Cryptocurrency ramblings

Future of Bitcoin: When All Bitcoins Will Be Mined

The last Bitcoin is projected to be mined around the year 2140 because the network's supply is fixed at 21 million BTC and new issuance keeps slowing through a programmed halving cycle. But if you want to understand when all bitcoins will be mined in any meaningful economic sense, the more important answer is that Bitcoin starts feeling “done” much sooner, as new supply becomes a tiny part of the system.

Stopping at 2140 and treating it like the whole story misses the more useful question. When does Bitcoin stop mattering as a source of new coins and start operating mainly as a fee-funded network?

That distinction matters for investors, miners, and anyone trying to understand Bitcoin's long-term role in Web3, DeFi, and the broader digital asset economy. It also matters if you want to separate trivia from tokenomics. The calendar date tells you when issuance finally reaches zero. The economic transition tells you when scarcity is already doing most of the work.

If you need a quick refresher on how the system itself works before going deeper, this primer on blockchain technology basics is a useful foundation.

Table of Contents

- The End of an Era Is Bitcoin Mining Almost Over

- The Genius of 21 Million Why Bitcoin Has a Hard Cap

- The Halving The Engine That Controls Bitcoin's Supply

- The Long Countdown Bitcoin's Issuance Curve to 2140

- Life After the Last Bitcoin The New Era for Miners

- Frequently Asked Questions About Bitcoin's Future

The End of an Era Is Bitcoin Mining Almost Over

Bitcoin mining isn't almost over in the calendar sense. It still has a very long tail. Yet in another sense, the transition is already underway because the network is moving from a world shaped by new coin issuance to one shaped by fees, utility, and market demand.

That's why the headline question can be misleading. “When all bitcoins will be mined” sounds like a finish line. Bitcoin doesn't really have a dramatic final scene. It has a slow fade in which each halving reduces the flow of new BTC and shifts more of the network's economics onto users who pay to move value on-chain.

Why the common framing falls short

A lot of readers picture a countdown clock hitting zero and miners suddenly stopping. That isn't how the protocol is built. Blocks continue. Transactions continue. Validation continues. What changes is the composition of miner revenue.

Bitcoin's monetary policy is best understood as a glide path, not a cliff.

That's a useful lens for anyone evaluating Bitcoin as digital gold, a reserve asset, collateral in DeFi rails, or a base layer for Layer 2 systems. If you only focus on the last coin, you miss the deeper story. The deeper story is how scarcity, network usage, and fee markets gradually replace subsidy-driven issuance.

Why this matters now

The topic matters now because Bitcoin's role is expanding beyond simple buy-and-hold narratives. It sits inside a larger crypto conversation that includes Layer 2 scaling, tokenomics, real-world asset tokenization, AI-linked crypto products, and Bitcoin-adjacent financial rails.

For investors, the takeaway is simple:

- Scarcity is already visible: Bitcoin's fixed-supply design isn't theoretical. It's being enforced in real time.

- Miner incentives are evolving: The network's future security depends less on fresh issuance over time.

- Utility becomes more important: Payment layers, settlement demand, and Bitcoin-based financial activity matter more in a lower-subsidy world.

