Cryptocurrency ramblings

Liquidity of Cryptocurrency: The Ultimate 2026 Explainer

You buy a token that's trending on X, the chart looks vertical, and the community is loud enough to make you think exit demand will be there whenever you want it. Then you hit sell, and the price you get is nowhere near the number on your screen. Your order moves the market against you, the next candles look ugly, and suddenly a “winning” trade turns into a lesson.

That's not just volatility. It's liquidity of cryptocurrency in action.

Most investors learn about liquidity the expensive way. They focus on narrative, tokenomics, smart contracts, Layer 2 buzz, or AI plus crypto integrations, but ignore the one force that decides whether they can enter and exit cleanly. Traders feel it as slippage. DeFi users feel it as a poor swap. Token issuers feel it when they launch a coin, see attention pour in, then watch the chart break because the market can't absorb real flow.

Liquidity is the market's shock absorber. When it's deep, trades land with less drama. When it's thin, even a modest order can punch a hole through the book or drain an AMM pool fast. That's why pros don't ask only, “Is this asset going up?” They ask, “Can size move through this market without wrecking the price?”

If you want to understand why some crypto markets feel smooth and others feel dangerous, this is the skill that matters.

Table of Contents

- The Invisible Force Shaping Your Crypto Portfolio

- What Is Cryptocurrency Liquidity Really

- The Four Pillars of Measuring Crypto Liquidity

- Where to Find Liquidity On-Chain Versus Off-Chain

- Becoming a Liquidity Provider With AMMs and Order Books

- The Hidden Dangers of Illiquidity Risks and Fragmentation

- Your Action Plan for Navigating Crypto Liquidity in 2026

The Invisible Force Shaping Your Crypto Portfolio

Crypto traders often blame the wrong thing when a trade goes badly. They blame bots, whales, timing, news, or “market manipulation.” Sometimes those are real factors. But a lot of the damage starts with a simpler problem. There just weren't enough resting buyers near the price you expected.

That's why liquidity shapes your portfolio even when you're not thinking about it. It affects how fast you can build a position, how expensive it is to unwind one, and whether the chart you're staring at reflects a healthy market or a fragile one. Two tokens can have the same hype and wildly different execution quality.

A retail investor usually notices liquidity at the worst moment. You're rotating out of a small-cap alt, bridging between chains, or swapping through a DEX after a sudden market move. The quote looks acceptable, but the final execution doesn't. That gap is where inexperience gets taxed.

Practical rule: If you can't explain where the buyers and sellers are coming from, you don't understand the trade yet.

For token issuers, the consequences are even sharper. A project can have a strong product, a clever Web3 narrative, and active users, but still fail in the market if liquidity is shallow or scattered across too many venues. Price discovery becomes erratic. Large holders become dangerous. Community confidence weakens because every significant trade creates visible stress.

This is why seasoned investors treat liquidity as infrastructure, not as a side metric. It sits underneath price, volume, and market sentiment. If the plumbing is weak, everything above it looks stronger than it really is.

What Is Cryptocurrency Liquidity Really

Liquidity is the ease with which you can buy or sell an asset without causing a big price move. In crypto, that definition matters more than it sounds, because a market can look active while still being hard to trade well.

A simple way to think about liquidity

Think of liquidity like water depth.

Drop a cup of water into a swimming pool and almost nothing changes. Drop the same cup into a shallow pan and the water splashes everywhere. The trade size is the same in both cases. What changes is the market's ability to absorb it.

That's the easiest way to understand the liquidity of cryptocurrency. A deep market absorbs orders smoothly. A thin market reacts violently.

In centralized exchanges, that depth usually sits in the order book as bids and asks around the current price. In DeFi, it often sits inside AMM pools, where smart contracts price trades based on the balance of assets in the pool. Different mechanics, same core question: how much size can the market handle before price jumps?

Why price and market cap can mislead you

A token can have a high quoted price and still be illiquid. It can also have a respectable market cap and still trade poorly if only a small slice of supply is actively available near the market price. That's why professionals don't treat price alone as proof of strength.

