Cryptocurrency ramblings

Tokenization in Payments: Secure Web3 & Crypto Assets

The technology behind a simple card-on-file checkout has become one of the clearest previews of the tokenized future crypto people talk about every day. Industry research cited by Spreedly projected that 35% of all transactions would be tokenized in 2025, and that tokenized transaction volumes would surpass 1 trillion globally by 2026 (Spreedly on payment tokenization). That's a useful reality check. Tokenization in payments isn't a niche security trick. It's already part of modern financial infrastructure.

For a Web3 audience, that should feel familiar. Traditional finance takes a sensitive real-world value, replaces it with a safer digital representation, and then lets trusted systems move that representation through a network. Crypto does something conceptually similar, but pushes the idea further with public blockchains, smart contracts, self-custody, and programmable assets.

That's why payment tokenization matters beyond PCI compliance. If you want to understand tokenized real-world assets, DeFi settlement, wallet UX, or the long path toward programmable money, it helps to understand how card networks solved one narrow but critical problem first.

Table of Contents

- The Hidden Link Between Your Wallet and Web3

- What Is Payment Tokenization Really

- The Engine Room How Payment Tokens Work

- Tokenization vs Encryption A Critical Distinction

- Unlocking Security and Reducing Compliance Headaches

- From Code to Checkout Implementation in the Real World

- The Bridge to Web3 Where Payment Tokens Meet Crypto

The Hidden Link Between Your Wallet and Web3

When you tap your phone at a café, you're not just using a polished fintech feature. You're using a token system that mirrors one of Web3's core ideas: replace direct exposure to a valuable asset with a controlled digital representation.

That doesn't mean a Visa token is the same thing as an ERC-20 token. It isn't. One lives inside tightly managed payment rails. The other often lives on open blockchain infrastructure. But the mental model overlaps in an important way. A token stands in for something else, moves through a network, and lets other systems operate without exposing the underlying asset every time.

For crypto-native readers, that makes payment tokenization feel much less like old-world banking jargon and much more like a working production example of applied token design. Traditional finance used tokenization to protect card credentials at internet scale. Web3 is using tokenization to represent money, rights, claims, identity, and real-world assets on programmable rails.

Payment tokenization is one of the rare TradFi concepts that crypto users can understand instantly once they stop treating the word “token” as blockchain-exclusive.

That's also why the rise of tokenization in payments matters now. It grew alongside digital commerce, saved cards, recurring billing, mobile wallets, and one-click checkout. If you want a primer on the broader internet shift toward decentralized digital systems, this Web3 technology overview helps frame where payment infrastructure fits in that evolution.