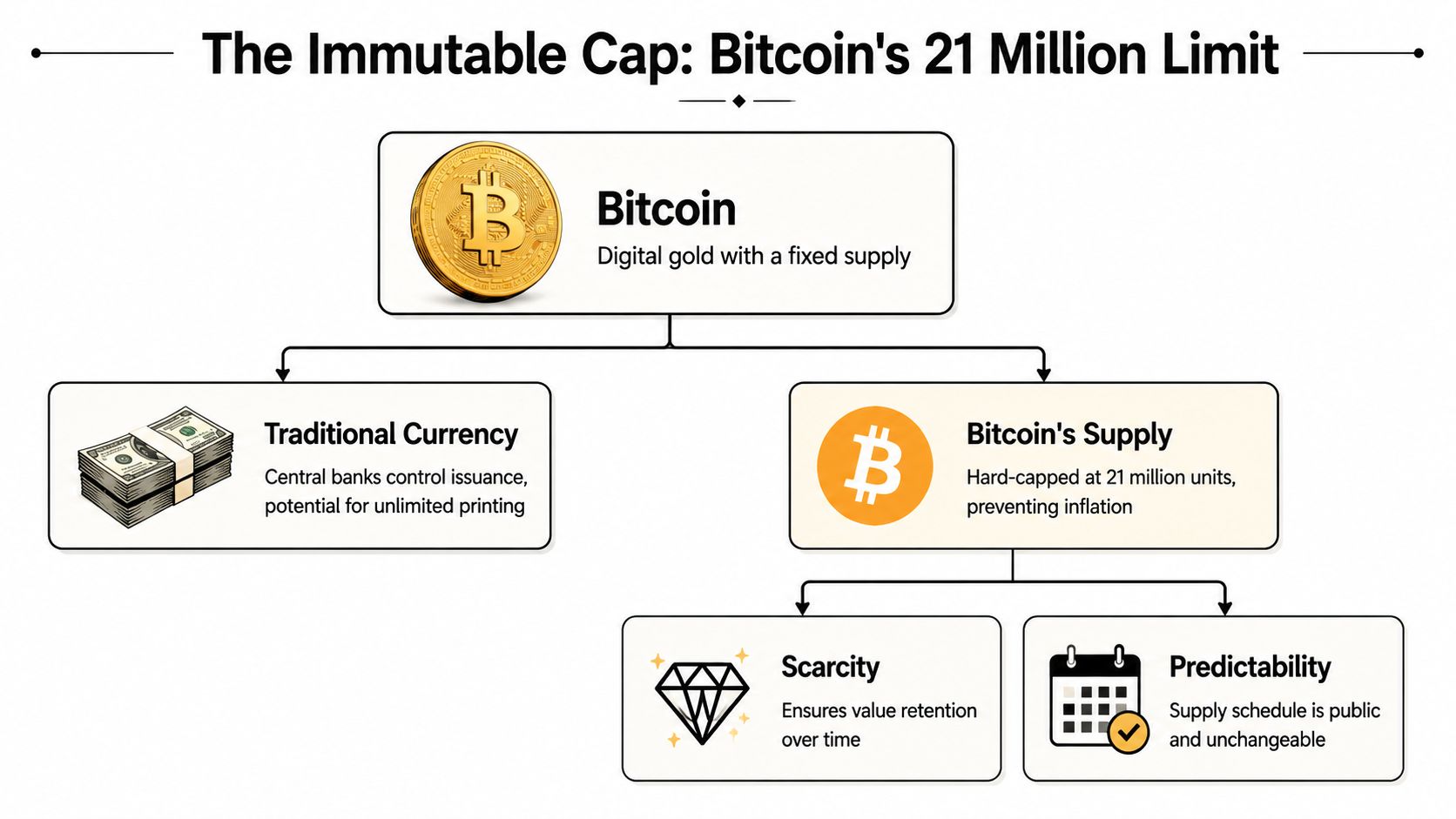

The Genius of 21 Million Why Bitcoin Has a Hard Cap

Why does the number 21 million matter so much if the network will still be producing blocks for more than a century?

Because Bitcoin's hard cap is doing two jobs at once. It sets the final limit on supply, and it shapes the economics long before the calendar reaches the last fraction of a coin. That is why the network can feel monetarily mature well before the famous 2140 date.

Why scarcity is the point

Bitcoin introduced a form of scarcity that runs on rules instead of human discretion. In a fiat system, supply can expand when policymakers decide conditions call for it. In Bitcoin, the issuance path is written into the protocol. That makes the asset easier to evaluate because the long-term supply target does not change with elections, central bank meetings, or emergency interventions.

Gold is the closest analogy, but Bitcoin is stricter. New gold can appear if mining technology improves or a major deposit is discovered. Bitcoin does not have that kind of surprise. The cap is fixed in code, which is why so much of Bitcoin's identity starts with scarcity.

That design choice goes back to the project's earliest moments. The logic behind a scarce, rule-based money begins with the Bitcoin Genesis Block, where the monetary policy was introduced as software rather than a promise.

Practical rule: If you want to understand Bitcoin's long-term investment case, study the supply rules before you study the price history.

The cap matters before the last coin arrives

A common misunderstanding is that Bitcoin's scarcity only becomes meaningful at the very end of the mining schedule. The more important reality is economic completion. By the time the final scraps of new supply are being issued, Bitcoin will have spent decades with very little new issuance entering the market.