A healthier lens looks at execution. Can you enter and exit without paying a hidden penalty? Can a larger buyer do the same? Can the token sustain normal two-way trading, not just bursts of enthusiasm?

Here's a simple distinction:

- Liquid asset: Buyers and sellers are consistently available, spreads are relatively tight, and normal trades don't yank price around.

- Illiquid asset: Orders are sparse, spreads are wider, and even medium-sized trades can move the market sharply.

- Pseudo-liquid asset: It looks fine during calm conditions, then becomes hard to trade when volatility spikes.

Liquidity isn't the same thing as popularity. It's the market's capacity to process demand without breaking structure.

That's why liquidity is one of the most useful health checks in crypto. It tells you whether market interest is durable, whether DeFi participation is real, and whether a token's chart can survive pressure instead of collapsing under it.

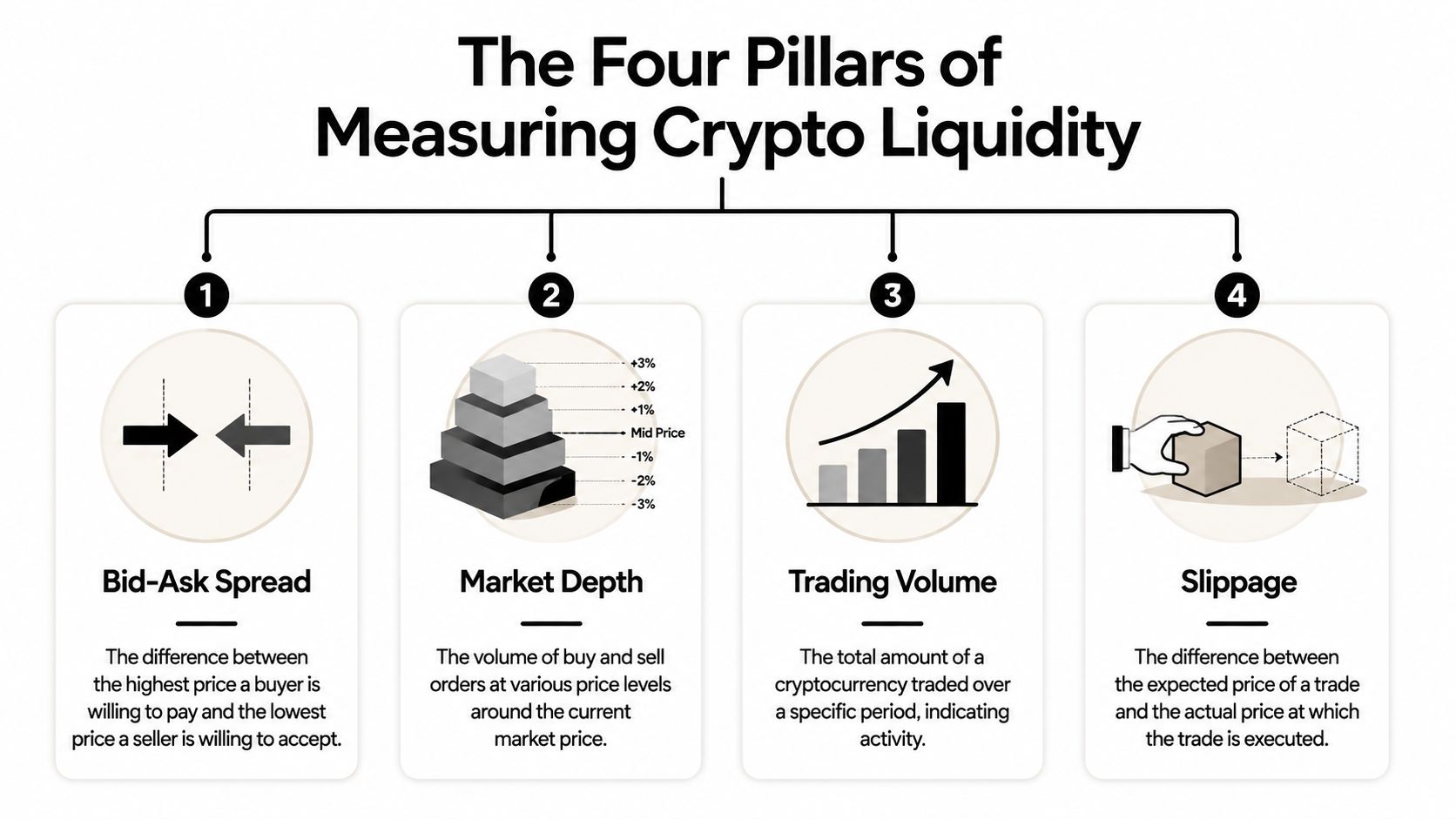

The Four Pillars of Measuring Crypto Liquidity

A market can look healthy on the screen and still punish you the moment you try to trade real size. That is why experienced traders judge liquidity with a handful of metrics that describe execution, not just appearance.

For traders, these pillars answer a practical question: can you get in and out at a fair price? For token issuers, they answer a different one: have you built a market that can absorb demand across venues and chains, or one that breaks under pressure?

Bid ask spread

The bid ask spread is the distance between the highest bid and the lowest ask. It is the first friction cost you pay.

A tight spread usually means buyers and sellers are competing close to the current price. A wide spread signals thinner participation, weaker market-making, or stress. In fragmented crypto markets, the spread can also widen because liquidity is scattered across multiple exchanges, pools, and chains instead of concentrated in one place.

Airport currency exchange works like a thin crypto market. The quoted rate looks simple, but the hidden cost is large because the venue has limited competition and wants protection. A tight institutional FX market works the opposite way. Crypto follows the same logic.

Market depth

Market depth measures how much buy and sell interest sits near the current price. Many investors misread the market here. A token may show a clean top quote, but that says very little about whether the next $50,000 or $500,000 can trade cleanly.

What matters is the shape of the book or pool around the mid-price. Are there meaningful resting orders nearby? Is liquidity balanced on both sides? Does size disappear a few ticks away, or does it keep building?

