Cryptocurrency ramblings

Stablecoin Regulation: A Global Explainer for 2026

By August 2025, the global supply of fiat-backed stablecoins had reached approximately $238 billion, more than 60 times its value at the beginning of 2020, according to the Visa Economic Empowerment Institute's stablecoin policy analysis. That single number changes how stablecoin regulation should be read.

Stablecoins are no longer a sidecar to crypto trading. They sit between bank deposits and blockchain rails, between centralized exchanges and DeFi, and between dollar liquidity and global internet-native payments. When a token that looks like digital cash becomes infrastructure, regulators stop treating it like a niche experiment.

That shift matters far beyond issuer legal teams. It affects how exchanges list assets, how Ethereum and Layer 2 applications design settlement flows, how tokenized real-world assets move on-chain, and how banks or credit unions decide whether to enter crypto-linked payments at all. The main story in 2026 isn't whether regulation is coming. It's that the market is now large enough that operational details decide who can compete.

Table of Contents

- The Unstoppable Rise of Stablecoins

- Understanding Stablecoins and Regulatory Concerns

- Deconstructing the US Regulatory Framework

- A Tour of Global Stablecoin Rules

- Impact on Issuers Exchanges and Traditional Finance

- How Stablecoin Rules Affect DeFi and Web3

- The Road Ahead and Compliance Best Practices

- Stablecoin Regulation FAQs

The Unstoppable Rise of Stablecoins

Fiat-backed stablecoins reached about $238 billion by August 2025, up more than 60x from the start of 2020, according to analysis cited earlier from Visa. Growth at that scale explains why policymakers stopped treating stablecoins as a niche crypto product and started treating them as payment infrastructure with potential spillovers into markets, custody, and consumer protection.

Their role has expanded far beyond exchange settlement. Stablecoins now sit at the center of crypto market plumbing, serve as collateral and quote assets across trading venues, and provide the cash leg for many on-chain transactions. For payment firms, they offer faster blockchain-based transfer rails. For DeFi protocols, they function as base liquidity. For banks and credit unions, they raise a different question: whether blockchain-based dollars become a deposit substitute, a settlement tool, or both.

Why this growth changed the policy debate

The market is also highly concentrated. Visa's earlier analysis notes that USD stablecoins make up more than 90% of the global market, with nearly all outstanding stablecoins denominated in dollars. That concentration gives U.S. rulemaking effects far outside U.S. borders.

A reserve rule written for a U.S. issuer can alter liquidity conditions on offshore exchanges. A redemption standard can change how a DeFi protocol evaluates collateral quality. A custody requirement can determine whether a regional credit union views stablecoin access as a treasury opportunity or a compliance burden.

This is the strategic point many summaries miss. Stablecoin regulation is not only about issuer licensing. It is also about who gets distribution, who bears compliance costs, and which institutions become trusted gateways between tokenized dollars and the banking system.

Stablecoin rules increasingly function as rules for dollar-based internet finance.

Why regulators focused on stablecoins first

Regulators usually treat volatile cryptoassets as investment products or speculative instruments. Stablecoins create a different policy problem because they are marketed around reliability, redemption, and short-term liquidity. Users do not approach them like they approach bitcoin. They expect something closer to cash, even when the legal claim is much weaker than a bank deposit.

That is why policy frameworks have centered on familiar controls such as 1:1 reserve backing, asset quality, redemption rights, and limits on yield-like features, as noted earlier in the same Visa analysis. The objective is practical. If a token is used like money, supervisors want its reserves, disclosures, and operational controls to behave more like those of a payment product than an experimental crypto instrument.

The market impact differs by participant. Large issuers can spread compliance costs across scale. Exchanges must reassess listing, custody, and treasury practices token by token. DeFi protocols face indirect pressure because their core liquidity often depends on a small number of centrally issued stablecoins. Smaller financial institutions, including credit unions, may see an opening in custody, payments, or member services, but only if they can absorb vendor risk reviews, sanctions controls, and liquidity management requirements.

