Cryptocurrency ramblings

Blockchain Identity Verification: The Ultimate 2026 Guide

Blockchain identity verification is moving from niche architecture to core digital infrastructure. The strongest signal isn't ideological. It's financial. The global Blockchain-Based Identity Verification market is valued at $3.8 billion in 2025 and is projected to reach $28.5 billion by 2033, growing at a 28.4% CAGR, according to DataIntelo's blockchain-based identity verification market analysis.

That kind of trajectory matters because identity sits underneath almost everything crypto wants to scale. DeFi onboarding. Sybil-resistant airdrops. NFT community gating. GameFi reputation. Real-world asset tokenization. Even AI agents will need some form of portable, cryptographic trust if Web3 is going to onboard mainstream users without rebuilding the same brittle identity silos that Web2 gave us.

The bullish case is real. So is the catch. A lot of crypto content treats decentralized identity as if legal recognition will arrive automatically once the tech works. It won't. The most investable insight in this category might not be the upside of DIDs and verifiable credentials. It might be the friction created when regulators, banks, exchanges, and courts move far slower than protocol builders.

Table of Contents

- Why Blockchain Identity Is Web3s Next Billion-User Onramp

- The Core Pillars of Decentralized Identity Explained

- The Architecture of Trust A Look Under the Hood

- Blockchain Identity Versus Traditional KYC

- Real-World Use Cases in Crypto NFTs and GameFi

- Privacy Regulation and the Adoption Dilemma

- The Future of Identity and How to Get Involved

Why Blockchain Identity Is Web3s Next Billion-User Onramp

Identity fraud and repeated KYC failures already cost the digital economy billions each year. Web3 still carries the same structural problem. Users keep handing passports, selfies, and proof-of-address files to every exchange, off-ramp, wallet-linked service, and fintech app that asks.

The broken economics of centralized identity

Centralized identity systems create high-value data honeypots. A single provider often stores passports, addresses, banking details, sanctions screening results, selfies, and compliance histories in one stack. One breach can expose everything needed for account takeover, synthetic identity fraud, or long-tail financial abuse.

The operational cost is just as damaging. Platforms pay to collect and secure sensitive documents. Users pay in duplicated onboarding, higher exposure, and almost no portability between services. Crypto was supposed to reduce intermediaries, yet identity remains one of the most duplicated and expensive intermediated layers in the stack.

Practical rule: If a product asks users to upload the same personal documents again and again, it is increasing compliance overhead and widening the attack surface.

Why this matters for Web3 adoption

The fit with crypto is straightforward. Wallets already trained users to value direct control over assets and permissions. Identity follows the same path. Credentials can sit with the user, and a verifier can check a signed claim instead of collecting the raw document every time. For readers tracking the broader shift in ownership rails, that logic connects closely to what Web3 technology changes about ownership and control.

That model gets more relevant as Web3 expands into DeFi, tokenized real-world assets, stablecoin payments, and AI-linked services. A smart contract may not care who you are, but the application layer often does. Residency, age, accredited investor status, sanctions clearance, uniqueness, and institutional authority all affect what a user should be allowed to do.

This is the part many bullish articles skip. The technology is moving faster than the legal system. A protocol can support DIDs and verifiable credentials today, but regulators, courts, and compliance departments often still require familiar documents, legacy databases, and human review. That lag matters for investors and builders because adoption will not depend on product quality alone. It will depend on whether credential formats, issuers, and verification flows gain real legal recognition in major jurisdictions.

So yes, blockchain identity can reduce friction for users and lower data-handling risk for platforms. But the path to a billion users is not just a technical rollout. It runs through policy, standards bodies, and regulated institutions that move far slower than crypto markets. That mismatch is the under-discussed risk, and it is also why the upside is so large if a few identity standards cross from technical acceptance into legal acceptance.

