Impermanent Loss Calculator: Master DeFi LP Risk in 2026

You're probably here because you've already lived the classic LP disappointment.

You deposited into a promising pool, watched both tokens move up, collected some fees, and still ended up thinking: why does this feel worse than holding? That gap between expected yield and actual outcome is where most liquidity provider mistakes happen. An impermanent loss calculator helps, but only if you understand what it's really telling you and what it leaves out.

In DeFi, smart contracts don't care about your market view. Automated market makers rebalance your position as prices move, and that changes what you own. In a market shaped by Web3 experimentation, Layer 2 adoption, AI-assisted trading tools, and more complex tokenomics, basic LP math isn't enough anymore. You need to know when a pool is compensating you for risk, and when it's undermining your returns.

Table of Contents

- The DeFi Puzzle Why Your LP Gains Might Lag Behind HODLing

- What Is Impermanent Loss Behind the DeFi Curtain

- The Math of Impermanent Loss A Practical Breakdown

- How to Use an Impermanent Loss Calculator

- Beyond 50/50 Pools IL in Modern DeFi

- Actionable Strategies to Minimize Impermanent Loss

- Frequently Asked Questions About Impermanent Loss

The DeFi Puzzle Why Your LP Gains Might Lag Behind HODLing

A common LP experience goes like this. You add liquidity to an ETH paired pool because you want fees and upside. Weeks later, the pool looks active, both assets are worth more in dollar terms, and yet your wallet would've been worth more if you had kept the tokens untouched.

That's not a bug. It's the trade you made.

When you provide liquidity, you stop being a passive holder and become part of an automated pricing system. The AMM uses your assets to quote trades, and every swap changes your token mix. If one asset runs harder than the other, arbitrage traders pull the appreciating asset out of the pool and push the lagging asset in until pool pricing matches the market. Your share follows that rebalance.

Why the outcome feels counterintuitive

When entering liquidity pools, participants frequently focus on fee income. They typically think in terms of yield. What they often miss is that LPing is also a live rebalancing strategy with constant exposure to volatility, slippage, and execution costs. If you've ever reviewed how slippage affects trading outcomes, you already know execution friction can turn a decent idea into a mediocre result.

Practical rule: If you can't explain why this pool should outperform simple holding after fees and costs, you don't have a liquidity strategy. You have a yield hope.

The puzzle gets harder in modern DeFi. Layer 2 networks make active position management easier, concentrated liquidity raises capital efficiency, and AI-driven dashboards make pools look cleaner than they really are. But the core question hasn't changed. You're still comparing one thing against another: owning assets outright versus letting a smart contract continuously rebalance them.

That's why an impermanent loss calculator matters. It gives you a baseline for the hidden drag before you decide whether the pool's fee profile is worth it.