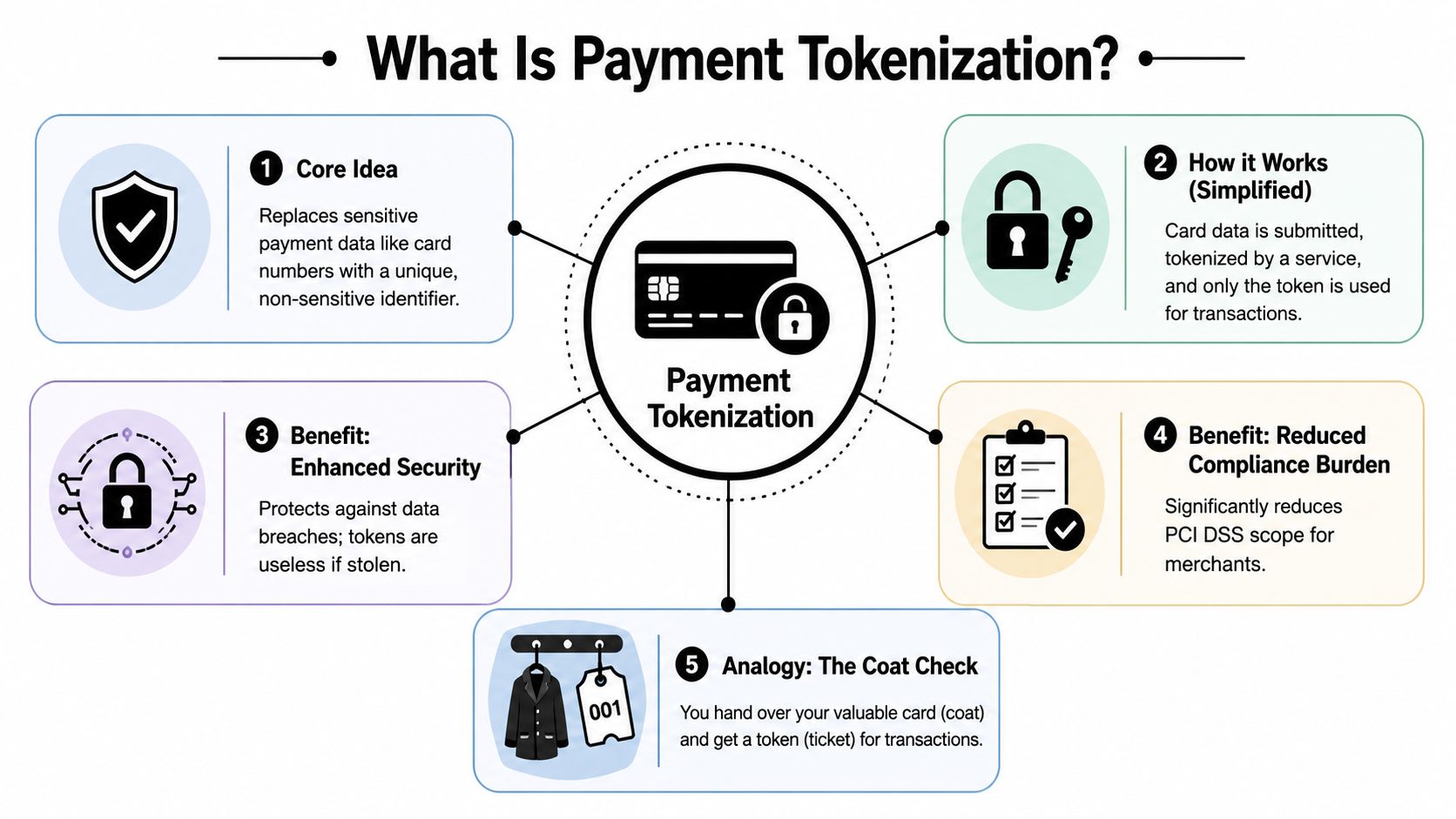

What Is Payment Tokenization Really

A simple definition

Payment tokenization replaces a card's Primary Account Number, or PAN, with a different value that isn't sensitive on its own. The merchant stores and uses that replacement value instead of holding the raw card number directly.

The easiest analogy is a coat check ticket. You hand over something valuable, the venue stores it securely, and you get a claim ticket back. That ticket helps the system work, but it isn't the coat.

A payment token works the same way in spirit. The underlying card data stays in a secure environment controlled by a token service or network. The merchant gets a token that can support payment activity without exposing the original card number in everyday operations.

Crypto readers often trip on the word “token” here, so it helps to draw a clean line.

- Payment token: A surrogate for card data inside the payments stack.

- Crypto token: A blockchain-based unit tracked by a distributed ledger and often governed by smart contracts.

- RWA token: A blockchain token that represents some offchain claim, asset, or legal right.

These are related ideas, not identical products.

Why merchants use it

The biggest reason is simple. Merchants don't want raw card numbers sitting across databases, app layers, logs, and support workflows if they can avoid it.

According to Worldpay, the merchant uses a token instead of the original card number after the token is generated by a tokenization service, and the commercial upside can extend beyond security into approval performance and recurring billing resilience (Worldpay on how tokenization works).

That leads to three practical outcomes:

- Less exposed card data: Fewer systems touch the PAN.

- Lower compliance burden: PCI scope usually becomes easier to manage when sensitive card data is removed from merchant environments.

- Better reuse for digital commerce: Saved cards, recurring subscriptions, and app payments become easier to support safely.

Practical rule: In payment tokenization, the token is useful inside a defined payment context. It is not a freely portable bearer asset like a crypto token in a self-custody wallet.

