convenience has a cost. As one side of the pool gets drained, the next unit becomes more expensive. The curve is doing two jobs at once. It serves traders, and it protects LP capital from being pulled out at a stale price.

Why slippage happens

A pool with balanced reserves works like a self-adjusting scale. If you remove a little from one side, the balance shifts only slightly. If you remove a lot, the scale tilts hard, and the terms get worse with each extra unit.

That worsening execution is slippage.

Small trades usually stay close to the quoted price because they barely disturb the reserve ratio. Large trades push the pool far from its starting balance, so the average execution price drifts against the trader during the swap itself. The AMM is not reading market sentiment or checking a price feed first. It is reacting to its own inventory.

This is also where many new users misread what the formula is doing. The pool price is an internal quote derived from reserves, not a declaration of fair value. Outside markets matter because arbitrageurs compare the pool's quote with prices elsewhere and trade whenever there is a gap. If you want a clearer framework for that interaction, this explanation of price discovery in crypto markets connects onchain pricing to the broader market.

For LPs, slippage has a second meaning. It is not just a trader problem. Every trade that moves the pool away from the wider market creates an opening for arbitrageurs to rebalance it, and those rebalancing trades often extract value from LPs. In practice, LPs are getting fee income in exchange for selling options on their inventory.

Different formulas for different jobs

“AMM” describes a category, not one formula. Different designs choose different points on the spectrum between capital efficiency, inventory risk, and rebalancing cost.