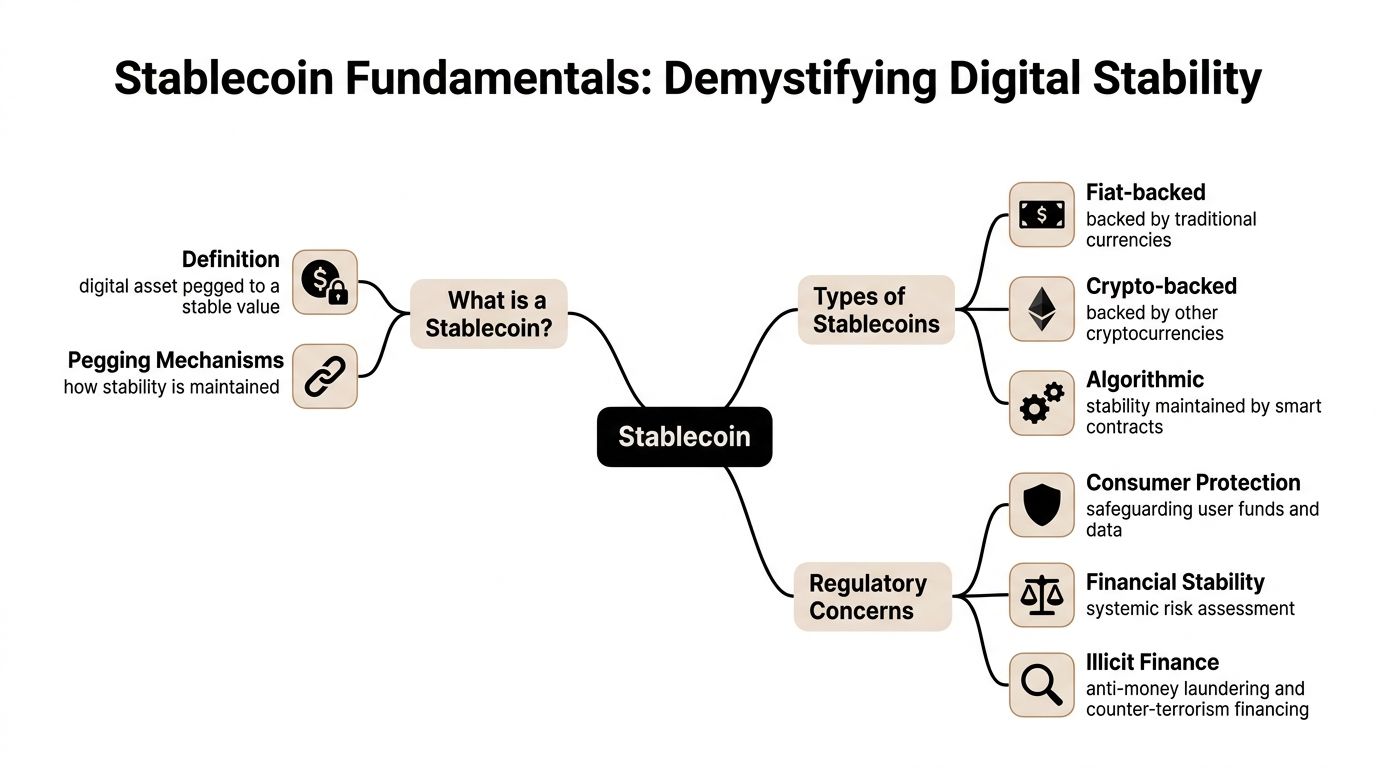

Understanding Stablecoins and Regulatory Concerns

A stablecoin is a blockchain-based token built to hold a reference value, usually a national currency such as the U.S. dollar. The simple definition hides a harder regulatory question. What matters in practice is not the label, but the mechanism that is supposed to keep the token stable during stress, redemptions, and market fragmentation.

The distinction is operational.

A fiat-backed stablecoin depends on an issuer, reserve manager, custodian, and legal redemption process. That model is usually easiest for supervisors to assess because the core issues resemble traditional payments and stored-value regulation. Are the reserves segregated, liquid, and available when holders ask for cash?

A crypto-backed stablecoin shifts more of the stabilizing logic on-chain. Collateral ratios, liquidations, and issuance rules can be visible in code, which appeals to DeFi protocols that need programmable collateral. But visibility is not the same as resilience. If the backing assets are volatile, a sharp market move can force liquidations precisely when on-chain liquidity is thinning.

An algorithmic stablecoin relies mainly on supply adjustments, arbitrage incentives, or linked tokens rather than conventional reserve assets. Regulators treat this category with particular caution because stability depends heavily on market confidence. Once that confidence breaks, the mechanism can fail faster than disclosure documents can reassure users.

Those design differences explain why one legal framework rarely fits every token. A bank, a centralized issuer, a lending protocol, and a credit union may all interact with the same stablecoin, but they inherit different risks. The issuer faces reserve, disclosure, and redemption obligations. Exchanges must decide whether a token's controls are strong enough for listing and custody. DeFi protocols absorb indirect exposure through collateral eligibility, oracle design, and liquidity concentration. Credit unions considering stablecoin payments or custody services face a different problem set: vendor oversight, BSA and sanctions controls, member disclosures, and liquidity planning if redemptions spike.