Amberdata's liquidity analysis shows that at 5 basis points, average depth stands at $1.85 million, and at 25 basis points it rises to $7.56 million. That matters because larger participants rarely care only about the first quote. They care about how much size the market can absorb before execution quality deteriorates.

A useful way to read depth:

| Metric | What it tells you | Why it matters |

|---|---|---|

| Tight top-of-book quotes | Surface-level tradability | Often enough for small orders |

| Deeper layers near price | Capacity for larger trades | Reduces the odds of sharp price impact |

| Balanced bids and asks | Two-way market health | Supports steadier price discovery |

For token issuers, depth is not just a trading statistic. It is a credibility test. Weak depth can make listings look performative, especially if a token trades well only in tiny size on one venue while appearing active on aggregators.

Slippage

Slippage is the gap between the price you expect and the price you receive. It converts abstract liquidity talk into a cash cost.

In an order book, a larger market order walks up or down the book as it consumes available liquidity at each level. In an AMM, the same trade pushes the pool balance out of line, and the pricing curve gives you progressively worse fills as size increases. Different mechanics, same economic result.

Watch slippage most closely in these situations:

- During volatility: resting liquidity gets pulled or repriced fast.

- In smaller tokens: books and pools are easier to overwhelm.

- Across fragmented venues: the best displayed quote may sit on a venue with little usable size.

Trading habit: Don't evaluate a market by the first quote you see. Evaluate it by the fill you'd get for the size you plan to trade.

TVL in DeFi

For on-chain markets, Total Value Locked, or TVL, adds another layer. It measures how much capital is committed to DeFi protocols such as DEX pools, lending markets, and collateral systems.

TVL is not a substitute for spread, depth, or slippage. It answers a different question. Is there enough committed capital to support trading activity, or is the market relying on short bursts of attention? In AMMs, more capital in the pool often means the pricing curve is harder to push around, which gives traders better execution for a given order size.

This metric has direct consequences for token issuers in a multi-chain market. A project can launch on several chains, advertise broad availability, and still leave traders stuck in shallow pools with poor routing. High headline reach does not guarantee usable liquidity. What matters is where the capital sits, how concentrated it is, and whether it supports real trading size.