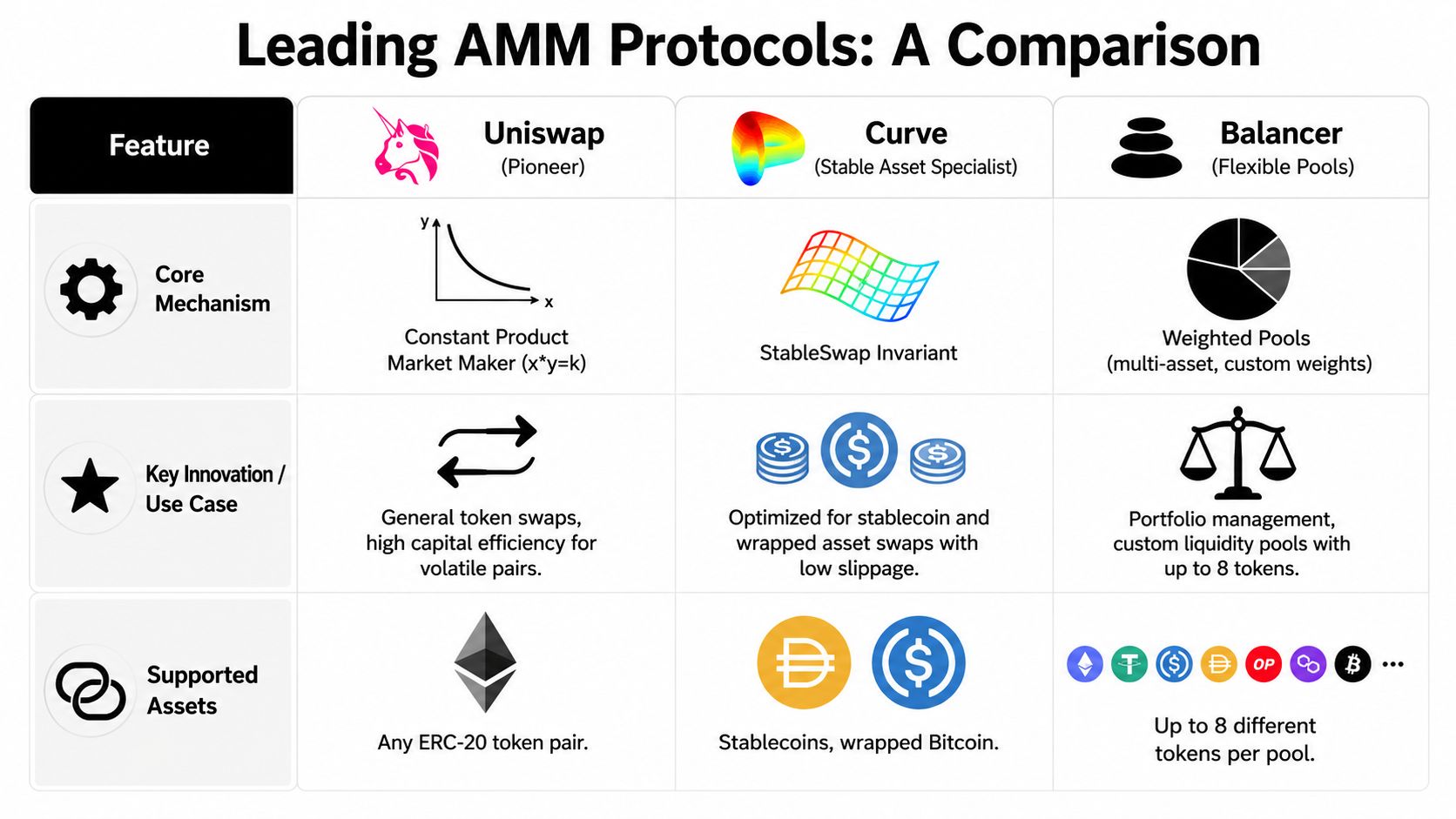

Constant product pools

This is the classic model used by Uniswap and many similar DEXs. It works well for volatile pairs because it always offers a two-sided market, even during fast moves. The price impact grows nonlinearly as a trade gets larger, which discourages anyone from emptying the pool cheaply.

That shape creates a predictable economic pattern. Traders use the pool for instant execution. Arbitrageurs keep it aligned with the outside market. LPs collect fees while absorbing the cost of being rebalanced by faster traders.

Stable asset AMMs

Protocols such as Curve changed the formula for assets that should trade near the same value, such as stablecoins or wrapped versions of one asset. Near parity, the curve stays flatter, so traders can move size with much less price impact. Once the pair drifts far from parity, the pricing gets harsher.

That design matches the economics of the assets. If USDC and USDT are expected to stay close, a pool should not charge the same slippage as an ETH memecoin pair. Stable AMMs became core DeFi infrastructure because they make routine rebalancing, collateral management, and stablecoin routing cheaper.

Weighted and multi-asset pools

Balancer expanded the idea by letting pools hold more than two assets with custom weights. These pools work like onchain index funds with a built-in trading engine. The formula continuously nudges the basket back toward its target mix as users trade against it.

That opens different use cases. A protocol treasury can keep strategic exposure. An index product can rebalance through trades rather than a manager manually buying and selling. LPs, though, still face the same basic tension. Fees come in steadily, but arbitrageurs harvest mispricings whenever the basket drifts from external markets.

Here's a simple comparison:

| AMM style | Best fit | Core advantage | Main trade-off |

|---|---|---|---|

| Constant product | Volatile token pairs | Simple and widely applicable | More slippage on larger moves |

| Stable asset model | Stablecoins and pegged assets | Better pricing near parity | Less suited to wide price divergence |

| Weighted multi-asset pools | Portfolio-like baskets | Flexible composition | More design complexity |

The design space is still expanding. Some researchers have formally proven a novel AMM mechanism with arbitrage resilience for legacy blockchains where a single miner proposes each block, as described in this paper. That line of research matters because AMMs are becoming more than swap formulas. They are market structures shaped by latency, MEV, and who captures the value of rebalancing.

New tools are pushing that evolution further. AI-based routing systems can compare pools, forecast price impact, and split orders across venues more intelligently than a simple one-pool swap. At the same time, regulation is starting to matter in a more practical way. Rules such as MiCA in Europe, and SEC scrutiny in the United States, raise harder questions about whether some LP activities look passive or more like organized market making. For LPs, formula choice is no longer only a math question. It is becoming a mix of economics, automation, and legal exposure.

A Tour of Major AMM Implementations

The easiest way to understand the AMM environment is to stop thinking in slogans and start thinking in design choices. Different protocols solved different problems.