Regulators stepped in because stablecoins sit awkwardly between payments, deposits, securities, commodities, and software. The policy concerns usually center on three questions:

- Can holders redeem at par, on time, and at scale?

- What happens to trading, lending, and payments if confidence in a major token breaks?

- Who is responsible for AML, sanctions screening, and transaction monitoring across wallets, exchanges, and smart contracts?

The reserve question connects all three. As noted earlier in the same Brookings explanation, recent U.S. rulemaking ties reserve quality directly to redemption reliability, segregation of assets, and periodic attestation rather than broad claims of backing. The practical point is straightforward. “1:1” is only meaningful if the assets are liquid, legally ring-fenced, and available under stress.

That distinction has strategic consequences. Large centralized issuers can spread compliance costs across a bigger balance sheet and user base. Smaller issuers may find that monthly attestations, custody restructuring, and redemption operations are more expensive than the token itself appears to justify. For DeFi teams, the hard lesson is that on-chain composability does not eliminate off-chain legal dependencies. A protocol can automate collateral calls in seconds, but it cannot repair weak reserve management at a centralized issuer.

For traditional finance institutions, including credit unions, stablecoin risk assessment also looks different from ordinary crypto diligence. The key questions are less about price upside and more about operational dependency. Who controls minting and burning? How quickly can reserves be verified? What rights do end users have in insolvency? By Design Law Firm insights are useful on this point because stablecoin rules increasingly shape product design, partner selection, and treasury operations, not just legal disclosures.

The clearest takeaway is that stablecoins are regulated according to how they function under pressure. A token used as cash-like settlement infrastructure will attract scrutiny closer to payments and prudential supervision than to speculative crypto trading, even if the user experience still feels like a simple wallet transfer.

Deconstructing the US Regulatory Framework

Dollar-backed stablecoins sit at the center of the market, so U.S. rulemaking affects far more than domestic issuers. It shapes where liquidity forms, which intermediaries will support a token, and how quickly a stablecoin can move from crypto trading pair to payment rail.

In July 2025, the United States enacted the Guiding and Establishing National Innovation for US Stablecoins Act, or the GENIUS Act. As noted earlier, the statute creates the first federal framework focused specifically on payment stablecoins and sets a transition period before the regime is fully in force.

The practical significance is easy to miss. The law does not just define what reserves should look like. It shifts stablecoin issuance closer to regulated payments and prudential supervision, especially where a token is marketed as cash-like, redeemable at par, and suitable for broad transactional use.

What the GENIUS Act changed

The statute imposes three core disciplines.

First, it narrows the range of acceptable reserve structures. Issuers are expected to hold permitted high-quality liquid assets and maintain redemption arrangements that work in practice, not only in offering documents. That raises the bar for treasury operations. An issuer now has to prove that reserves remain liquid under stress, that custody and segregation are clear, and that redemption rights are operationally real.

Second, it places issuers inside the Bank Secrecy Act perimeter. For crypto firms, that means anti-money laundering and sanctions controls become part of the product itself. Customer identification, transaction monitoring, suspicious activity escalation, recordkeeping, and board-level oversight are no longer optional design choices.

Third, it adopts a dual federal-state model. That structure reflects U.S. institutional reality more than regulatory theory. Federal standards create consistency, while state supervisors and chartering paths still matter for licensing strategy, examinations, and day-to-day oversight.

That mix has uneven effects across the market.

A large issuer with established banking, legal, and treasury teams can spread those costs across a large circulation base. A smaller issuer may find that reserve management, independent review, reporting cadence, and redemption staffing compress margins quickly. For credit unions and regional financial institutions considering tokenized deposit substitutes or branded stablecoin partnerships, the question is less whether stablecoins are interesting and more whether the institution can support the operational controls that the law assumes.

What compliance looks like in practice

Compliance under the GENIUS Act starts long before a token launch. The hard work sits in entity design, vendor oversight, reserve operations, and user redemption flows.

Key pressure points include:

- Reserve management: Treasury teams need policies for asset eligibility, concentration limits, liquidity ladders, and daily reconciliation.

- Redemption mechanics: Legal redemption rights must match actual cut-off times, banking rails, customer support capacity, and settlement procedures.

- AML and sanctions controls: Exchanges, custodians, and banking partners will test whether the issuer can evidence monitoring, escalation, and audit trails.