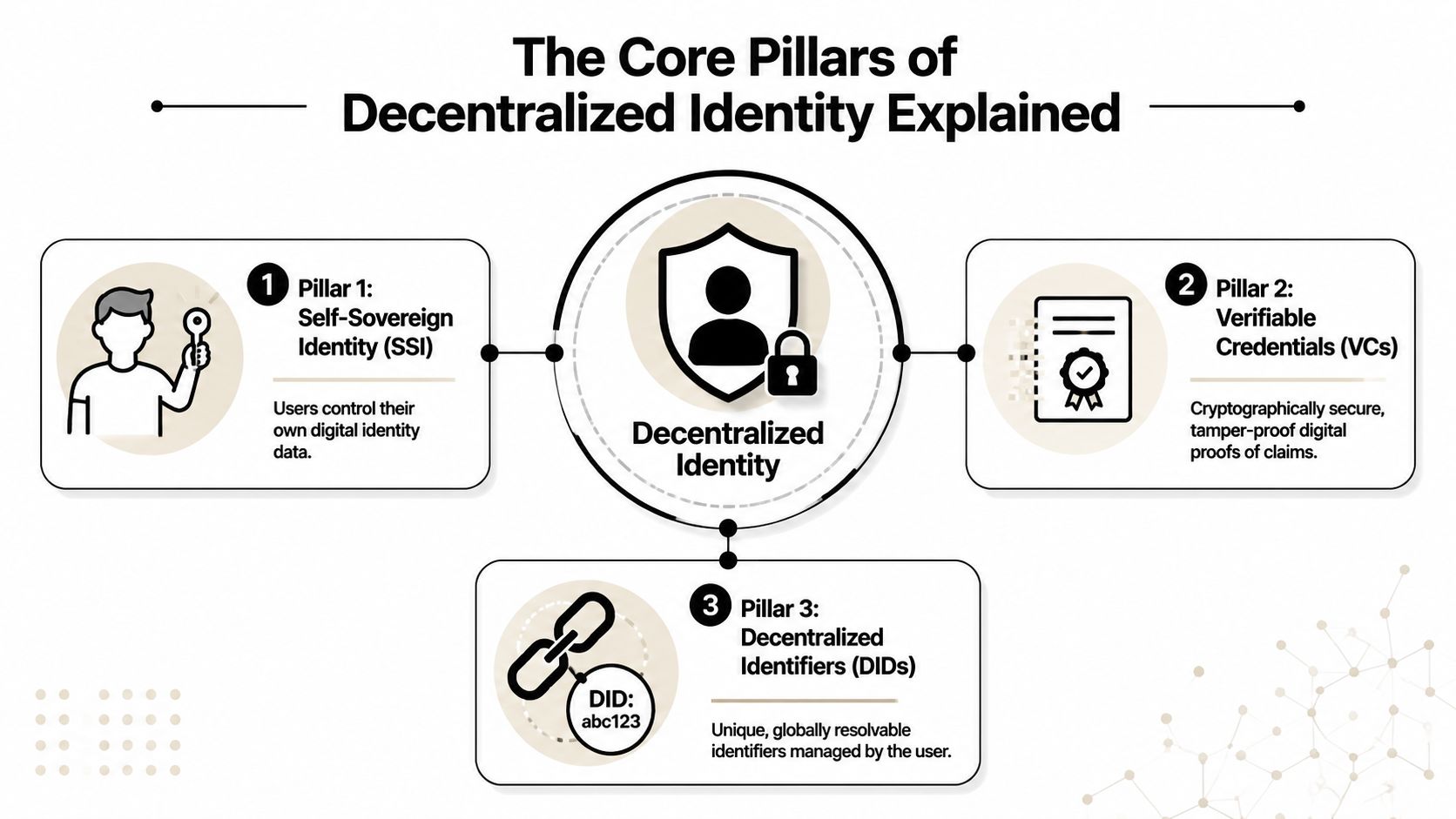

The Core Pillars of Decentralized Identity Explained

Decentralized identity rests on three core concepts: Self-Sovereign Identity (SSI), Verifiable Credentials (VCs), and Decentralized Identifiers (DIDs). Get these three pieces right, and the rest of the stack becomes much easier to evaluate, both as technology and as an investment theme.