Three platforms three philosophies

Uniswap is the generalist and the brand widely associated with AMMs. Its importance comes from setting the pattern that much of DeFi later built on. If you want broad token access, strong network effects, and the default mental model for AMMs on Ethereum and related ecosystems, Uniswap is usually the first stop.

Curve took the opposite path. Instead of trying to serve every pair equally, it specialized in stable assets and similar-value swaps. That focus made it central to stablecoin routing, yield strategies, and DeFi balance-sheet management. Curve isn't trying to be flashy. It's trying to be efficient where price relationships are tight.

Balancer leans toward customization. Its weighted pools and multi-asset design appeal to users who want more than a simple trading venue. Projects can shape pools around treasury goals, portfolio exposure, or index-style products. In tokenomics terms, that flexibility is powerful.

How users typically choose

A side-by-side lens is more useful than platform tribalism.

- Choose Uniswap when you want broad ERC-20 coverage, familiar UX, and access to a large ecosystem of wallets, aggregators, and Layer 2 deployments.

- Choose Curve when you're swapping stablecoins, wrapped assets, or other tightly correlated tokens and care about cleaner execution around parity.

- Choose Balancer when you want custom weights, more than two assets in one pool, or an onchain portfolio structure.

This isn't the whole AMM market, of course. PancakeSwap, SushiSwap, and other platforms matter too. As early 2026, major AMM platforms such as Uniswap, SushiSwap, PancakeSwap, and Balancer collectively managed over $50 billion in total value locked, while daily AMM transaction volumes exceeded $5 billion across all platforms in 2025, according to Coinbase's AMM explainer. That same overview notes that Uniswap held a 60% share of all DEX volume in 2025, while PancakeSwap had processed over $300 billion in volume by 2025.

If your activity spans multiple networks, one practical layer sits above all of these protocols: routing. Users increasingly compare pools across chains and venues rather than pledging loyalty to one DEX. If that's your world, this guide to cross-chain swaps adds helpful context.

The protocol you choose should match the job you're doing. General swaps, stable swaps, and portfolio-style pools aren't the same activity wearing different logos.

The Risks Every Liquidity Provider Must Understand

A new LP deposits into a hot pool, sees fees rolling in, and assumes the position is paying rent. Then price jumps, arbitrage bots rush in, and the wallet ends up holding more of the weaker asset and less of the winner. The fees were real, but so was the transfer of value.

That is the first mindset shift. Providing liquidity is not passive income in the usual sense. It works more like running a tiny exchange inventory that constantly gets rebalanced by the market, whether that rebalance helps you or not.