- Licensing posture: Issuers and distribution partners need to decide early which federal or state path fits the business model, because re-papering after launch is expensive.

- Third-party dependence: Custodians, transfer agents, and technology vendors become regulatory dependencies, not just service providers.

The same pressure reaches DeFi protocols, even if they never issue a stablecoin themselves. If a protocol relies on a centralized dollar token for collateral, settlement, or treasury management, U.S. compliance failures at the issuer level can become protocol-level liquidity and governance problems. That is a strategic point many teams still underprice.

A useful legal companion to this discussion is By Design Law Firm insights, which examines how the GENIUS framework can affect digital asset businesses with U.S. exposure.

The strongest position in this new framework may belong neither to the most aggressive crypto-native issuer nor to the largest bank. It may belong to firms that can combine conservative reserve design, credible compliance operations, and distribution partnerships without making redemption slower or more expensive for end users. In the U.S., stablecoin regulation is becoming a test of operational credibility.

A Tour of Global Stablecoin Rules

Stablecoin rules are now active or taking shape across many major financial centers, but the result is not a single global standard. The closer reality is a patchwork of regimes that agree on reserve quality and redemption, while differing sharply on issuer eligibility, distribution rights, and the role of banks versus nonbank fintechs. For firms expanding across borders, those differences shape operating costs more than the headline policy goals do.

Where rules are starting to align

Across major jurisdictions, regulators are converging around a familiar core. Stablecoins marketed as cash-like instruments are increasingly expected to maintain high-quality reserves, segregate customer assets, honor redemption rights, and apply AML and sanctions controls. That shared baseline matters because it pushes issuers toward similar treasury and compliance architecture even when legal forms differ.

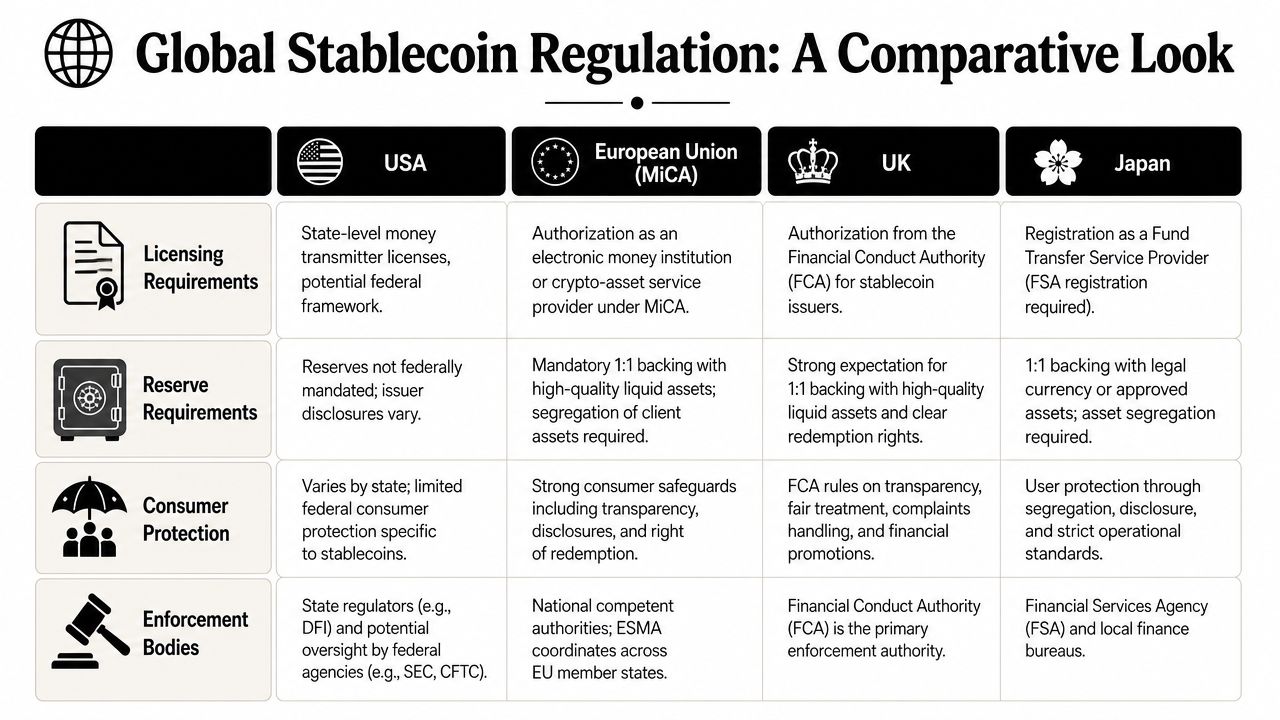

Hong Kong shows how detailed that baseline can become. Its Stablecoins Ordinance, implemented on August 1, 2025, requires licensing for fiat-referenced stablecoin issuers that distribute to the public, and it ties that license to face-value redemption, restrictions on paying yield, asset segregation, and control requirements around cybersecurity and financial crime, as outlined in BVNK's overview of global stablecoin regulations.