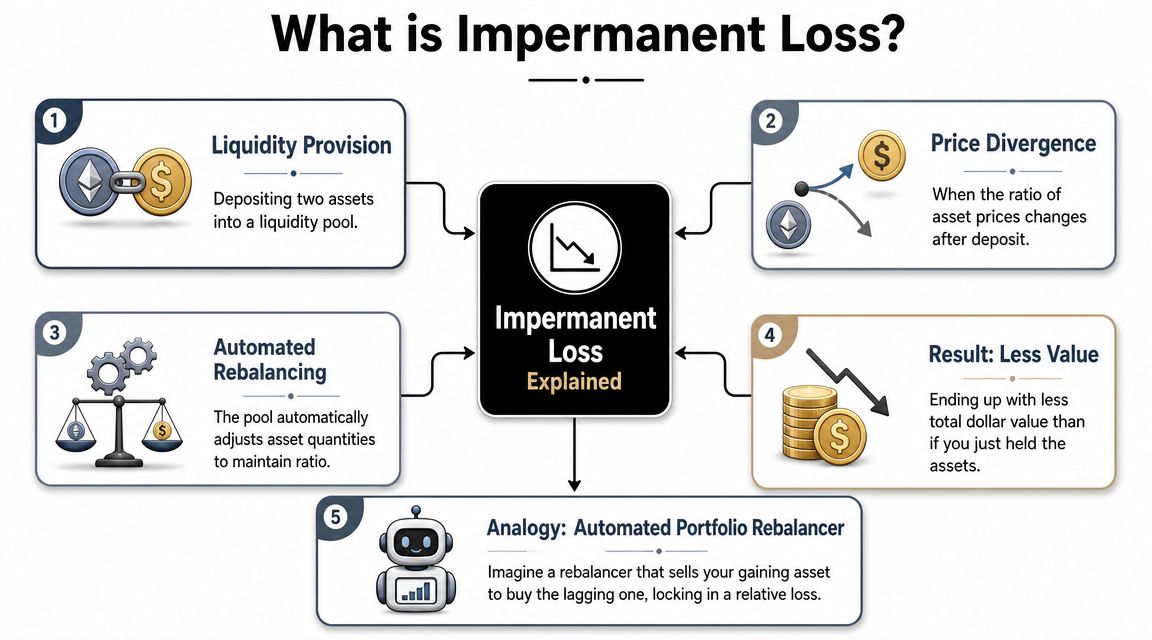

What Is Impermanent Loss Behind the DeFi Curtain

Impermanent loss is the shortfall between the value of your LP position and the value you would've had if you held the deposited assets in your wallet. It happens when the price ratio between the two assets changes after you enter the pool.

This isn't just a DeFi buzzword. It's the direct result of how AMMs work.

The pool is always rebalancing you

Think of a 50/50 liquidity pool like a balancing scale controlled by code. You place two assets on it at equal value. If one side rises in market price, traders rush in to buy that stronger asset from the pool. The AMM doesn't resist. It adjusts reserves to maintain its pricing logic.

So your position changes shape:

- You hold less of the winner: The pool sells down the asset that appreciated.

- You hold more of the laggard: The pool accumulates more of the comparatively weaker asset.

- You keep earning fees: But those fees are separate from the rebalancing effect.

- You no longer own the original mix: You own a claim on pool reserves, not a fixed token count.

That's why I often describe LP positions as an automated portfolio rebalancer you didn't personally configure. It's efficient for market making. It isn't always efficient for preserving upside.

For readers brushing up on the mechanics behind decentralized systems, a solid primer on blockchain technology basics helps frame why smart contracts can enforce this behavior without any intermediary.

Why HODLing can still win

Impermanent loss confuses newer LPs because it can happen in a bullish market. Both assets can rise against the dollar and you can still underperform HODLing. The issue isn't whether prices rose. The issue is how far they diverged from each other.

The more one asset pulls away from the other, the more the AMM reshapes your position.

This is why “impermanent” can be misleading in practice. The loss is only unrealized while you stay in the pool and price ratios remain capable of returning. Once you withdraw while the ratio is still changed, you lock in the relative underperformance.

That doesn't mean LPing is bad. It means LPing is a different strategy from directional investing. Traders use pools to earn from flow. Investors hold assets to capture upside. Sometimes those overlap. Often they don't.

The Math of Impermanent Loss A Practical Breakdown

A pool can show a healthy APR and still trail a simple hold. That gap starts with the math.

For a standard 50/50 constant-product AMM, impermanent loss depends on one input above all others: the relative price move between the two assets. If ETH doubles against USDC, the pool has to sell some of your ETH into strength to keep the reserve balance aligned with the pricing curve. If ETH keeps running, that forced rebalance keeps reducing your exposure to the winner.

You do not need to memorize the formula, but you do need to respect its shape. The loss curve is nonlinear. Small divergences are manageable. Large divergences get expensive fast. As noted earlier in the article, a 2× relative move produces a modest but real drag versus HODLing, and a 4× move is much harsher. The practical mistake is treating LP underperformance as if it grows in a straight line.

Impermanent Loss vs HODL Value at a Glance

| Price Change | Impermanent Loss |

|---|---|

| 2× | Roughly 5.7% |

| 4× | Around 20% |

Those figures matter because they frame the core LP question: do fees beat the rebalance cost? In quiet, high-volume pools, sometimes yes. In volatile pairs with weak flow, often no. APR screenshots hide that trade-off because they show income, not the value transferred away by constant rebalancing.

That is why I treat an impermanent loss calculator as a risk input, not a return model. It helps estimate the drag from price divergence. It does not tell you whether the position made sense after fees, incentives, gas, and slippage. For that, you need to track the full position over time, ideally with one of the best crypto portfolio trackers for LP performance and token exposure.

Why quants care about this math

Experienced LPs do not stop at the formula. They ask what market conditions are required for fees to offset that drag, and whether the pool structure improves or worsens the trade.