The three concepts that matter

Self-sovereign identity (SSI) defines control. The user holds the identity relationship, decides which credentials to keep, and chooses what to present to a verifier. In practice, that means identity starts to work more like key custody than account registration.

Verifiable Credentials (VCs) are the signed claims. A diploma, proof-of-age credential, KYC attestation, employee badge, or DAO membership credential all fit the model. The important point is not the document format. It is the issuer's signature, which lets another party verify authenticity without calling the issuer every time.

Decentralized Identifiers (DIDs) are the cryptographic identifiers that route trust. They point to the keys and metadata needed to verify signatures and establish control. For crypto-native readers, the intuition is close to not your keys, not your coin. If a platform controls the identity layer, it can still gate access, freeze permissions, or force repeated checks.

A practical way to separate the roles looks like this:

- SSI is the control model. It answers who governs the identity relationship.

- VCs are the claims. They carry the facts a user may need to prove.

- DIDs are the coordination layer. They connect issuers, holders, and verifiers through cryptographic references.

That distinction matters because many projects market "decentralized identity" while only decentralizing one layer. A wallet with credentials but no portable identifier is limited. A DID with no trusted issuer network is just an identifier. A credential standard with no user control starts to look like old KYC in a new wrapper.

A quick visual helps if you want to see the framework in action.

How the verification flow works

The technical flow is straightforward. A holder presents a credential. The application checks the issuer's digital signature. It then resolves the DID document to find the public keys or service endpoints needed for verification. Under W3C DID and VC standards, that process can happen cryptographically instead of through repeated manual review.

That changes the economics of compliance and access control. The verifier does not need to store every raw document or re-run the same identity checks from scratch for every interaction. It only needs confidence that a trusted issuer signed a valid claim and that the claim still meets the policy requirements.

Zero-knowledge proofs make the model more useful. A user can prove they are over an age threshold, reside in an approved jurisdiction, or hold an eligibility credential without exposing the full underlying document. That is a better fit for Web3 products that need selective disclosure, especially in DeFi, gaming, and tokenized asset platforms.

The catch is adoption. The cryptography already works, but legal and institutional acceptance still lags in many jurisdictions. Builders can ship DID and VC flows today. Regulated entities may still ask for PDFs, database checks, and manual escalation. That gap is not a side issue. It determines how quickly these pillars move from strong infrastructure to recognized identity rails.