That convergence creates a strategic opening for some firms and a constraint for others. A large exchange group may be able to standardize reserve management across regions, but a DeFi protocol that depends on several third-party stablecoins still inherits legal fragmentation at the token level. A credit union considering stablecoin-enabled payments faces a different problem. It may not want to issue a token at all, but it still needs banking partners, custody arrangements, and settlement workflows that fit local rules and examiner expectations. Teams evaluating those dependencies often start with practical infrastructure questions such as access to crypto-friendly banks for digital asset businesses.

Where the real divergence sits

The biggest differences are less about whether reserves should be safe and more about who gets to participate.

Some jurisdictions route stablecoins through existing e-money, payments, or banking laws. Others create a dedicated licensing category. Japan has taken a more institution-centered approach, with issuance tied closely to regulated financial entities. The European Union uses MiCA to place stablecoins into defined token categories with bloc-wide authorization and conduct rules. The UK is still building out its regime, which leaves firms planning for policy direction rather than settled implementation details.

Those choices have direct market consequences. A bank-led model may reduce perceived credit risk for supervisors, but it can slow product iteration and limit the number of eligible issuers. A bespoke licensing model can admit more fintech participation, but it also creates threshold questions around capital, governance, and redemption mechanics. For exchanges, this affects which tokens are realistic to list in each jurisdiction. For wallet providers, it affects whether local distribution triggers licensing, registration, or marketing restrictions. For DeFi protocols, legal fragmentation can turn a technically interoperable stablecoin into a geographically uneven collateral asset.

| Jurisdiction | Governing Law | Reserve Requirements | Issuer Licensing | Key Feature |

|---|---|---|---|---|

| United States | GENIUS Act | Full backing with high-quality liquid assets | Dual federal-state supervision | Bank secrecy and compliance obligations shape issuer operations |

| European Union | MiCA | Backing and redemption framework for regulated token categories | Authorization-based regime | Single framework across member states, with product classification built in |

| UK | Developing regime under financial services reforms | Reserve and redemption expectations are central | Authorization-focused approach | Direction is clear, but implementation details are still being finalized |

| Japan | National stablecoin framework | Conservative reserve and issuer model | Closely tied to regulated financial institutions | Strong institutional gatekeeping |

| Hong Kong | Stablecoins Ordinance | Redemption at face value without delay, zero yield on balances | HKMA licensing required for public distribution | Clear public-distribution trigger for licensing |

One conclusion is easy to miss. The hardest part of going global is often not reserve composition. It is distribution design. The same token can move across public blockchains without friction, yet the legal act of offering, marketing, redeeming, or integrating that token into local payment flows can trigger very different obligations depending on the jurisdiction and the institution involved.

That is why “global stablecoin strategy” now means choosing where to issue, where to market, who handles redemption, and which entity in the group bears compliance responsibility. Banks and credit unions also need to decide whether they are entering as issuers, distributors, custodians, or payment intermediaries, because each role carries a different regulatory burden. Visbanking on banks and crypto captures this pressure well from the banking side.

For crypto founders, the practical lesson is simple. Product architecture, treasury structure, and market-entry sequencing now need to be designed together. For DeFi teams, the less obvious lesson is that jurisdictional mismatch at the stablecoin layer can become a governance, liquidity, and collateral-risk problem long before any regulator contacts the protocol directly.

