Cryptocurrency ramblings

ETF Creation Redemption Process: Powering Crypto ETFs

You're probably seeing Bitcoin ETF tickers everywhere, watching crypto and TradFi collide in real time, and wondering what's happening under the hood. You buy a share on an exchange, the chart moves, liquidity appears, spreads tighten, and somehow the ETF keeps tracking an asset that lives on a blockchain rather than in a broker's old-school ledger.

That mechanism matters more than the headlines. The ETF creation redemption process is the hidden engine that turns investor demand into tradable shares, and in crypto ETFs it also exposes the messy edges of regulation, custody, settlement, and tax design. If you've been following price action and asking whether the move is driven by flows, arbitrage, or structure, that curiosity is exactly the right instinct.

The recent rush into spot Bitcoin products made this impossible to ignore. Plenty of people focused on price and momentum, much like they do when asking why Bitcoin is rising. But the deeper story sits behind the ticker. Why doesn't the ETF just drift wildly away from the value of the Bitcoin it's supposed to represent? Who creates new shares when demand spikes? Who removes shares when sellers overwhelm buyers?

Those questions pull you into the plumbing of modern markets. And once you understand that plumbing, crypto ETFs stop looking like magic and start looking like a tightly governed bridge between Web3 assets and regulated capital markets.

Table of Contents

- The Billion-Dollar Question Behind Bitcoin ETFs

- The ETF Ecosystem Key Players and Markets

- The Creation Cycle How New ETF Shares Are Born

- The Redemption Cycle How ETF Shares Are Retired

- In-Kind vs Cash Creates The Big Debate for Crypto ETFs

- The Arbitrage Flywheel Keeping ETF Prices Honest

- Crypto Custody Settlement and Investor Takeaways

The Billion-Dollar Question Behind Bitcoin ETFs

Spot Bitcoin ETFs changed the conversation because they gave traditional investors a familiar wrapper for a natively digital asset. For a crypto-native reader, that wrapper can look almost suspiciously simple. You click buy in a brokerage account, and suddenly you have Bitcoin exposure without touching a wallet, seed phrase, bridge, or Layer 2.

That convenience raises a harder question. If an ETF share trades like a stock on an exchange, how does it stay tied to an asset that trades across crypto venues with different custody, liquidity, and settlement patterns?

Here's the part most headlines skip. The ETF share you buy on the secondary market doesn't appear out of nowhere. Institutions coordinate the supply of those shares behind the scenes through a controlled process of creation and redemption. That process is what lets ETFs expand when demand rises and contract when demand falls, instead of just floating away from the value of the underlying asset.

Crypto traders often think first in terms of order books and exchange liquidity. ETF mechanics add another layer. Primary market inventory management.

For Bitcoin ETFs, that matters because the product sits between two worlds with very different operating assumptions. Crypto assumes constant markets, transparent ledgers, and self-custody as a philosophical ideal. TradFi assumes regulated intermediaries, named gatekeepers, settlement cycles, and compliance workflows.

The result is a product that feels simple on the surface and highly engineered underneath. Once you understand the engine, you can read ETF flow headlines differently. You can think about whether premiums, discounts, custody choices, or cash creation models may affect execution quality, tax efficiency, and long-term investor outcomes.