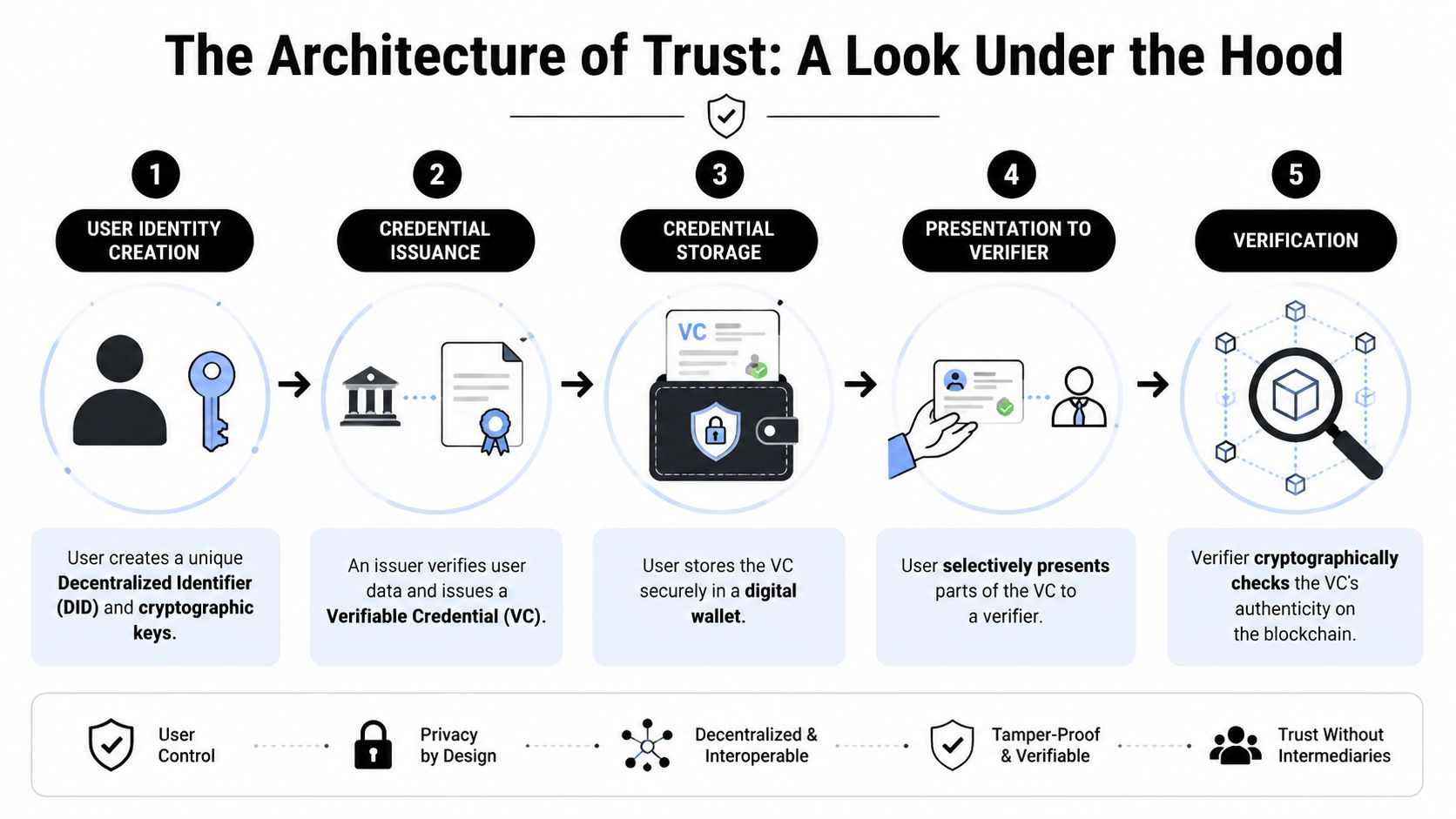

The Architecture of Trust A Look Under the Hood

Under the hood, decentralized identity is a trust triangle. One party issues a claim. One party holds it. Another party verifies it. Blockchain identity verification works because all three can coordinate cryptographically without relying on a central identity database to mediate every interaction.

The three actors that make the model work

Holder. This is the user, usually operating through a wallet. The holder generates or controls the DID and stores credentials locally or in a controlled wallet environment.

Issuer. This is the trusted entity that validates a fact and signs the credential. In practice that could be a bank, exchange, university, DAO admin layer, employer, or government-linked service.

Verifier. This is the application that needs confirmation. Think of a DeFi frontend checking sanctioned-jurisdiction restrictions, an NFT community checking membership credentials, or a tokenized RWA platform checking investor eligibility.

That separation matters. It prevents the verifier from becoming the custodian of every raw document.

A practical verification sequence

A standard architecture usually follows this order:

- Key creation. The user creates a DID and associated cryptographic keys.

- Credential issuance. An issuer verifies the user and signs a VC.

- Wallet storage. The user stores the credential in a digital wallet.

- Selective presentation. The user shares only the required credential data or proof.

- Verification. The verifier checks signatures, status, and validity against the relevant trust framework.

The trust guarantee comes from the ledger layer. The immutability of the distributed ledger ensures identity data can't be altered without consensus, creating an auditable record. Smart contracts can also automate verification logic, potentially reducing operational costs by up to 40% in financial sectors, according to this technical overview of blockchain-based identity verification.