The Engine Room How Payment Tokens Work

The mechanics matter because tokenization in payments isn't just a security sticker placed on top of checkout. It changes the architecture of the transaction itself.

A useful reference point comes from EMV-style payment ecosystems. Payment tokenization replaces the PAN with a unique token scoped to a specific context, which helps contain damage if a merchant database is breached (J.P. Morgan on network tokenization and EMVCo concepts).

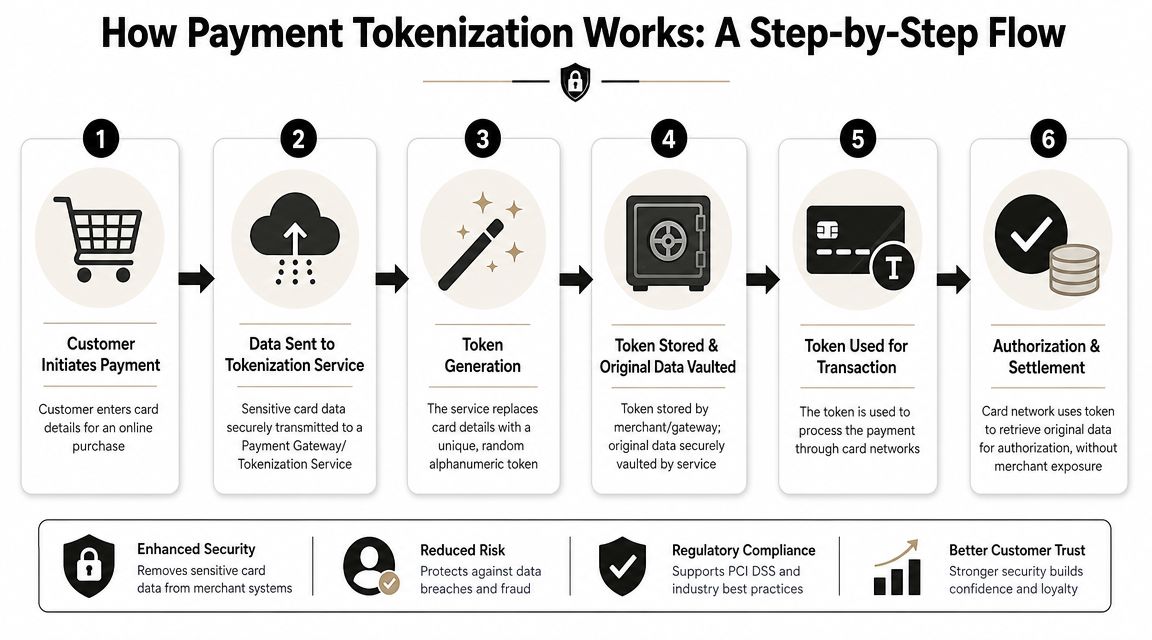

Here's the transaction flow in plain language.

The core transaction flow

- A customer enters card details in an app, checkout page, or wallet.

- Those details go to a tokenization service, payment gateway, network, or wallet provider.

- The provider generates a token and stores the underlying card data in a secure mapping system.

- The merchant keeps the token, not the raw PAN.

- For future charges or card-on-file transactions, the merchant sends the token through the payment flow.

- Authorized parties map the token back to the funding account where needed for authorization, clearing, settlement, refunds, or disputes.

Square describes a typical setup where the token service provider creates a random token with no mathematical relationship to the PAN, while the merchant stores only the token and the provider handles the secure mapping later in the process (Square on what tokenization means).

For readers coming from crypto, this feels a bit like an offchain asset registry plus a permissions layer. The merchant can transact with the representation, but doesn't hold the original credential itself.

To ground the TradFi plumbing in blockchain concepts, this blockchain technology basics guide is a helpful parallel read.

A concise explainer is worth watching here:

Network tokens device tokens and cryptograms

Not all payment tokens play the same role.

Network tokens are issued within card network frameworks and are designed to support ongoing payment operations. They matter for recurring payments and card-on-file setups because they can remain usable across later events in the payment lifecycle.