Impact on Issuers Exchanges and Traditional Finance

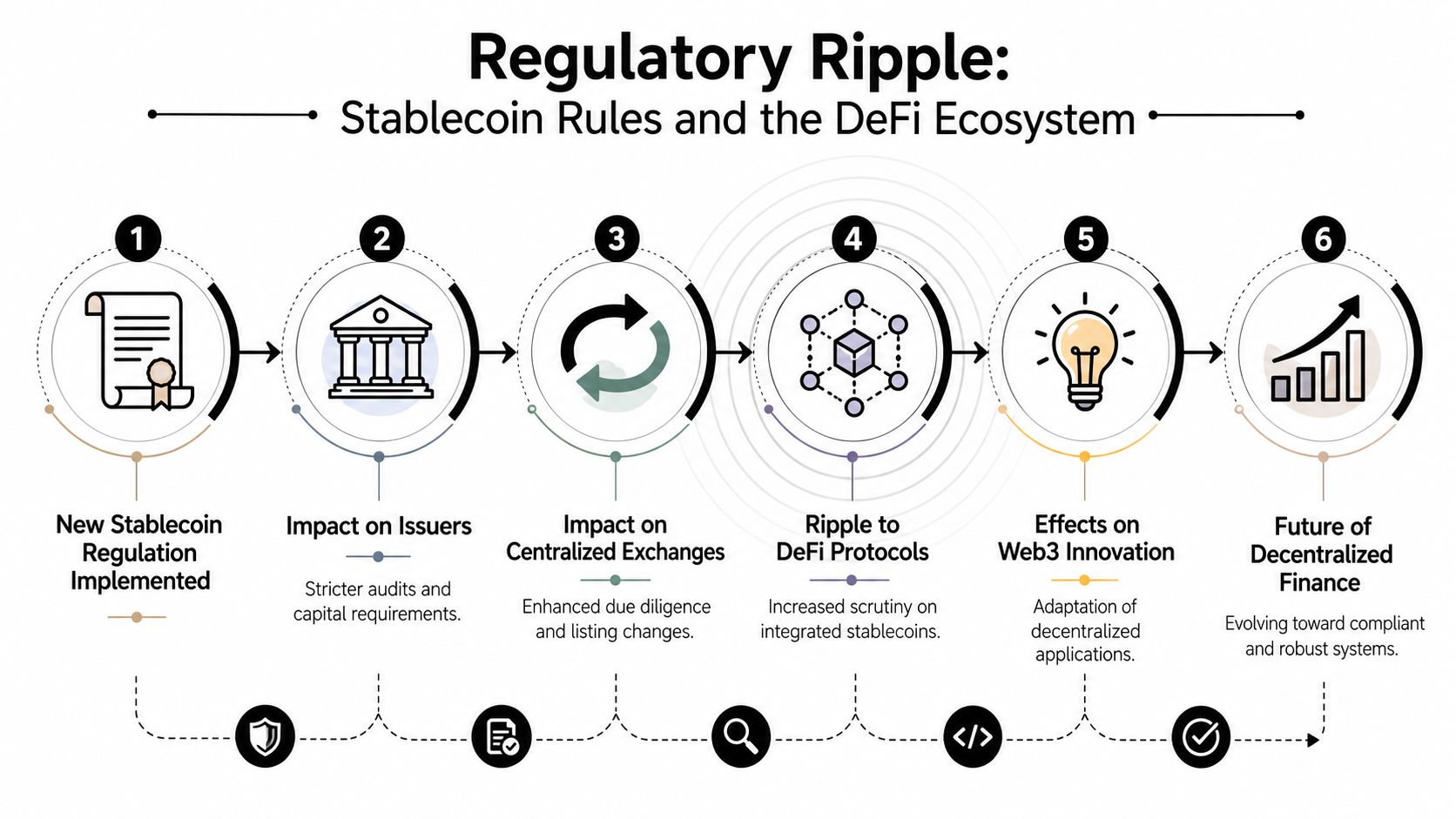

Stablecoin rules reshape the economics of issuance, distribution, and banking access. The firms under the most pressure are not only token issuers. Exchanges, custodians, payment intermediaries, banks, and credit unions all inherit new operating requirements once a stablecoin is expected to function like a regulated cash instrument rather than a loosely governed crypto asset.

For issuers, the hard part is no longer drafting policy language. It is building a treasury operation that can support daily redemption, reserve segregation, attestation, sanctions controls, and incident response at the same time. As noted earlier, proposed U.S. rules such as the GENIUS Act point toward reserves limited to cash and short-duration government assets, with tighter limits on riskier holdings. That pushes issuer finance teams closer to the center of the business. A stablecoin issuer increasingly resembles a narrow payments institution with a token wrapper, not a software company that happens to mint on-chain liabilities.

That shift affects competition. Scale will matter, but process discipline may matter more. An issuer with weaker reserve reporting or slower redemption operations can lose exchange support, banking relationships, and institutional users even before a regulator intervenes.