That doesn't mean every identity project should write everything on-chain. In practice, mature designs keep sensitive personal data off-chain and use the ledger for public keys, revocation states, trust registries, or credential status checks. Builders who ignore that distinction usually create systems that are either privacy-hostile or operationally clumsy.

If you want a deeper foundation in the security side, it helps to understand the future of cryptography in blockchain systems, because decentralized identity is really applied cryptography wrapped in UX.

The architecture is powerful, but only when teams keep the chain focused on verification and integrity. Putting too much raw identity data on a ledger is usually a design smell, not a feature.

Blockchain Identity Versus Traditional KYC

Traditional KYC was built for institutions, not users. That's why it feels repetitive, intrusive, and slow. Every bank, exchange, and fintech stack asks for the same documents, stores the same data, and recreates the same verification burden in isolation.

Where the old model breaks

The old model has two structural weaknesses. First, it creates centralized repositories full of sensitive data. Second, it makes identity non-portable. A user who already proved who they are to one trusted institution often has to start from zero somewhere else.

Research highlighted by IBM Blockchain found that implementing blockchain-powered PKI systems can reduce the risk of identity theft by up to 70% by removing the single points of failure common in centralized databases, as summarized in Spydra's review of blockchain identity and KYC compliance.

That doesn't make blockchain identity a magic compliance pass. It does show why the architecture is attractive. It changes where risk accumulates.

For readers who want a grounded primer on why this problem matters outside crypto bubbles, Matil has a useful piece on the importance of identity verification, especially if you're thinking about fraud control and onboarding integrity in practical business terms.

Side-by-side comparison

| Feature | Traditional KYC | Blockchain Identity (SSI) |

|---|---|---|

| Data control | Institution-controlled | User-controlled |

| Storage model | Centralized databases | User wallets plus distributed verification rails |

| Verification flow | Repeated manual or semi-manual checks | Reusable cryptographic proofs |

| Privacy | Often requires broad disclosure | Supports selective disclosure |

| Portability | Low | High |

| Breach profile | Large honeypots | Reduced central aggregation risk |

| User experience | Repetitive onboarding | Credential reuse across services |

| Automation potential | Limited by siloed systems | Strong alignment with smart contracts and Web3 apps |

The hidden cost in traditional KYC isn't just delay. It's duplication. A compliance team reviews a user, stores documents, and builds internal trust that rarely transfers cleanly outside that institution. Blockchain identity verification turns that one-off process into a reusable trust object.

There are trade-offs, of course:

- Recovery is harder. If users lose wallet access, identity recovery becomes a product problem, not just a password reset.

- Interoperability still varies. Standards exist, but implementation quality doesn't.

- Institutions may resist. Some firms prefer owning the identity relationship because it preserves data advantage.

The result is clear. Traditional KYC works, but it scales badly. SSI-based identity models fit the internet better, and they fit crypto far better.

Real-World Use Cases in Crypto NFTs and GameFi

Speculation gets the headlines, but identity is what makes crypto systems hold up under repeated use. In NFTs and GameFi, the practical question is simple: can a protocol tell the difference between a real participant and a disposable wallet without pushing everyone through heavy onboarding?

Airdrops are the clearest example. Teams want broad distribution, but they also need to limit wallet farming, regional violations, and scripted participation. Verifiable credentials give them a narrower tool than full KYC. A user can prove uniqueness, residency status, or prior contribution without exposing a full document stack. That changes token distribution from a spam contest into a rules-based allocation system.

NFT communities face a similar problem, but with social trust instead of token eligibility. Allowlists, gated Discord roles, IRL event access, and governance permissions all work better when tied to reusable attestations rather than snapshots of wallet balances. For readers tracking the ownership side of that equation, this guide on how NFTs work in practice helps frame why identity becomes more useful once ownership, access, and reputation start to overlap.

GameFi is where the identity thesis gets more interesting. A serious game economy needs memory. It needs to know whether a player has a tournament history, a cheating record, moderator status, or earned achievements that should travel across publishers and chains. Wallets alone are weak containers for that. Credentials make persistent reputation possible while keeping personal data off the public surface.