Device tokens are often associated with wallets such as Apple Pay or Google Pay. They're tied to a specific device or wallet context, which narrows where they can be used.

Then there's the cryptogram, which crypto readers should think of as a transaction-specific proof layer. Mastercard notes that cryptograms add an extra security check to verify authenticity for each payment, giving tokenized transactions a dynamic element rather than a static reused credential, as summarized in the J.P. Morgan material linked earlier.

A stolen token is already less useful than a stolen PAN. A stolen token paired with missing transaction-specific validation is even less useful.

That's one of the hidden strengths of the system. Payment tokenization doesn't just obscure data. It narrows the valid context for using it.

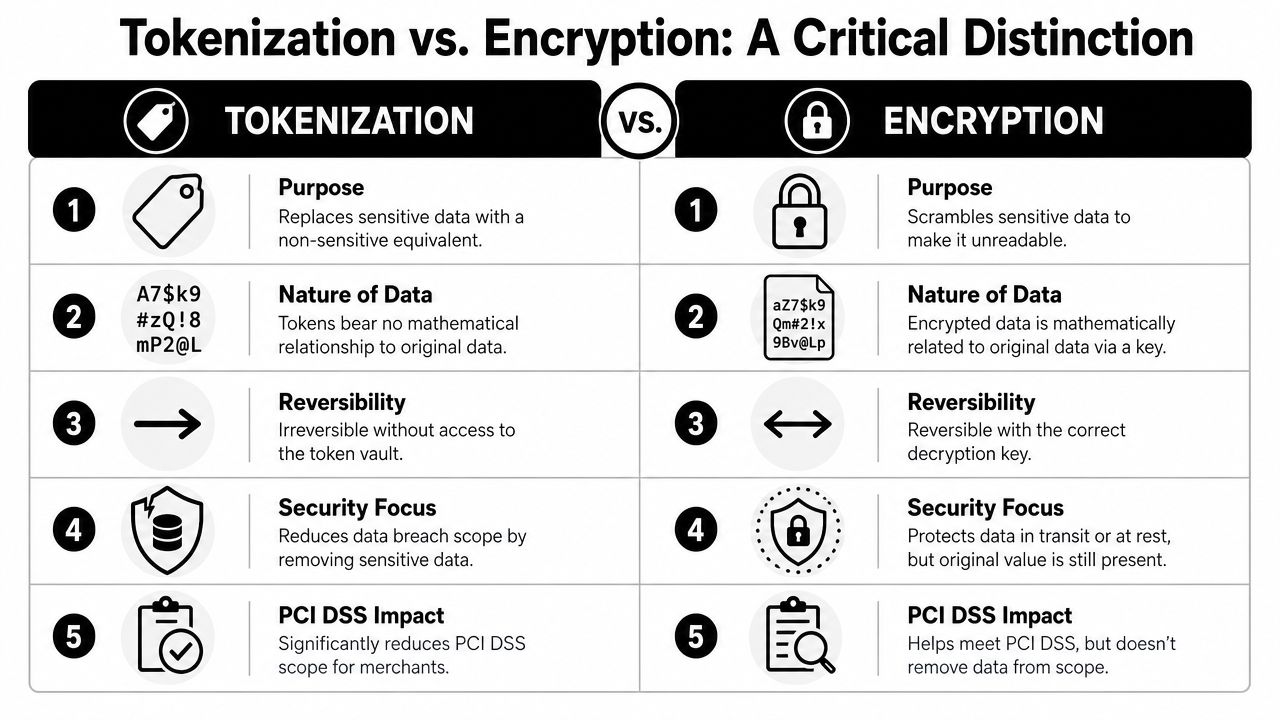

Tokenization vs Encryption A Critical Distinction

A lot of people blur these concepts together. Security teams shouldn't.

Substitution versus scrambling

Encryption scrambles data so authorized systems can later turn it back into its original form using the right key. The original value still exists in encrypted form.

Tokenization substitutes the sensitive value with a different one. The token has no mathematical relationship to the original card number in the typical setup described above. To recover the underlying value, an authorized system usually relies on a vault or token mapping service, not a decryption key applied to the token itself.