Where to Find Liquidity On-Chain Versus Off-Chain

A trader trying to move $25,000 of BTC and a token issuer trying to support a new market often ask the same question from different angles. Where is the actual liquidity, and how fast does it disappear when size hits the market?

In crypto, liquidity lives in two main places. Off-chain, it sits on centralized exchanges in order books. On-chain, it sits in DEX pools, on-chain order books, and routing systems that pull from multiple venues. The difference is not academic. It changes execution quality, custody risk, listing strategy, and even which chain a token team should support first.

CEX liquidity and order books

Centralized exchanges still dominate deep liquidity for major assets because they concentrate buyers and sellers in one matching engine. For BTC and ETH, that usually means tighter spreads and more size near the mid price than you will find on a single DEX pool.

Analysts at CoinGecko's 2025 crypto liquidity research found that Binance captured about 32% of total Bitcoin orderbook depth across major exchanges, and that at plus or minus $100 from market price, Binance alone provided around $8 million in liquidity on both the buy and sell sides. That concentration matters because displayed liquidity across crypto is uneven. A few large venues carry a disproportionate share of usable size.

For traders, the practical takeaway is simple. If you need to execute size in majors, start where the book is thick enough to absorb your order without forcing you several price levels away from the quote. For token issuers, the lesson is different. A listing on a recognizable CEX can improve price discovery and attract flow, but only if the market maker support and book depth are real. A ticker symbol alone does not create liquidity.

CEXs also give active traders the tools they expect, including fast matching, conditional orders, and deep derivatives integration. The tradeoff is counterparty exposure. Your capital depends on the exchange staying solvent, operational, and accessible when the market gets stressed.

DEX liquidity and AMMs

On-chain liquidity follows different mechanics. Many DEXs use Automated Market Makers, or AMMs, where traders swap against a pool rather than against another trader's posted order. The pool acts like a vending machine with a dynamic price tag. As one asset gets bought out of the pool, the exchange rate moves against the next buyer.

That design makes market making permissionless. It also makes liquidity highly path-dependent. A token can look active on a block explorer and still be difficult to trade if its capital is split across Ethereum, Base, Arbitrum, Solana, and a few small side pools with weak routing between them.

This matters even more for issuers than for traders. A team can launch on multiple chains to widen distribution, but if each pool is shallow, every market ends up feeling thin. Traders pay more slippage. Arbitrage becomes less efficient. The token's quoted price may look healthy while real executable size remains poor.

DEXs still offer clear advantages. They let traders keep custody, reach newer assets earlier, and plug directly into lending, staking, and bridge activity. For many niche tokens, on-chain venues are not the backup option. They are the primary market.

A quick visual helps if you want a primer on exchange mechanics:

How to choose the right venue

The right venue depends on what you are trying to accomplish.

| If you care most about | CEXs often fit better | DEXs often fit better |

|---|---|---|

| Large trade execution in majors | Yes | Sometimes |

| Self-custody | No | Yes |

| Access to early or long-tail tokens | Limited | Stronger |

| Integration with DeFi apps | Limited | Native |

| Fiat on-ramps and simpler onboarding | Stronger | Weaker |

A disciplined trader usually uses both sides of the market structure. CEXs often handle deep execution for majors and fast tactical entries. DEXs often handle emerging assets, governance tokens, and positions tied to specific chains or DeFi protocols.

For token issuers, venue choice is a strategic capital allocation decision. Put liquidity where your users already are, where routing is efficient, and where market makers can support real two-sided flow. In a fragmented multi-chain market, broad presence is less valuable than concentrated, usable depth.

Becoming a Liquidity Provider With AMMs and Order Books

A trader pays for liquidity. A liquidity provider tries to get paid for supplying it. That sounds simple until you see what you are taking on: inventory risk, adverse selection, fee compression, and in DeFi, smart contract exposure.

For traders, the practical question is execution quality. For token issuers, it is market quality. If your token has shallow books or weak pools, every buyer and seller feels it in slippage, wider spreads, and unstable price discovery. Providing liquidity, or paying others to do it well, is often part of building a usable market.