Speed matters here. If verification takes minutes, users drop. If it happens in the background with cryptographic proofs, identity becomes part of gameplay and market access rather than a separate compliance event.

A useful signal comes from outside the usual crypto pitch deck. In a ridesharing system built on a permissioned blockchain with zero-knowledge proofs, researchers reported an average verification time of approximately 239 milliseconds per proof in this safe ridesharing identity verification paper. That kind of latency is fast enough for real-time trust checks. Web3 applications need that if they want identity to support trading, matchmaking, gated access, or fraud controls without breaking user flow.

The strongest near-term use cases are practical:

- Airdrops and token claims. Projects can filter likely Sybil clusters, confirm region-based restrictions, and reward prior contributors with auditable criteria.

- NFT membership systems. Communities can issue credentials for moderators, creators, collectors, and event attendees instead of relying only on token holdings.

- GameFi reputation rails. Games can carry anti-cheat history, rank, guild status, and achievement records across ecosystems.

- Tokenized RWA access. Platforms can verify investor attributes or jurisdiction claims while reducing unnecessary data exposure.

There is a catch that many bullish pieces skip. These systems can work at the product layer before they work at the legal layer. A game studio or NFT community can accept a credential because it controls the rules. Regulated counterparties move slower. That creates a real adoption gap for investors to watch, especially where identity claims start touching age checks, sanctions screening, or jurisdictional restrictions. Technical capability can arrive years before formal recognition.

Teams building in this category should plan for dual rails for longer than the market expects. One rail serves crypto-native users through wallets and credentials. The other satisfies platforms, regulators, and enterprise partners that still want conventional records and audit trails. That operational burden is not theoretical. It shows up in consent logging, data retention, and proof handling, which is why Operational evidence for GDPR matters once identity products move beyond demos.

The winners in NFTs and GameFi will not be the loudest identity brands. They will be the products that make abuse more expensive, make status portable, and keep one eye on the slower pace of legal acceptance.