That difference changes risk.

If an attacker steals encrypted card data, they've stolen the protected version of the original secret. If they also get the keys, or compromise the right environment, the data becomes readable.

If an attacker steals a payment token from a merchant system, the token often has no independent utility outside its intended domain.

For readers interested in how broader cryptographic systems are evolving beyond payments, this look at the future of cryptography gives useful context.

Tokenization vs Encryption at a Glance

| Attribute | Tokenization | Encryption |

|---|---|---|

| Purpose | Replaces sensitive data with a non-sensitive surrogate | Scrambles sensitive data to make it unreadable |

| Relationship to original data | No mathematical relationship in the typical payment-token model | Mathematically related through encryption methods and keys |

| Reversal method | Requires authorized lookup or detokenization via vault or network mapping | Requires decryption with the correct key |

| Main security benefit | Removes usable card data from merchant environments | Protects data in transit or at rest |

| PCI impact | Often reduces scope significantly when PANs are removed from systems | Helps protect data, but encrypted PAN data may still remain in scope |

Encryption protects secret data. Tokenization tries to keep that secret data out of more places in the first place.

In practice, payment systems often use both. Data may be encrypted in transit and tokenized for storage and reuse.

Unlocking Security and Reducing Compliance Headaches

Security is the obvious headline. The business impact is where tokenization in payments becomes more interesting.

Why issuers like tokenized transactions

ACI Worldwide adds that tokenization can improve authorization rates, reduce false declines, support preferential interchange treatment on eligible transactions, and help reduce involuntary churn through lifecycle updates for recurring billing, as summarized by Worldpay in its overview linked earlier.

That matters because payment performance isn't just about blocking fraud. It's also about getting legitimate transactions approved.

If an issuer sees a network-tokenized transaction as more trustworthy than a raw PAN transaction, a merchant may benefit in ways customers never notice directly:

- Fewer avoidable declines: A genuine customer is less likely to get blocked by a risk model that distrusts the credential.

- Better checkout continuity: Returning users can keep buying without re-entering card details every time.

- Healthier recurring revenue: Subscription merchants care significantly about billing continuity.

This is one reason payment teams treat tokenization as revenue infrastructure, not just risk infrastructure.

Why subscription businesses care

Recurring billing exposes a separate problem. Cards expire, get replaced, or are reissued after fraud events. If every change forced the customer to manually update billing details, subscription businesses would lose legitimate payments for preventable reasons.

Tokenized setups can help maintain continuity when the underlying card changes, because lifecycle management can update the credential relationship behind the scenes within the payment ecosystem. For a streaming app, SaaS platform, game subscription, or AI tool charging monthly, that's operationally valuable.

The quiet win in tokenization isn't only fewer breaches. It's fewer moments where a valid customer hits a payment error that didn't need to happen.

There's also the PCI angle. Teams that stop storing raw card numbers directly reduce the surface area that auditors and security teams need to treat as card-data heavy. That doesn't remove all obligations, but it can make the compliance burden more manageable.

From Code to Checkout Implementation in the Real World

Theory feels abstract until you notice how often you already rely on tokenization in payments.

Where you already use it

Mobile wallets are the most visible example. Tap-to-pay on a phone or wearable typically avoids exposing the raw card number to the merchant in the way older card-present flows did.

Card-on-file checkout is another. When an e-commerce site lets you buy with a saved card, there's usually a token sitting behind that convenience layer.

Recurring billing depends on the same idea. Subscription software, media platforms, gaming services, cloud tools, and digital memberships all need a reusable payment reference that isn't just a raw PAN copied into a merchant database.

These use cases make tokenization feel less like a specialist security product and more like baseline infrastructure for internet commerce.

What implementation teams actually manage

The engineering work is more involved than “call an API and forget about it.”

Square's description is useful here: the provider generates a random token with no mathematical relationship to the PAN, which reduces PCI scope for merchants, but creates dependencies around token provisioning APIs and lifecycle management (Square's implementation-oriented explanation).

That tradeoff shows up in everyday operations:

- Provisioning logic: Teams need reliable creation and storage of tokens during signup, checkout, and wallet enrollment.