That is a bit like watching a printing press slow from full speed to a near stop. The machine is still on, but its effect on total supply becomes small enough that the system already behaves like a nearly fixed-supply asset.

So the hard cap is not just a finish line. It is a credibility device. It tells every participant, early and late, that dilution has a limit and that the limit is visible in advance.

Why investors watch this so closely

For investors, the importance of 21 million is straightforward. If demand changes over time while new supply becomes harder and slower to produce, scarcity becomes more than a slogan. It becomes part of market structure.

That also helps explain why Bitcoin influences how people judge crypto tokenomics more broadly. Many projects talk about limited supply. Bitcoin made supply restraint the base rule of the system itself, and the market has treated that rule as one of the asset's defining features ever since.

If you want a live dashboard to track Bitcoin while following price, market cap, and circulating supply, it helps connect the abstract idea of a hard cap to day-to-day market behavior.

The deeper point is easy to miss. Bitcoin will reach calendar completion far in the future, but its economic completion arrives much sooner, as new issuance fades and fee-driven activity matters more to miner revenue and network security.

The Halving The Engine That Controls Bitcoin's Supply

How does Bitcoin slow new supply without anyone voting on it or adjusting it year by year?

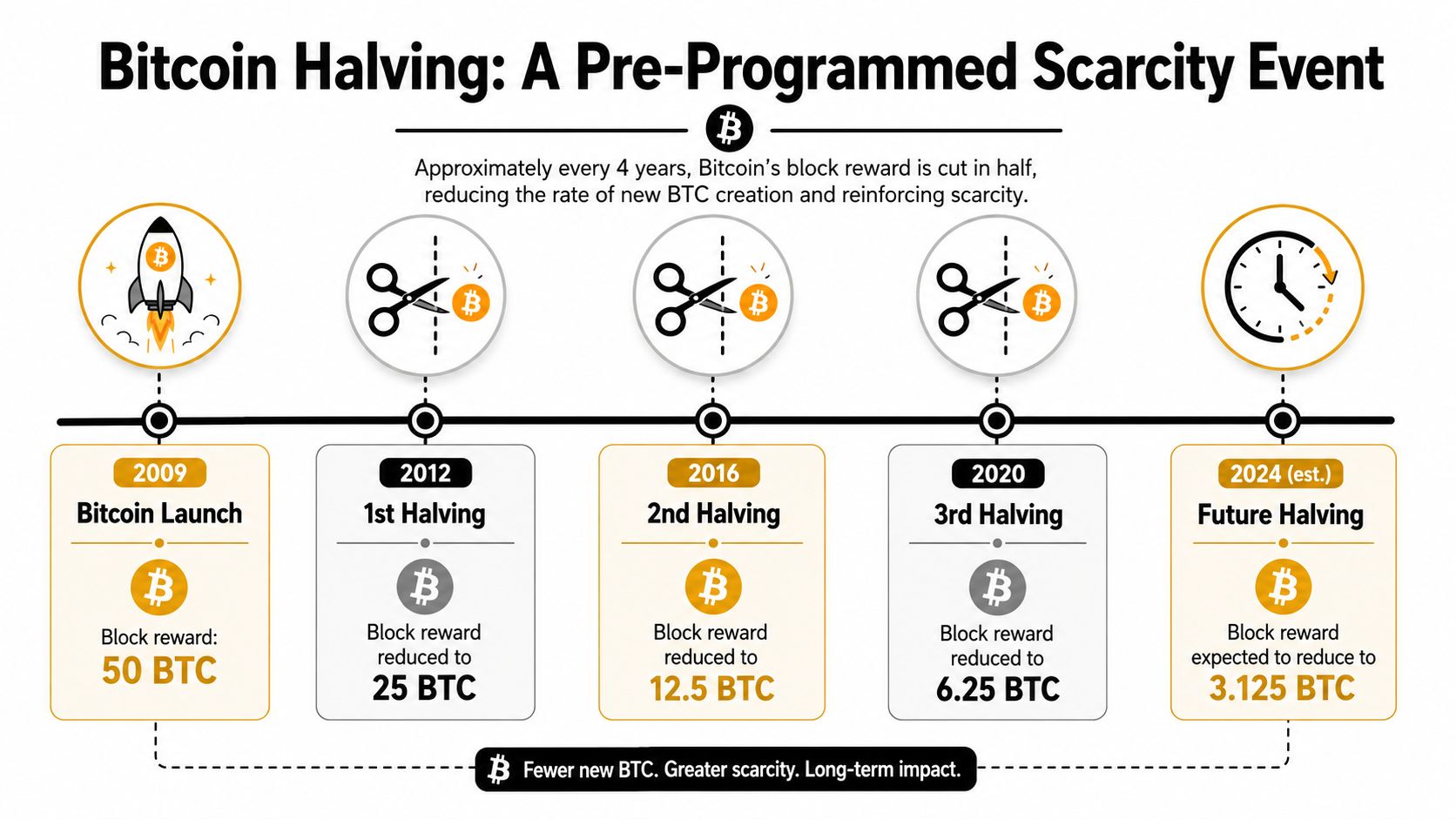

It uses a rule called the halving. If the 21 million cap is the endpoint, the halving is the metronome that sets the pace. About every four years, the amount of new bitcoin awarded to miners for adding a block is cut in half. The system keeps producing blocks, but the flow of new coins gets smaller in clear, scheduled steps.

A faucet that keeps tightening

A faucet is a useful comparison here. Early in Bitcoin's life, the tap was wide open. Miners earned large block subsidies, so new supply entered circulation quickly. Then the protocol tightened the faucet. It tightened it again at the next halving, and it will keep doing that until new issuance becomes tiny.

That design matters because it turns scarcity into a schedule instead of a promise. No central bank decides whether to speed issuance up or slow it down. The protocol applies the same rule every cycle, which is why halvings get so much attention from investors, miners, and long-term holders.