A passive deposit into a vanilla 50/50 pool is one case. Concentrated liquidity introduces another layer because your impermanent loss profile changes with range selection, time spent in range, and how often price crosses your bounds. Non-50/50 pools change the payoff again because the inventory mix and rebalance pressure are different from the standard examples most calculators assume. That is one reason people in advanced DeFi quant trading roles model volatility, flow quality, and inventory risk together instead of relying on a single calculator output.

Use the math to set expectations. Then compare that estimate against actual fee generation. That is the only comparison that matters in live LPing.

How to Use an Impermanent Loss Calculator

You deposit into a pool, fees start coming in, and the dashboard looks fine. Then one token runs, the other lags, and your LP position trails a simple hold. That is the moment an impermanent loss calculator becomes useful. It gives you a clean way to measure the drag from rebalancing before you decide whether the fees were worth taking that risk.

What to enter into the tool

The best input is boring, precise recordkeeping. Pull the numbers from your actual deposit and the current market, not from memory.

- Entry price relationship: Record the relative price of the two assets when you added liquidity.

- Current price relationship: Use the latest ratio between the pair, because IL is driven by divergence, not by the chart of one token in isolation.

- Pool design: Check whether the calculator assumes a plain 50/50 pool. Many still do, which matters if your position uses a different weight.

- Holding period notes: Keep your own record of time in the pool, since most calculators do not estimate fees, gas, or incentive decay over that period.

A calculator gives one slice of the picture. To judge the position properly, pair that output with a portfolio tracker for LP performance and token exposure so you can compare fee income, token drift, and overall wallet impact in one place.

How to read the output

The result is usually shown as underperformance versus holding the original assets. Read it that way.

If the tool shows a loss, it does not automatically mean the position lost money in dollar terms. It means the LP position ended up worth less than a passive hold of the same starting assets. In a rising market, both outcomes can still be positive, with LP merely finishing lower.

That distinction matters because LPing is a market-making trade, not a directional bet. The calculator is estimating the cost of providing that liquidity.

A practical workflow looks like this:

- Calculate the gap between your LP position and a simple hold.

- Treat that gap as the inventory cost of being in the pool.

- Add your earned fees, incentives, and any gas paid to enter, rebalance, or exit.

- Decide whether the net result justified the capital and the management effort.

Where calculators stop being enough

This is the part basic guides miss. The raw IL number is useful, but it is not the decision.

A key question is whether fees beat impermanent loss after costs. That depends on trade volume, fee tier, how long capital stayed deployed, and how much friction you paid on the way in and out. A calculator can estimate price-divergence drag. It usually cannot tell you whether the position was a good trade.

That limitation gets more serious once you move beyond simple pools. If you are using concentrated liquidity, your outcome depends on range selection, time spent in range, and how inventory shifts when price moves through your bounds. If you are in a non-50/50 pool, a generic calculator may point you in the right direction but still miss the actual payoff shape.

Use the calculator to frame the risk. Then compare that estimate against realized fees and total costs. That is how experienced LPs answer the only question that matters: did this pool outperform holding after everything was counted?

Beyond 50/50 Pools IL in Modern DeFi

You deposit into a pool, the fee APR looks strong, and the calculator says the impermanent loss is manageable. Then the month ends and a simple hold would have done better. That gap usually shows up when the pool structure is more complex than the calculator assumed.

A lot of impermanent loss content still treats DeFi like a collection of plain 50/50 constant-product pools. Real capital is now spread across concentrated liquidity, weighted pools, and protocol-specific designs that change how inventory moves as price moves. If the tool does not match the pool design, the output is only a rough estimate.

Concentrated liquidity changes the payoff shape

Uniswap V3 style liquidity is a different job from passive V2 style LPing. You are not just choosing a pair. You are choosing a price range, a fee tier, and how actively you are willing to manage the position.

That changes the economics in two ways. First, capital efficiency can improve a lot while price stays inside your range. Second, your exposure becomes path-dependent. If price runs through your band, you can end up holding mostly one asset, stop earning meaningful fees out of range, and face a very different result from the one a basic IL calculator suggested.

This is why concentrated liquidity often turns the usual question on its head. The issue is not just "what is my impermanent loss?" The practical question is whether your realized fees, after gas and rebalances, were enough to beat the inventory drag created by your range selection. In active markets, that answer can flip quickly.