- Lifecycle handling: Tokens may need updates when cards change, wallets are re-provisioned, or issuers refresh credentials.

- Failure management: A token can still fail if the underlying funding source changes or if downstream systems reject the transaction.

- Provider dependence: Merchants rely on payment gateways, token vaults, networks, and related APIs staying available.

For developers building modern payment experiences, the work sits at the intersection of backend architecture, security policy, and product UX. If your world already includes wallet integrations, smart contracts, or dApp interfaces, this Web3 application development guide helps connect those implementation mindsets.

One practical takeaway stands out. Tokenization reduces exposure, but it also introduces infrastructure relationships that teams need to monitor carefully. In crypto language, it lowers one class of risk while adding dependency on specific rails and service providers.

The Bridge to Web3 Where Payment Tokens Meet Crypto

The big similarity

The conceptual overlap is hard to miss. In both TradFi payment tokenization and Web3 tokenization, a digital representation stands in for something of value.

In card payments, the token stands in for a PAN. In crypto, a token may stand in for native network value, governance power, a stablecoin claim, access rights, or an offchain asset. In RWA systems, the token may represent a treasury exposure, a fund interest, real estate rights, or another legally structured claim.

That's why payment tokenization feels like the older cousin of the tokenized economy crypto builders want. Traditional payments proved that users and institutions will trust token-based interaction models when those models improve security and usability.

The crucial difference

The differences matter more than the similarities if you're investing, building, or thinking about long-term market structure.

Payment tokens are usually closed-loop, permissioned, and purpose-built for secure transaction routing. They are not general-purpose assets. They don't usually carry open composability across DeFi protocols, decentralized exchanges, or smart-contract platforms.

Web3 tokenization aims for something broader. It wants assets to be programmable, composable, portable, and machine-readable across applications. That opens the door to DeFi lending, automated market makers, collateral systems, onchain identity layers, and entirely new tokenomics models.

It also exposes a limitation in payment tokenization. It secures credentials, but it doesn't fix the deeper frictions of cross-border payments by itself. The Bank for International Settlements notes that broader tokenization could make transactions “instantaneous, programmable and less costly” (BIS paper on tokenisation and the future financial system). That's an ambitious destination. Current card tokenization helps with security and continuity, not with every settlement, FX, compliance, or interoperability problem across jurisdictions.

Where convergence could happen next

Crypto-native readers will find this particularly interesting.

Real-world assets: Payment tokenization taught institutions that token representations can reduce risk and improve operations. That makes the leap to tokenized money market funds, tokenized deposits, and other RWAs easier to understand politically and technically.

Smart contracts: TradFi tokenization mostly secures and routes. Smart contracts let tokenized assets execute logic. A token can become collateral, trigger payouts, enforce transfer rules, or plug into DeFi rails automatically.

Layer 2 scaling: If Web3 wants to support mainstream payment-like experiences, it needs cheaper and faster execution. Layer 2 networks matter because users won't tolerate clunky settlement for everyday financial activity.

AI plus crypto: As tokenized economies grow, AI systems may help manage routing, fraud screening, risk scoring, treasury decisions, and onchain monitoring. In a hybrid future, AI agents could interact with both bank-grade token rails and blockchain-based asset networks.

Wallet UX will also matter. The average person doesn't care whether a token lives in a card network, a custody platform, or a self-custody app. They care whether payments work, assets are safe, and the interface feels simple. If you want a practical example of how crypto users interact with tokenized assets today, this Phantom Wallet guide is a useful starting point.

The likely future isn't “TradFi tokenization loses and Web3 wins,” or the reverse. The more plausible outcome is convergence. Card networks, banks, fintechs, stablecoin issuers, DeFi protocols, and wallet providers are all solving adjacent pieces of the same problem: how to represent value digitally without exposing too much risk, too much friction, or too much complexity to the user.

If you want more clear, grounded analysis on crypto, Web3, DeFi, wallets, Layer 2s, AI-blockchain trends, and tokenized real-world assets, explore Coiner Blog. It's a strong resource for readers who want practical explanations instead of hype.