The market impact is easy to misunderstand. A halving does not guarantee a price jump. It changes the rate of new supply, not the level of demand. If demand stays steady or grows while fewer new coins reach the market, that shift can shape sentiment and price narratives over time. For readers following that side of the story, this guide on why Bitcoin is rising adds useful market context.

This explainer video gives a quick visual overview before we get to the table:

Bitcoin halving epochs and block subsidy reduction

One helpful reference for readers looking for key Bitcoin halving information is The Coin Course, especially if you want a plain-language recap of how these events are tracked.

| Halving Event (Year) | Block Height | Block Subsidy Before Halving (BTC) | Block Subsidy After Halving (BTC) |

|---|---|---|---|

| 2012 | 210,000 | 50 | 25 |

| 2016 | 420,000 | 25 | 12.5 |

| 2020 | 630,000 | 12.5 | 6.25 |

| 2024 | 840,000 | 6.25 | 3.125 |

A few practical observations matter here:

- Early issuance was front-loaded: Larger subsidies pushed a large share of Bitcoin's total supply into the early years.

- Later issuance becomes gradual: Each cut makes the remaining path to the cap longer and quieter.

- Miner economics keep changing: With every halving, transaction fees matter more relative to the block subsidy.

That last point is the one many casual explanations skip. The halving is not only a scarcity mechanism. It is also a training process for Bitcoin's future security model. As subsidies shrink, miners must rely more on fees paid by users who want their transactions included in blocks.

This is why the network can feel economically closer to "finished" long before the calendar reaches 2140. The date of the last fraction mined matters, but the more immediate shift is that new issuance stops being the main source of miner revenue. Over time, Bitcoin moves from a system secured largely by newly created coins to one secured more by user-paid fees. For investors, that transition says as much about Bitcoin's maturity as the hard cap itself.

The Long Countdown Bitcoin's Issuance Curve to 2140

What does it really mean to say Bitcoin will be mined until 2140 if the network may feel mostly finished much earlier?