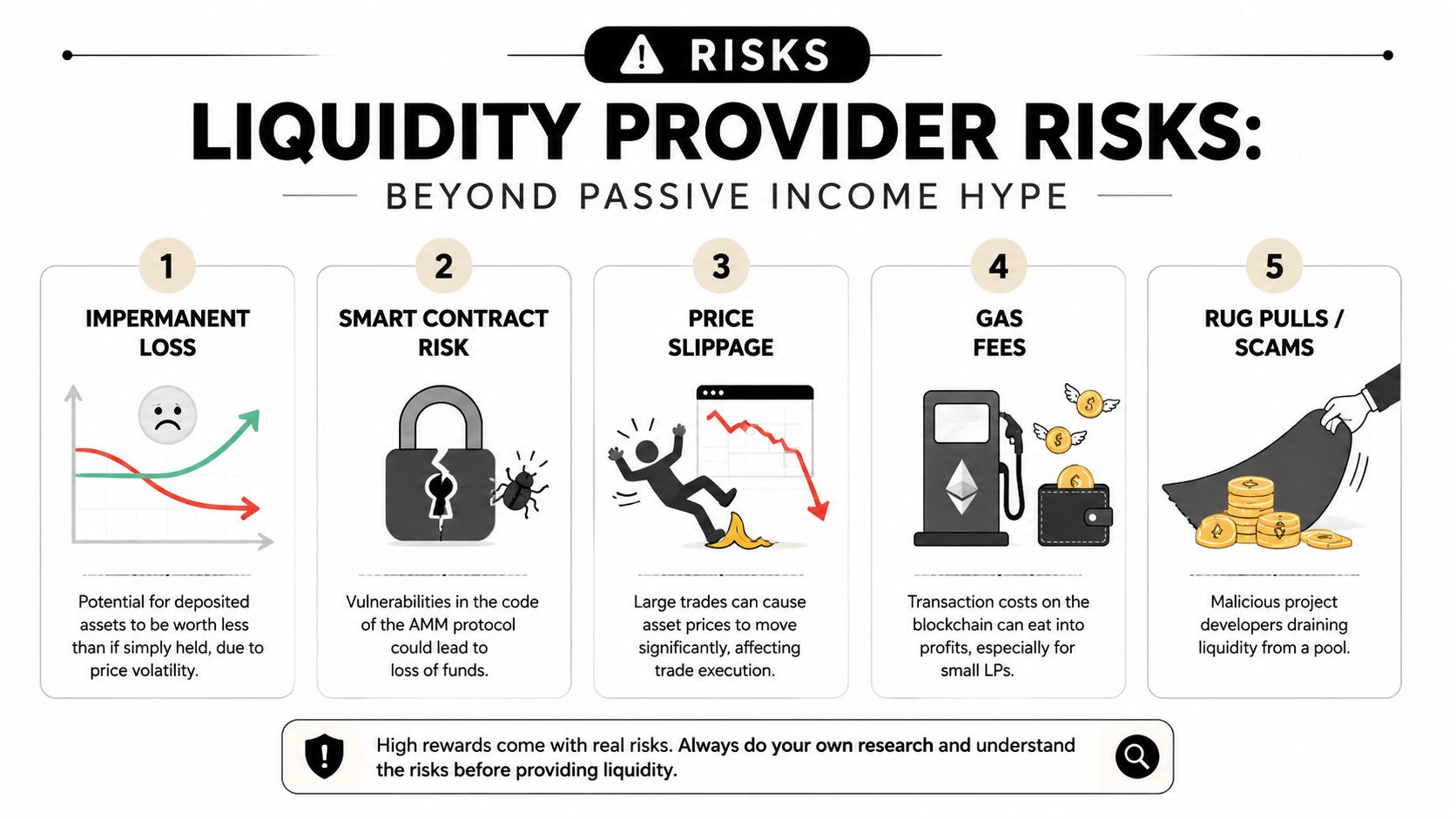

Impermanent loss is the price of being the counterparty

Impermanent loss confuses many newcomers because the name sounds temporary and harmless. In practice, it is the economic cost of letting the pool sell your outperforming asset and buy more of the underperforming one as prices move apart.

A constant-product AMM works like a self-balancing scale. If one token becomes more valuable in the outside market, traders remove some of that token from the pool until the pool price catches up. The pool stays balanced. Your portfolio does not stay the same.

That is why comparing an LP position to simple holding matters. You are not asking, “Did I make fees?” You are asking, “Did fees beat the cost of automatic rebalancing?”

This effect becomes painful in volatile pairs. Uniswap's documentation explains the pattern clearly: the farther relative prices move, the larger the gap between LP returns and a buy-and-hold portfolio can become, even before gas and taxes are considered (Uniswap Docs on impermanent loss). If you want to test that tradeoff before depositing, this impermanent loss calculator guide gives a practical way to model different price moves.

Arbitrage keeps AMMs honest, and charges LPs for the service

Arbitrageurs are not a side character in AMMs. They are part of the pricing engine.

An AMM does not “know” the fair market price on its own. It posts a price based on its pool balances. When the outside market moves first, the AMM becomes stale. Arbitrageurs then trade against the pool until its price lines up with the broader market again.

That process is good for traders using the pool later. It is expensive for LPs in the moment. The arbitrageur buys underpriced inventory from the pool or sells overpriced inventory into it, capturing the gap. In economic terms, LPs are paying for price discovery by offering stale quotes to anyone fast enough to take them.

This is the tug-of-war inside AMMs. Fee income flows to LPs, but mispricing flows to arbitrageurs. Your net return depends on which side is stronger over time.