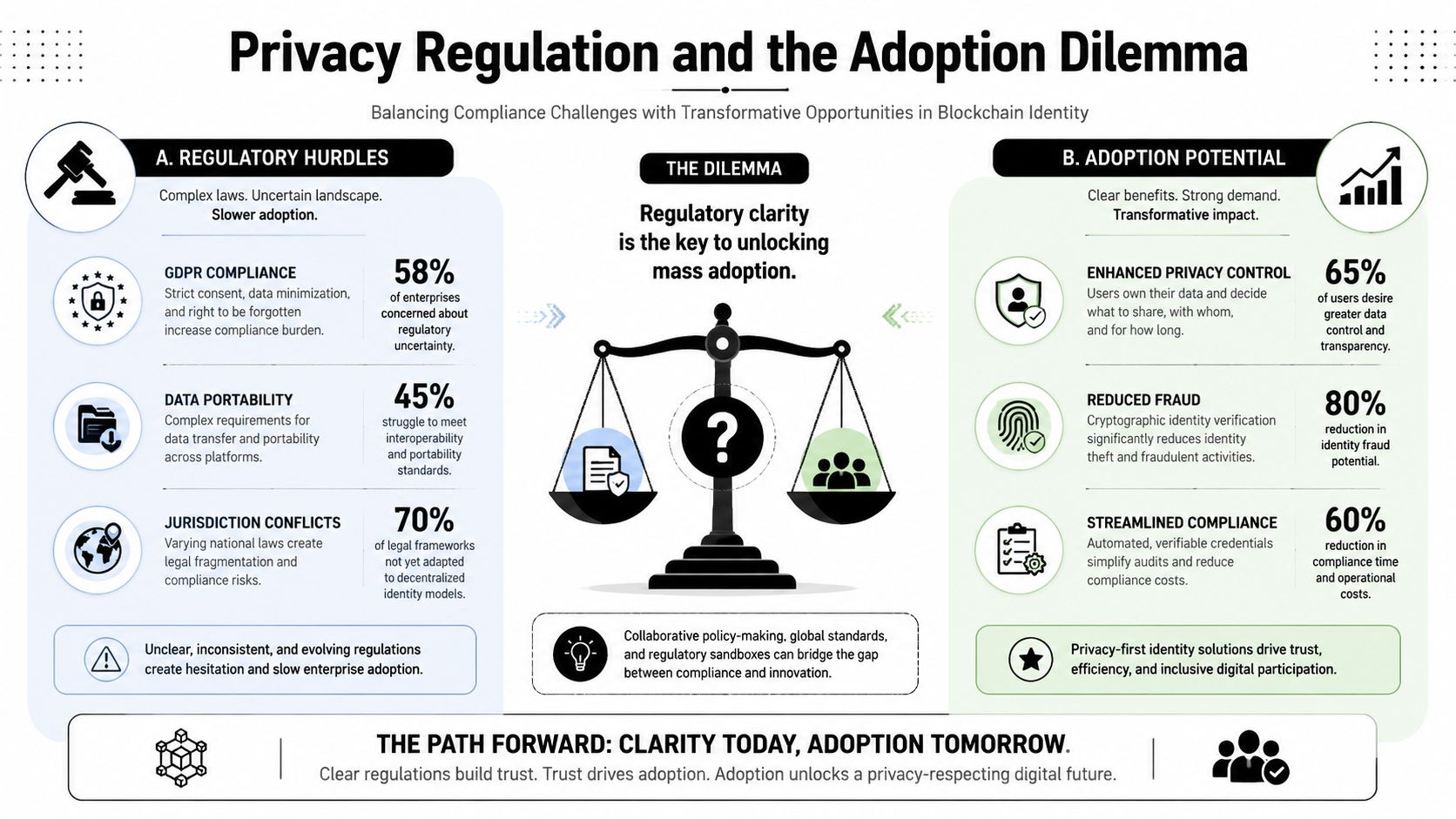

Privacy Regulation and the Adoption Dilemma

Most bullish identity theses get sloppy because teams often assume that if the technology is privacy-preserving and cryptographically sound, legal systems will treat it as equivalent to established identity frameworks. That assumption is too optimistic.

The market is early but the law is later

A 2025 OECD study found that 78% of major economies still lack legal recognition for DIDs as valid identity proofs, even though 90% of blockchain identity projects claim regulatory readiness, creating a meaningful adoption risk, as cited in Chainlink's discussion of digital identity verification in blockchain.

That gap matters more than most token investors realize. A protocol can build elegant DID tooling, polished wallets, and solid verifier rails. But if a regulator, bank partner, court, or compliance officer doesn't recognize that credential model as legally sufficient, the user still gets pushed back into legacy identity checks.

Reality check: Technical readiness and legal acceptance aren't the same milestone.

This is the under-discussed drag on the sector. It doesn't kill the thesis. It changes the timeline.

How to evaluate regulatory risk realistically

Privacy-preserving design still matters. Zero-knowledge proofs and selective disclosure fit the direction regulators say they want. Systems that minimize unnecessary data collection are often easier to defend than systems that hoard identity records. If you work in compliance-adjacent environments, it's worth reviewing practical operational evidence for GDPR because implementation proof usually matters more than abstract privacy promises.

There's also a security angle here. Regulatory ambiguity creates room for bad actors to market “compliant” identity products far too aggressively. Users and investors should apply the same skepticism they use elsewhere in crypto. This primer on how to avoid crypto scams is relevant because identity infrastructure can attract polished narratives with weak legal foundations.

A better diligence framework looks like this:

- Check jurisdiction first. Ask where the credential is meant to be accepted, not just where the protocol is deployed.

- Inspect the trust model. Find out who issues credentials, who can revoke them, and what legal weight that issuer carries.

- Separate privacy from recognition. A design can be elegant and still not count as valid identity proof in regulated workflows.