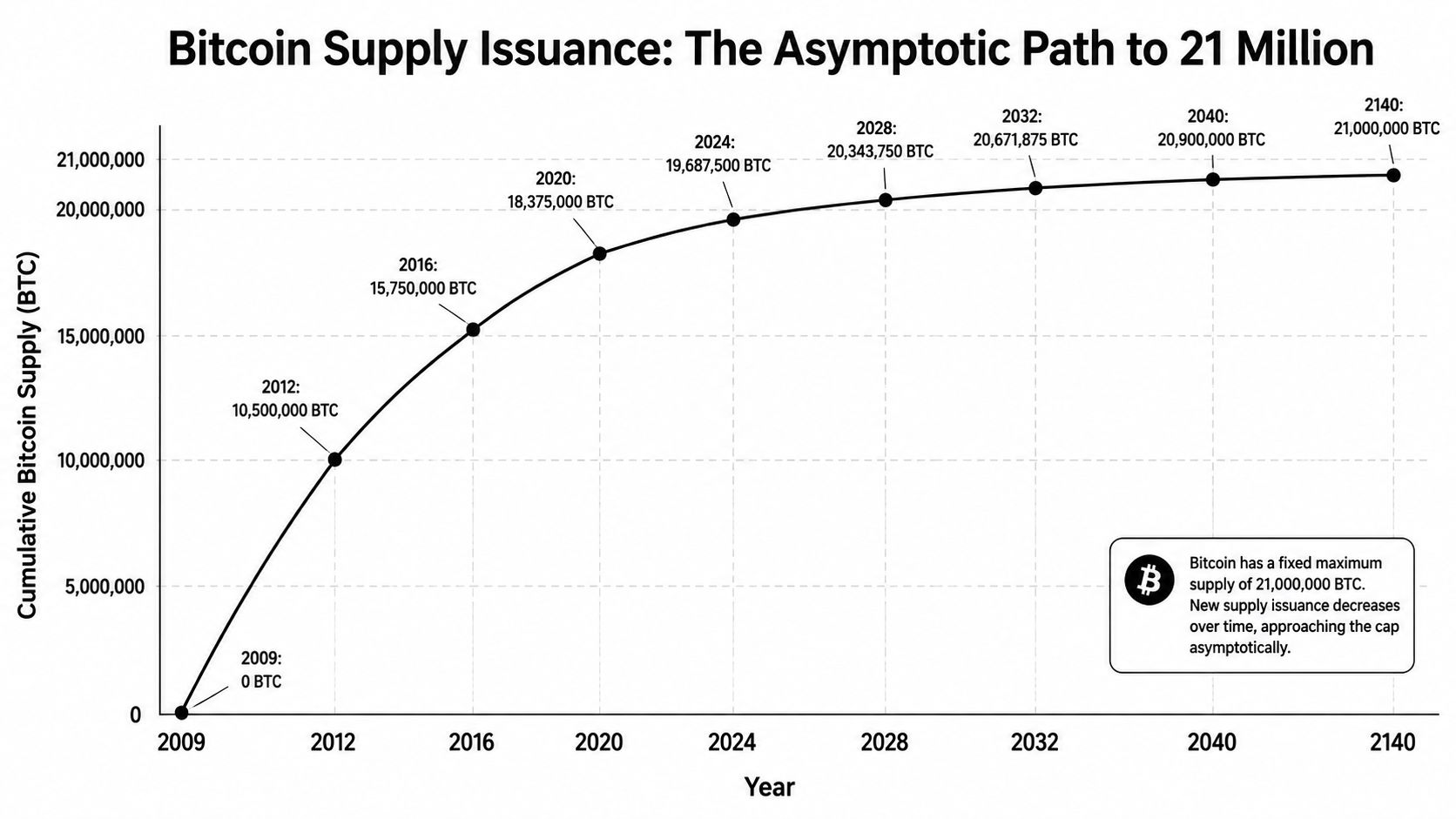

Bitcoin's issuance curve works like a faucet that starts wide open and then tightens every few years. In the beginning, new coins entered circulation quickly. Later, the flow slowed to a drip. That shape explains why the last stretch of issuance takes so long, even though most coins arrive far earlier.

A casual reader can easily miss what that implies. A long calendar runway does not mean a large amount of supply is still left to mine. In Bitcoin's case, the opposite is true. The schedule is front-loaded by design, so the final decades matter less for adding new coins and more for changing how the network pays for security.

Calendar completion versus economic completion

This distinction explains far more than the headline date ever does.

Calendar completion is the technical endpoint. It refers to the moment the final tiny fraction of a bitcoin is issued, which is generally expected around 2140. Economic completion happens earlier, when new issuance becomes too small to be the main force shaping miner incentives, market supply, and investor expectations.