Order book market making

On centralized exchanges and some on-chain order book venues, liquidity providers post bids and asks around a reference price. Their goal is to earn the spread again and again while keeping inventory within limits.

A good analogy is running a currency booth at a busy airport. You quote a buy price and a sell price. If flow is balanced, the spread is your revenue. If one side of the market overwhelms you just before price moves, your inventory becomes the problem.

That is why professional market making is usually automated. The hard part is not placing orders. The hard part is updating quotes fast enough when volatility jumps or informed traders hit stale prices.

The compensation can be real, but it rises with risk. According to the Riksbank working paper on trading volume and liquidity provision in cryptocurrency markets, BTC and ETH may yield roughly 0.5% to 1% annualized liquidity premia, while illiquid altcoins with under $10M daily volume can exceed 5% to 10%, with about 3x the volatility. For a token issuer, that tradeoff matters. Thin markets may attract liquidity only if providers are paid enough to tolerate the extra inventory risk.

AMM pools and impermanent loss

On decentralized exchanges, liquidity provision works differently. You deposit assets into a pool, and an automated market maker, or AMM, uses a pricing formula to quote trades against that pool.

AMMs work like a vending machine that reprices itself after every purchase. You do not negotiate with another trader on every swap. The pool adjusts the price mechanically based on its token balances.

That design made market making available to far more participants. You do not need exchange infrastructure or a low-latency trading stack. You do need to understand what the pool is doing to your inventory.

The biggest point of confusion is impermanent loss. If one asset in the pool rises much more than the other, the AMM sells some of your winner and buys more of your laggard as traders rebalance the pool. Your wallet value may still go up, but it can lag a simple buy-and-hold position in the same two assets.

Three practical distinctions help:

- Fee income can offset the drag: Busy pools with steady two-way flow give providers a better chance to come out ahead.

- Pair selection matters more than headline APY: Volatile token pairs can show attractive fees while increasing rebalancing losses.

- Stable or correlated assets behave differently: Pools made of stablecoins or closely linked assets usually face less severe impermanent loss from price divergence.

- Protocol risk is part of the return: Smart contract bugs, oracle failures, and governance mistakes can overwhelm months of fee income.

Providing liquidity is a market business, not passive yield farming. You are getting paid to warehouse risk and process order flow.

When liquidity provision makes sense

Liquidity provision fits investors who can answer three questions before depositing capital or posting quotes: What flow is likely to hit this venue? What inventory am I willing to hold if conditions turn? What happens if liquidity fragments across chains or exchanges?

For traders, the cleaner setups are often stablecoin pools, major pairs with durable volume, or selective order book quoting where execution discipline matters more than speed alone. For token issuers, the better question is whether the liquidity setup creates usable depth for your real users. A token spread across five chains and ten tiny pools can look widely distributed while still trading poorly in practice.

It usually goes wrong when yield is treated as free money. In newer ecosystems, narrative-driven altcoins, and thin multi-chain launches, advertised returns can reflect one thing above all else: someone is being paid to absorb risks that casual investors have not measured.

The Hidden Dangers of Illiquidity Risks and Fragmentation

A trader sees BTC quoted at one price, submits a large order, and gets filled much worse than expected. A token issuer sees their asset listed on several chains and venues, yet users still complain that every meaningful trade moves the market. Both problems come from the same place. Liquidity is present in pieces, not in one usable pool.

Why fragmentation hurts everyone

Crypto liquidity now sits across centralized exchanges, decentralized exchanges, Layer 2s, sidechains, and bridged versions of the same asset. On paper, that looks like broad access. In practice, it often works like a city where the water supply is split across many small tanks. The total volume may look adequate, but the pressure at your tap can still be weak.

That gap between visible price and executable size matters most when trade size rises. CryptoRank's coverage of the crypto liquidity crisis and institutional adoption notes that institutions can face 2% to 5% slippage on a $10M+ BTC trade in fragmented markets, while forex markets often operate with less than 0.01% spreads according to the same CryptoRank summary. For large allocators, that is not a minor trading cost. It changes whether the market is usable at all.