The problem grows sharper during fast markets, thin liquidity, or poor oracle design. It also explains why AI-driven search and execution matter more now than they did a few years ago. Better bots identify tiny pricing gaps faster, route capital more efficiently, and compete harder for every stale quote. For LPs, that means the market gets more efficient while the margin for earning “easy” fees gets thinner.

The risks that look secondary often decide the final return

Price divergence gets the attention, but several other risks determine whether an LP position was worth taking.

- Smart contract risk: A bug, exploit, upgrade failure, or governance failure can overwhelm months of fee income.

- Gas and rebalancing costs: On expensive chains, entering and exiting a position can erase a meaningful share of returns, especially for smaller deposits.

- MEV, front-running, and sandwiching: Visible order flow creates opportunities for searchers, which can worsen execution and indirectly reduce the value flowing to LPs.

- Token risk: A pool is only as sound as the assets inside it. Weak token design, admin key abuse, or outright fraud can turn “yield” into exit liquidity.

- Protocol-specific constraints: For example, the XRP Ledger's AMM rules limit what pools can hold and how trust line settings affect participation.

There is also a legal layer that many LPs still ignore. Regulation is starting to matter in concrete ways, not as background noise. MiCA in Europe and the SEC's posture in the United States both push protocols, interfaces, and token issuers toward clearer disclosures, licensing questions, and stronger scrutiny around who is facilitating a market. For a casual LP, that may sound distant. It is not. If regulators treat some forms of liquidity provision, fee sharing, or governance control as more than passive software use, LPs and protocol operators could face new reporting, tax, or liability questions.

A simple filter helps before you deposit capital:

| Question | Why it matters |

|---|---|

| Do these assets move differently for fundamental reasons | Bigger divergence usually means stronger impermanent loss pressure |

| Who captures the edge in this pool, LPs or arbitrage bots | Fast external price moves can transfer value out of the pool quickly |

| Is the pool deep enough for the volume it attracts | Thin pools are easier to move and easier to pick off |

| Has the protocol been tested in volatile conditions | Security and market design matter more than headline APR |

| What legal or interface restrictions apply in your region | Access, disclosures, and liability can change by jurisdiction |

A good LP does not ask only, “What is the yield?” A good LP asks, “Who is paying that yield, and what risk am I taking from them in return?”

Smart Strategies for LPs and Traders

The people who do well with AMMs usually don't treat them like savings accounts. They treat them like active positions with changing edge.

What disciplined LPs do differently

A smart LP starts with pair selection, not APR screenshots. Stable pairs and correlated assets often make more sense for conservative capital because the pool isn't constantly fighting large price divergence. Volatile pairs can work, but only if you're confident the fee opportunity justifies the rebalancing pain.

Pool depth matters too. Small pools look attractive when incentives are flashy, but they can be brittle. According to Rango's discussion of AMM limitations, attackers can shift prices by more than 30% with trades under $10,000 in small liquidity pools. That's a serious warning, especially for tokens without strong external pricing or oracle support.

For LPs, the practical playbook usually looks like this:

- Prefer understandable pairs: Start with assets whose relationship you can explain.

- Treat fees as compensation, not free yield: Ask what risk the yield is paying you for.

- Monitor position drift: Concentrated liquidity positions, especially on designs inspired by Uniswap v3, can go from efficient to idle if price moves away from your chosen range.

- Exit weak markets early: If volume dries up or trust in the token erodes, the pool can become a trap instead of an opportunity.

Field note: The best LP positions are usually boring on the surface. Predictable flows often beat exciting token narratives.

What smart traders watch before swapping

Traders need a different mindset. Your job isn't to maximize fee income. It's to minimize bad execution.

That often means using DEX aggregators such as 1inch or Matcha, checking route previews, splitting larger trades, and avoiding thin pools during volatile periods. If you're trading on Ethereum mainnet, gas and MEV risk can distort what looked like a good quote at first glance.

A few habits go a long way:

- Check liquidity depth before placing size.

- Compare routes across protocols and chains.

- Lower slippage tolerance when possible.

- Be cautious with newly launched tokens and tiny pools.

- Understand how MEV can affect execution and final pricing.