Exchanges face a different problem. Listing a stablecoin now requires more than checking market capitalization and trading demand. The exchange has to assess whether the issuer can keep reserves liquid, satisfy redemption requests, and continue serving users across multiple jurisdictions without sudden restrictions. In practice, legal due diligence and treasury due diligence are starting to merge. A stablecoin with strong volume but uncertain compliance posture can create delisting risk, customer support strain, and exposure to abrupt changes in deposit and withdrawal flows.

Three operational consequences stand out:

- Listing committees become more conservative. Reserve transparency, redemption mechanics, and issuer governance now matter as much as liquidity metrics.

- Banking dependency gets sharper. Stablecoin businesses need reliable fiat settlement, custody, and cash management. That is one reason the market for crypto-friendly banks has become strategically important.

- Counterparty concentration risk rises. If only a small group of banks, custodians, and market makers can support regulated stablecoins at scale, outages or policy changes at one provider can spread quickly through the stack.

Traditional finance reads these rules through a different lens. Large banks often see stablecoins as an extension of payments, treasury services, and commercial deposit relationships. Credit unions may see member demand and competitive pressure, but the path is narrower. They typically have less in-house capacity for digital asset custody, blockchain monitoring, real-time redemption workflows, and vendor oversight.

That creates an uneven playing field. A bank with established compliance, liquidity management, and payments infrastructure may be able to add stablecoin services as a new product line. A credit union may need to assemble that capability through partnerships, which adds vendor risk, contract complexity, and dependence on third-party controls. Visbanking on banks and crypto captures this institutional pressure from the banking side.

The strategic takeaway is easy to miss. New stablecoin rules do not only sort compliant firms from non-compliant firms. They sort institutions that can operationalize compliance from those that can only describe it. For issuers, that means treasury and redemption design are now core product decisions. For exchanges, it means stablecoin support is becoming a regulated counterparty decision. For banks and credit unions, it means the fundamental question is not whether stablecoins fit the business model, but whether the institution can support the control framework those tokens now require.

How Stablecoin Rules Affect DeFi and Web3

A large share of on-chain activity still settles in stablecoins. That gives stablecoin rules direct influence over how DeFi markets function, even where no single protocol operator controls execution.

When a lending market, automated market maker, perpetuals venue, or tokenized asset platform uses a centrally issued stablecoin as its base asset, it imports off-chain constraints into an on-chain system. Governance may be decentralized. The core settlement asset often is not. That distinction matters more as reserve rules, sanctions screening, redemption controls, and issuer supervision become more formal across major jurisdictions.

The new dependency inside on-chain finance

For developers, the practical question is no longer whether a stablecoin is liquid. It is whether that liquidity remains usable under changing compliance conditions.

A regulated stablecoin can improve market depth and make settlement assets more acceptable to institutions. That supports use cases such as tokenized Treasuries, real-world asset platforms, and payment rails built on smart contracts. Yet the same asset may carry blacklist authority, transfer restrictions, wallet screening, or jurisdiction-specific distribution limits. If those controls tighten, the effect reaches far beyond the issuer. It can alter collateral quality, liquidation behavior, routing logic, and even oracle assumptions across integrated protocols.

That turns legal design into a protocol design issue. Teams should test a few questions early:

- Asset dependency: If a core stablecoin changes redemption terms, blocks certain addresses, or loses support in a key market, what breaks first?

- Governance design: Can tokenholders or multisig operators replace collateral, update risk parameters, or shift liquidity incentives fast enough to matter?

- User disclosure: Do interfaces explain that a permissionless smart contract can still rely on an asset with centrally enforced controls?

- Treasury planning: Is protocol-owned liquidity diversified across issuers, chains, and cash-equivalent instruments, or concentrated in one regulated token?

Why decentralization debates get sharper

The policy tension is now operational, not philosophical. Web3 teams often optimize for open access and composability. Stablecoin supervisors optimize for traceability, redemption integrity, and control over illicit finance risk. Those priorities can coexist, but only up to a point.

A broader framework appears in regulating digital finance, which examines how public rules apply differently across protocols, intermediaries, and infrastructure. That distinction helps explain why two products with similar user experiences can face very different risk profiles. A front end that routes users into a pool containing a regulated stablecoin may face fewer issues than an issuer, but it still depends on policy decisions made elsewhere.

The result is likely to be stratification inside Web3. Protocols built around institution-friendly settlement assets may gain better access to payments, custody, and tokenized real-world assets. Protocols that require censorship resistance at the asset layer may move toward overcollateralized crypto-native stablecoins or synthetic structures, even if those options are less capital-efficient.