- Watch enterprise pilots carefully. The strongest signal is repeated use in real compliance environments, not a polished dashboard.

The next phase of blockchain identity verification won't be won by technology alone. It'll be won by projects that can bridge protocol design, standards, wallets, enterprise integrations, and legal recognition without pretending those are the same problem.

The Future of Identity and How to Get Involved

Identity infrastructure is moving toward the same place wallets and stablecoins already reached. It starts as a crypto-native tool, then becomes plumbing. The long-term upside is real, but the timing risk is easy to underestimate because legal recognition still moves far slower than protocol development.

That mismatch matters.

The teams most likely to matter are building identity as a modular service that plugs into wallets, DeFi, tokenized real-world assets, AI agents, and Layer 2 networks. Technical composability is improving fast. Regulatory acceptance is not. For anyone allocating time or capital here, that gap should shape expectations more than product demos do.

Where the stack is heading

AI plus crypto is one obvious frontier. Autonomous agents, marketplaces, and machine-to-machine services need verifiable identity for the same reason human users do. If an agent can sign messages, move funds, or trigger contract logic, counterparties need to verify who deployed it, what authority it has, and whether its history means anything. A DID can help represent that context, but only if the relying party accepts the credential format and the issuer behind it.

Layer 2 scaling will decide whether identity becomes default infrastructure or remains a niche feature. Verification flows that are expensive, slow, or awkward will not survive contact with consumer apps. As wallets and applications shift to cheaper execution environments, identity checks can run more often and with less user friction. That creates room for reputation systems, gated access, and reusable attestations that would be too clunky on higher-cost rails.

Tokenized real-world assets could be the strongest commercial driver. RWA platforms need investor qualification, jurisdiction checks, sanctions screening, and transfer restrictions. Verifiable credentials are a better fit than copying legacy databases onto a chain because they let platforms confirm eligibility without exposing the full identity record every time. But this is also where regulatory adoption lag hits hardest. A credential can be cryptographically sound and still fail in a regulated workflow if a transfer agent, regulator, or court does not recognize it.

DeFi is heading in the same direction. As the sector matures, protocols will compete on trust design and access control as much as yield. Identity primitives can help protocols support undercollateralized lending, permissioned pools, and reputation-aware participation. The catch is simple. Privacy-preserving design does not remove the need for legal clarity when assets, disclosures, and restricted users are involved.

What builders users and investors can do now

Follow the projects shipping real tooling, not just the projects selling a future. SpruceID, Ceramic Network, and Lit Protocol are worth tracking because they sit in different parts of the stack, including credential issuance, data coordination, and programmable access control. The point is not to pick mascots. It is to understand where durable value may sit if identity becomes infrastructure rather than a feature.

A practical approach looks different for each group:

- For builders. Test wallet-based credential flows, selective disclosure, and verifier logic in products that people already use. Focus on issuer trust, revocation handling, and fallback paths for jurisdictions that still require traditional checks.

- For users. Try the wallet and verifier experience yourself before trusting the marketing. Good identity UX should make credential reuse clear, privacy settings legible, and failure states easy to understand.

- For investors. Prioritize teams solving distribution, enterprise integration, and legal recognition. A polished DID demo is not enough if the credential has no accepted role in a real transaction flow.

- For researchers. Track standards convergence across DIDs, VCs, wallets, smart contracts, and cross-chain systems. Also track policy shifts. In this category, one regulatory memo can matter as much as a protocol upgrade.

My view is straightforward. Identity may not become the loudest crypto narrative, but it has a credible path to becoming one of the decade's more valuable infrastructure layers. The technical case is strong. The commercial case is forming. The legal case is still catching up, and that lag will determine which projects create durable value and which ones stall at the pilot stage.

Coiner Blog covers the crypto infrastructure shifts that matter before they become obvious headlines. If you want more sharp analysis on Web3, DeFi, NFTs, GameFi, AI-integrated crypto, and the next generation of blockchain rails, follow Coiner Blog for new guides and market commentary.