If you're working through DEX design and market depth, this overview of cryptocurrency liquidity adds useful context for why pool structure changes execution outcomes.

Weighted pools are not a small variation

Weighted pools change the rebalancing pressure because the pool does not target a 50/50 split. An 80/20 pool, for example, behaves differently from a balanced pair because less capital sits in the asset with the smaller weight. That can reduce the drag relative to a 50/50 setup in some market conditions, but it also means the familiar IL shortcuts no longer map cleanly to the position.

This matters in treasury strategies, governance-token pools, and products built to keep dominant exposure to one asset while still earning swap fees. The trade-off is straightforward. You may get a pool that better fits your target exposure, but you also get a payoff profile that many free calculators do not model well.

A useful way to frame modern LP structures:

- 50/50 constant-product pools: easiest to estimate and still the baseline for many calculators

- Concentrated liquidity positions: higher fee efficiency in range, higher management burden, and more path dependence

- Weighted pools: asymmetric exposure by design, with different rebalancing dynamics and different IL behavior

- Protocol-specific AMMs: custom math, custom risks, and more room for calculator error

The practical takeaway is simple. Treat a generic impermanent loss calculator as a first filter, not a final verdict. For modern pools, the right comparison is net return versus holding after fees, incentives, gas, rebalances, and the specific pool mechanics are all counted. That is where theory stops and LP performance starts.

Actionable Strategies to Minimize Impermanent Loss

You won't eliminate impermanent loss in volatile pools. You can reduce your exposure to it by choosing structures that fit the actual job you want your capital to do.

Choose exposure that matches your actual objective

If your goal is stable yield, don't chase pools built for directional speculation.

- Use stable pairs when you want steadier LP behavior: Stablecoin pools usually keep price divergence low unless a peg breaks.

- Favor correlated assets over random pairings: Assets that tend to move together usually create less painful rebalancing.

- Treat farming rewards as a buffer, not a guarantee: Incentives can help, but they don't erase weak pool design.

- Skip LPing entirely if your real thesis is simple upside: Lending, single-sided staking, or other structures may fit better.

For active traders, MEV also matters. Arbitrage and searcher activity are part of the ecosystem that keeps AMMs aligned, but they also shape how value leaks from LPs to faster actors. If that topic is on your radar, this breakdown of MEV in crypto markets is worth reading.

Counterpoint: The highest visible yield is often attached to the pool where inventory risk is hardest to understand.

Manage the position like a position

A lot of LP mistakes happen because people treat liquidity provision as set-and-forget income. That's rarely the right frame outside conservative pools.

Use a process:

- Check how far price has moved from your entry ratio.

- Revisit whether fee generation still justifies staying in.

- Decide in advance what kind of divergence would make you exit.

- Review whether a concentrated or weighted position still matches your market view.

That discipline matters even more on faster chains and Layer 2 environments, where lower friction can tempt people into over-managing positions. The answer isn't constant tweaking. It's intentional monitoring.

If your edge is weak, simpler is often better. Blue-chip pairs, stable pairs, or no-LP alternatives usually outperform overly clever pool selection done without a real framework.

Frequently Asked Questions About Impermanent Loss

Is impermanent loss only temporary

Only while you stay in the pool and the price ratio has a chance to revert. If you withdraw while the ratio is still changed, the loss becomes permanent relative to HODLing.

Can fees fully offset it

Sometimes, yes. But that depends on volume quality, fee tier, how long you stay in, and your costs to enter and exit. That's why a raw impermanent loss calculator is useful but incomplete.

Why can I lose relative value if both tokens went up

Because impermanent loss compares your LP position against holding the original assets. If one asset outperformed the other, the AMM sold part of your winner into the laggard as the pool rebalanced.

Are some DeFi protocols better for avoiding this risk

Yes. Stable-focused pools, highly correlated pairs, lending markets, and single-sided staking models can reduce or avoid classic impermanent loss exposure, though each introduces its own trade-offs.

Is concentrated liquidity always better

No. It can improve capital efficiency, but it also increases complexity and makes your position more sensitive to price path and range selection. Better tools don't automatically mean better outcomes.

If you want more practical crypto analysis that cuts through hype and explains the actual trade-offs in DeFi, NFTs, blockchain infrastructure, and Web3 investing, explore Coiner Blog. It's a strong resource for readers who want clearer strategy, smarter risk management, and more useful crypto education.