Credit unions offer a useful comparison. As noted earlier, these institutions may have legal room to participate but still face meaningful custody, vendor, and operational hurdles before they can support stablecoin activity at scale. DeFi builders should draw the same lesson. Formal permission to use a regulated token is much less important than having contingency plans for freezes, issuer concentration, and fragmented cross-border availability.

A DeFi protocol that uses a regulated stablecoin remains decentralized in some respects, but its reliability still depends on decisions made by issuers, supervisors, custodians, and payment intermediaries outside the codebase.

That is especially relevant for teams building settlement and merchant flows around tokenized payment infrastructure. The strategic work sits in the details: issuer terms, mint and burn mechanics, freeze authority, supported jurisdictions, bankruptcy remoteness of reserves, and the legal rights attached to redemption. In practice, the next phase of Web3 competition may turn less on raw composability and more on legal interoperability between protocols and the regulated assets they use.

The Road Ahead and Compliance Best Practices

The next chapter of stablecoin regulation will be defined less by whether reserve rules exist and more by who can manage the unresolved edges. Cross-border issuance, public-company restrictions, identity controls, and the meeting point between payment tokens and tokenized real-world assets are all still developing.

The hardest unanswered question

One of the least discussed constraints is how foreign or non-traditional issuers enter the U.S. market. The GENIUS Act prohibits public companies that are not predominantly engaged in financial activities from issuing stablecoins unless they clear a Stablecoin Certification Review Committee, and there is no public data on the approval process, according to Latham & Watkins' analysis of the GENIUS Act. That's more than a technicality. It creates a strategic barrier for foreign fintechs and Web3 startups that may have product expertise but not the right institutional profile.

For market participants, that suggests a likely future split. Some firms will build regulated payment tokens with conservative structures and deep compliance layers. Others will keep innovating at the protocol level, integrating regulated assets where necessary but avoiding issuer status.

Practical compliance habits for crypto teams

A balanced future is possible, but only if teams treat compliance as part of system design.

- Document reserve logic clearly: If your product touches a stablecoin, explain where stability comes from and what users can redeem.

- Audit both code and process: Smart contract reviews matter, but so do treasury procedures, custody controls, and incident response.

- Map counterparties early: Banks, custodians, exchanges, oracle providers, and market makers all shape your compliance exposure.

- Improve user transparency: Wallet interfaces and app disclosures should explain freeze risk, redemption limits, and jurisdictional constraints in plain language.

- Treat identity as infrastructure: Compliance-friendly onboarding doesn't have to kill UX if it's designed properly. Projects exploring blockchain identity verification are effectively working on one of the missing layers for regulated Web3.

A short visual briefing helps underscore how fast the policy environment is evolving.

The broader crypto ecosystem should resist two lazy conclusions. One is that regulation automatically kills innovation. The other is that decentralization makes regulation irrelevant. Stablecoins sit in the overlap. They use blockchain rails, but they make promises that law and balance-sheet quality still have to support.

Stablecoin Regulation FAQs

Are regulated stablecoins good for DeFi users

They can be. Regulated stablecoins may improve confidence around redemption and reserve quality, which helps protocols that need dependable liquidity. The trade-off is that these assets can also carry issuer controls that don't exist in purely permissionless designs.

Will algorithmic stablecoins disappear

Not necessarily, but they face a harder trust environment. Regulators are more comfortable with models tied to clear reserves and redemption rights. Algorithmic designs may still exist in crypto, especially in experimental or niche settings, but users will likely judge them more skeptically when comparing them with regulated payment stablecoins.

Do exchanges have to change how they list stablecoins

In practice, yes. Exchanges need to think about reserve transparency, licensing exposure, AML expectations, and whether a token's legal status fits the markets where users access it. Listing a stablecoin is becoming closer to listing a regulated financial product than listing a generic crypto asset.

Does this affect Bitcoin and Ethereum directly

Not in the same way. Bitcoin and Ethereum are not stablecoins, but stablecoin regulation affects the infrastructure around them. Trading pairs, collateral choices, Layer 2 settlement flows, DeFi liquidity, and tokenized asset markets often depend on stablecoins.

What should builders do first

Start with dependency mapping. Identify which stablecoins your product relies on, what rights the issuer has, what jurisdictions matter, and where off-chain controls can affect on-chain behavior. Then align legal review, smart contract design, and user disclosures before scale makes changes harder.

If you want more clear-eyed analysis on crypto policy, DeFi infrastructure, tokenization, and the practical side of blockchain adoption, follow Coiner Blog. It's a strong place to keep up with how regulation and real-world crypto markets are evolving without the hype.