If you want a cleaner understanding of how transaction ordering can hurt users in onchain markets, this guide to MEV is worth reading.

The bigger lesson is simple. AMMs reward attention. Passive behavior works best for protocols, not always for users.

The Future of Automated Market Makers

AMMs are entering a more serious phase. The easy story was “smart contracts replace order books.” The harder story is about making those smart contracts more efficient, more adaptive, and more compatible with regulation.

Layer 2 AI and adaptive design

Layer 2 networks are a major part of that shift. Cheaper execution changes user behavior. Traders can rebalance more often, LPs can manage ranges with less friction, and DeFi apps can compose multiple actions into a single user flow without punishing fees at every step.

The next frontier is adaptability. AMM designs are moving toward dynamic fees, smarter routing, and more context-aware liquidity. That's where AI + crypto integration becomes interesting. Not because a chatbot will magically run your LP book, but because machine learning systems can help protocols and tools analyze volatility regimes, route trades more efficiently, detect anomalous pool behavior, and support risk dashboards for active users.

In other words, AI's near-term value in DeFi is operational. It can help users and protocols react faster to market conditions that static pools handle poorly.

There's also room for hybridization. Some AMM models will keep borrowing ideas from order books, batch auctions, and oracle-assisted pricing. That trend matters for high-value tokenized assets, where pure reserve-ratio pricing may not be enough.

Regulation and tokenized assets

Regulation is no longer a side conversation. It's part of the AMM design environment now.

As SIFMA's discussion of AMMs and securities regulation highlights, evolving global frameworks such as the EU's MiCA and newer SEC guidance are beginning to address LP liability and whether certain pools may facilitate trading in unregistered securities when tokenized assets are involved.

That becomes especially important as real-world asset tokenization expands. Trading tokenized funds, bonds, or other financial claims through AMM-style systems raises a different class of legal and compliance questions than swapping meme tokens in an open DeFi pool.

A reasonable forward view looks like this:

- Layer 2 AMMs will keep improving usability.

- AI-assisted analytics will make active liquidity management more common.

- RWA tokenization will push AMMs toward more controlled and hybrid forms.

- Regulation will shape which pools, assets, and LP roles remain viable in different jurisdictions.

The AMM of the next cycle probably won't look purely like the AMM of the last one.

AMM Frequently Asked Questions

Can I provide liquidity with one token

Sometimes, yes. Some protocols and interfaces support single-sided entry by internally swapping part of your deposit or routing it into a pool structure that handles imbalance for you. The convenience is real, but the economic exposure doesn't disappear. You're still taking on pool-specific risk once the position is live.

Are Layer 2 AMMs safer or just cheaper

Mostly cheaper and faster. Layer 2 deployment can reduce transaction costs and make active management more practical, but it doesn't automatically remove smart contract risk, bridge risk, token risk, or poor pool design. Lower fees improve usability. They don't guarantee safety.

Do fees guarantee profit for LPs

No. Fees are revenue, not a promise of net gains. An LP can collect fees and still underperform a simple hold strategy if price divergence, arbitrage extraction, gas costs, or contract risk outweigh that income.

Why do small pools feel dangerous

Because they are easier to move. Thin liquidity means a trade can push the reserve ratio sharply, which affects both execution and manipulation risk. That's why obscure pairs can show dramatic price swings from relatively modest trades.

Can AMMs work for tokenized real-world assets

Potentially, yes. The concept fits onchain trading well, but tokenized securities and similar assets introduce legal, compliance, and classification questions that open crypto-native pools often didn't have to solve. Expect more hybrid designs here.

Are traders and LPs aligned

Only partly. Traders want efficient execution. LPs want fee income that compensates for risk. Arbitrageurs help keep the system aligned with external prices, but they also extract value from stale pricing. The relationship is cooperative at the system level and competitive at the wallet level.

If you want more practical crypto analysis without the hype, Coiner Blog is a solid place to keep learning. It covers DeFi, Web3, tokenomics, Layer 2 trends, AI and blockchain, NFTs, crypto gaming, and the risks that matter when real capital is on the line.