Fortune noted that by 2035, about 99% of Bitcoin's total supply is expected to be mined in this Fortune analysis. The same publication also discussed why that leaves more than a century for the final sliver of issuance, which sounds dramatic on a calendar but looks much less dramatic in economic terms.

The current block subsidy is 3.125 BTC per block after the April 2024 halving, as shown in the Bitcoin protocol schedule summarized by Lightspark's explanation of Bitcoin's post-issuance model.

That is why 2140 can mislead people. It is the date of technical completion, not the date when new supply still feels large.

A useful analogy is a marathon where one runner covers almost the entire distance at a strong pace, then spends a very long time creeping through the final steps. The clock is still running, but the meaningful part of the race is mostly over. Bitcoin's supply curve behaves in a similar way. The last fraction takes an extremely long time to arrive, yet its economic weight keeps shrinking.

The supply story that matters most is not only "when is the last coin mined?" It is also "when does new issuance stop being the main support for miner revenue and market flow?"

Why 2140 matters less than most headlines suggest

For investors, the bigger transition is not a date on a distant calendar. It is the gradual handoff from subsidy-led security to fee-led security.

As the subsidy gets smaller, miner income depends more on users paying to get transactions confirmed. That change affects how analysts think about Bitcoin's long-term health. A mature network will need sustained transaction demand, settlement demand, or other forms of on-chain activity that create a durable fee market. Readers comparing mining models often run into simplified pitches, so it helps to separate Bitcoin's long-term security economics from services such as cloud mining platforms and hosted mining offers, which solve a very different problem.

Three practical implications follow:

- New supply matters less over time. Each halving reduces the market impact of freshly issued coins.

- Fees matter more over time. Miner incentives become tied more closely to actual network use.

- Lost coins matter more than many headlines admit. If some bitcoin never returns to circulation, effective supply can feel tighter than the official cap suggests.

This shift also connects Bitcoin to a broader payments and infrastructure story. If more economic activity settles through Bitcoin rails, the fee market has more room to grow. That is one reason institutions watching custody, settlement, and transaction infrastructure pay attention to the post-subsidy future, a theme that also appears in inabit's crypto gateway insights.

So yes, 2140 still matters. It marks the end of issuance on the protocol's calendar. But Bitcoin may feel economically close to "done" much sooner, because the role of new coins keeps shrinking long before the last fraction is mined.

Life After the Last Bitcoin The New Era for Miners

What exactly ends after the last bitcoin is issued?

Mining does not stop. The creation of new coins stops. Miners still compete to add blocks, order transactions, and secure the chain. The difference is economic, not mechanical. Bitcoin's calendar completion happens near 2140, but its economic completion arrives much earlier, as the subsidy becomes too small to matter much compared with the network's total value.

From subsidy-funded to fee-funded security

A useful way to picture the shift is to compare Bitcoin mining to a new toll road. Early on, the road operator offers large subsidies to attract builders and keep the system running. Over time, those subsidies shrink, and the road has to support itself through actual traffic. Bitcoin works in a similar way. In the early decades, miners were paid mostly with newly issued bitcoin. In the later decades, they must earn more of their revenue from transaction fees.

Lightspark's explanation of the post-issuance model outlines this endpoint clearly. After the subsidy falls to zero, miner compensation comes from fees attached to transactions in each block. That is the destination Bitcoin was designed for from the start.

The harder question is not whether this transition exists. It does. The harder question is whether fee revenue will be high enough, often enough, to support the level of mining security the network needs.

That is why 2140 can be a little misleading as a headline. Investors often hear it as a finish line. In practice, the more important period is the long approach to that date, when each halving makes new issuance less important and miner economics start to resemble the final model years or even decades in advance.

For readers comparing business models around mining, retail products such as cloud mining services for individual buyers answer a different question from Bitcoin's long-run security design. One is about access to mining exposure. The other is about how the protocol pays for block production after issuance fades.

Why fee markets become the real story

A fee-funded system changes what matters. Scarcity still matters, but usage matters more than many holders expect.