Retail traders run into the same structure on a smaller scale:

- Cross-chain mismatch: The token you want may exist on several networks, but the chain you are using may have thin depth and wide slippage.

- Routing dependence: Good execution can depend on aggregators, bridges, and whether one pool was just drained by a previous trade.

- Misleading quotes: A screen can show an attractive price for a tiny amount, then deteriorate fast when your actual order hits.

For token issuers, fragmentation creates a strategic trap. Spreading incentives across too many chains, market makers, and pools can create the appearance of distribution while weakening trade quality everywhere. Users do not care that your token is available in ten places if none of those venues can absorb real buying or selling.

A token can be widely listed and still be functionally illiquid.

That distinction matters in a multi-chain market. Listing count is a marketing metric. Usable depth is a market structure metric.

How lending stress drains liquidity

Lending markets add another layer of fragility. Overcollateralization protects lenders from some borrower default risk, but it does not guarantee orderly exits during stress.

Here is the mechanism. A borrower posts collateral, borrows against it, and looks safe while prices are stable. If the collateral drops fast, liquidators step in and sell that collateral into the open market. If the market is already thin, those sales push prices down further, trigger more liquidations, and widen spreads at the worst possible moment.

AMMs make this dynamic easy to underestimate. A pool can look deep near the current price, then become expensive to trade through as you move along the curve. Order books show the same problem differently. Size disappears as bids get pulled. In both cases, the market can feel liquid until stress tests it.

For traders, the consequence is simple. Your exit price during volatility may have little resemblance to the calm-market quote you saw an hour earlier.

For token issuers, the lesson is harsher. If your token is used as collateral, paired in a few thin pools, and bridged across multiple chains, a shock in one venue can spread through the rest of your market fast. Liquidity fragmentation stops being an inconvenience and becomes a balance-sheet problem for your holders, your treasury, and any protocol integrated with your asset.

That is why fast-growing sectors such as AI tokens, tokenized real-world assets, and newer Layer 2 ecosystems deserve extra scrutiny. Capital can arrive quickly. Reliable depth usually does not arrive at the same speed. When narrative growth outruns liquidity quality, the unwind is often far more violent than the chart suggested in quiet conditions.

Your Action Plan for Navigating Crypto Liquidity in 2026

Understanding liquidity gives you an edge because it forces you to think like an operator, not just a speculator.

Checklist for retail traders and investors

- Check the venue first: Look at the actual order book on a CEX or the pool depth on a DEX before you trade.

- Test size, not just price: Review what happens to your planned order size, not a tiny sample trade.

- Use slippage controls carefully: Tight settings can protect you, but they can also cause failed swaps in fast markets.

- Compare chains and routes: On DEXs, aggregators can help find better execution across pools.

- Watch the market around the token: If a token depends on one pool, one exchange, or one bridge, treat that as a structural risk.

- Respect volatility windows: Thin liquidity gets thinner during violent moves.

Checklist for token issuers and project founders

- Concentrate early liquidity: Don't scatter capital across too many venues at launch.

- Design tokenomics around tradeability: Emissions, release schedules, and incentives should support a stable market, not overwhelm it.

- Pair listings with real market support: A listed token without dependable liquidity is just a public chart with private fragility.

- Think cross-chain strategically: Expanding to Layer 2 or new ecosystems can help distribution, but only if liquidity follows.

- Monitor DeFi dependencies: If your token sits inside AMMs, lending loops, or collateral structures, stress can spread quickly.

- Build for trust: Healthy liquidity attracts better users, larger capital, and more durable price discovery.

The market will keep evolving through DeFi, Web3 infrastructure, AI plus crypto products, and tokenization. But the basic rule won't change. A token isn't just something people want to buy. It's something the market must be able to absorb.

If you want more practical breakdowns like this on Bitcoin, Ethereum, DeFi, NFTs, GameFi, Layer 2s, tokenomics, and the mechanics that move markets, follow Coiner Blog for new guides and analysis.

6 Comments