If block subsidies are the training wheels, transaction fees are the long-term engine. Fees appear when users compete for limited block space. The more valuable it is to settle on Bitcoin's base layer, the more miners can earn without relying on new coin issuance. That turns block space into something like premium settlement real estate. Small, routine activity may move elsewhere, while high-value transfers, final settlement, and time-sensitive transactions pay for inclusion on the main chain.

Several forces could strengthen that fee market:

- Layer 2 networks can push frequent, lower-value activity off the base chain while still settling important outcomes back to Bitcoin.

- Institutional settlement demand can make base-layer transactions more valuable even if the number of transactions does not rise dramatically.

- Custody, payment, and treasury infrastructure can increase the amount of economic value that eventually needs Bitcoin's final settlement layer.

- New financial uses for bitcoin can create periods where block space becomes more contested and therefore more profitable for miners.

One useful example comes from inabit's crypto gateway insights, which examine how crypto infrastructure is being built for operational finance, not only for speculation. That matters because miner revenue in Bitcoin's mature era depends less on the existence of bitcoin and more on how often people and institutions need the chain itself for settlement.

There is a trade-off here. If scaling works too well on upper layers, routine traffic may leave the base chain and reduce fee pressure. If Bitcoin becomes a widely used settlement layer for high-value activity, fewer transactions could still produce meaningful fees because each block carries more economically important transfers.

Investor lens: The late-stage Bitcoin question is not simply “Will all coins be mined?” It is “Will the network produce enough high-value demand for block space to fund security after new issuance fades?”

That is why the network may feel economically “done” long before the calendar says mining is over. By the time the final fractions of bitcoin are issued, the primary transition should already have happened. Miners will still mine, but the market will be paying them for security directly instead of receiving that security as a subsidy from new supply.

Frequently Asked Questions About Bitcoin's Future

Some of the most important questions about when all bitcoins will be mined show up at the edges. They're less about the headline date and more about how the rules behave when Bitcoin gets close to the end of issuance.

Could Bitcoin's 21 million cap ever change

In theory, software can always be changed. In practice, Bitcoin's cap is one of the most socially and economically defended rules in the network.

People don't treat the cap like a minor setting. They treat it like a core promise. Changing it would require broad agreement across the ecosystem, and it would cut directly against the very scarcity logic that gives Bitcoin much of its identity.

So the better way to think about this is not “can code be edited?” but “would the network accept a change that weakens Bitcoin's central monetary rule?” That's a much higher bar.

What happens when the reward gets too small

Bitcoin is divisible only to 8 decimal places, so the subsidy eventually falls to 1 satoshi and then reaches zero, which is why analysts describe the end of mining as effectively occurring around 2136–2140 rather than on a single precise day, as explained in Bitdeer's discussion of Bitcoin's final issuance phase.

After that point, miners still produce blocks, but they're compensated entirely by transaction fees. That's the same long-term shift discussed earlier, just viewed from the protocol's smallest unit.

Small technical details often explain big economic outcomes. Bitcoin's 8-decimal precision is one of them.

Do lost coins change the schedule

Lost coins don't change the issuance schedule. They change the effective supply people can access.

That's an important distinction. The protocol still follows its programmed path toward the cap. But if some coins are permanently inaccessible, the practical tradable supply can feel tighter than the official maximum suggests. That's one reason “21 million” and “available Bitcoin” aren't always the same idea.

For readers trying to think through long cycles and market psychology around scarcity, this guide to the cryptocurrency bear market helps frame how supply narratives interact with investor behavior.

Will Bitcoin still matter in a world of smart contracts and AI-linked crypto products

Yes, because Bitcoin's role doesn't depend on doing everything. It depends on doing a few things very credibly.

It can remain important as a scarce reserve asset, a settlement layer, and a monetary benchmark inside a wider crypto economy that includes DeFi, tokenized assets, AI-integrated applications, and Layer 2 networks. In that sense, Bitcoin's future may look less like an all-purpose app platform and more like a durable financial base layer.

The key idea is simple. The last Bitcoin being mined is not the moment Bitcoin becomes relevant or irrelevant. It's just the end point of a monetary schedule that has been shaping behavior all along.

If you want more plain-English analysis on Bitcoin, crypto market structure, Web3 trends, DeFi, and the risks behind the hype, explore Coiner Blog for deeper guides and ongoing commentary.