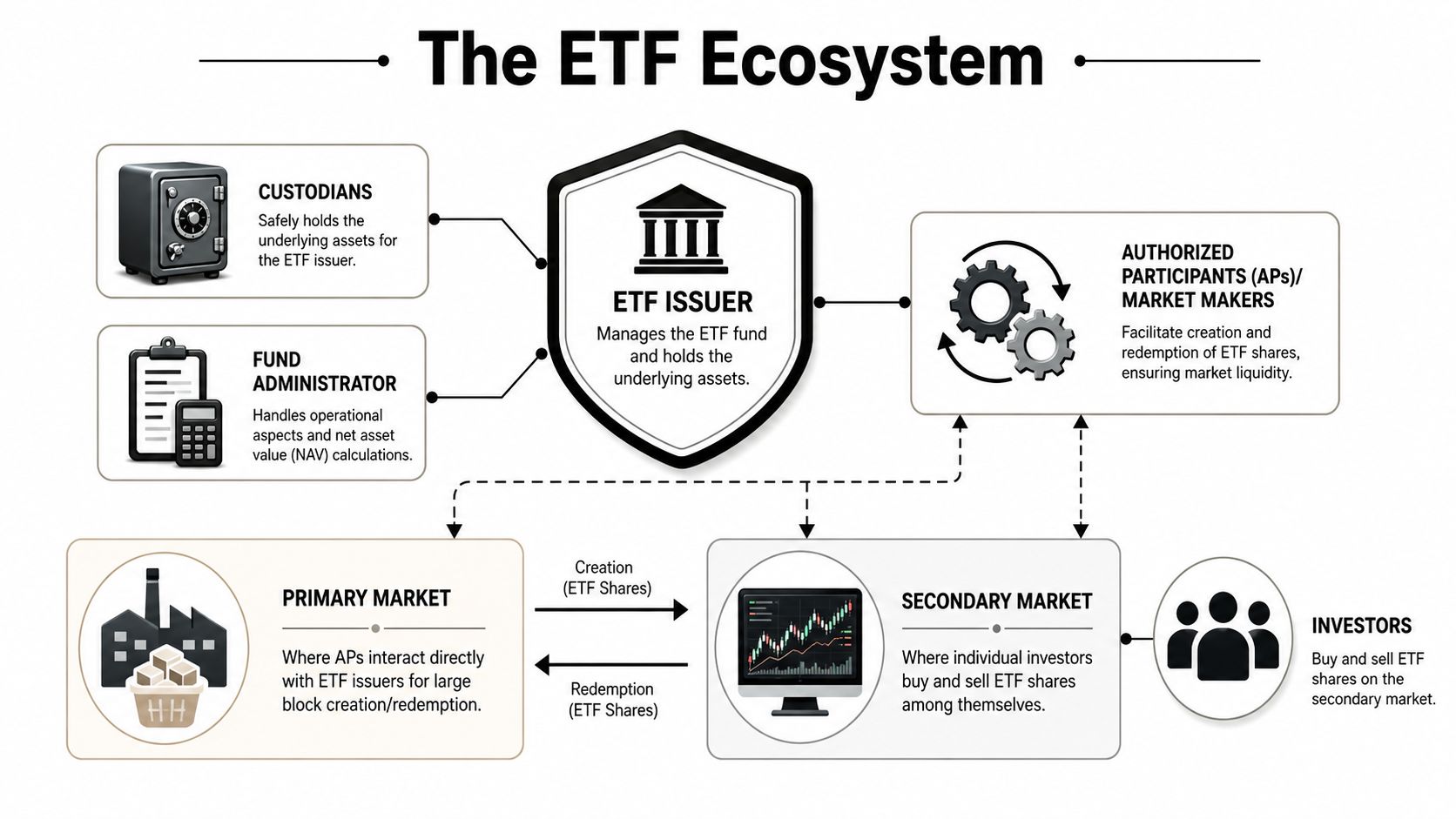

The ETF Ecosystem Key Players and Markets

The ETF machine works because two markets interact continuously, but they don't serve the same people.

Two markets, one product

The secondary market is the public-facing layer. That's where retail investors, RIAs, institutions, and traders buy and sell ETF shares on an exchange. If you've traded stocks, this part feels normal.

The primary market is different. It's restricted. According to Schwab Asset Management's explanation of the mechanism, ETF creation and redemption occurs exclusively in the primary market between ETF issuers and Authorized Participants, or APs, which are large institutional investors such as banks or market makers and the only entities permitted to create or redeem new ETF shares.

A crypto analogy helps. Think of the secondary market as trading wrapped tokens on an exchange, while the primary market is the mint-and-burn contract that only a whitelisted operator can access. Retail users can trade the asset. They can't control issuance.

The institutions doing the heavy lifting

Three players matter most.

- ETF issuer: The issuer designs and manages the fund. It defines the basket rules, product structure, and operating process.

- Authorized Participant: The AP is the institutional bridge between secondary-market demand and primary-market share supply. These are usually large banks or market makers.

- Custodian: The custodian safeguards the underlying assets. In crypto ETFs, this role gets much more attention because custody is not a side detail. It's the foundation of trust.

A fourth player often sits in the background.

- Fund administrator: This party handles operational functions such as fund accounting and NAV calculations.

That structure is one reason investors care about banking relationships and market plumbing in digital asset products. If you want a broader sense of how traditional rails are adapting to this new stack, the range of crypto-friendly banks helps explain why these partnerships matter.

Practical rule: If you don't know who the APs, custodian, and issuer are, you don't fully know the ETF.

Here's a simple way to frame the ecosystem:

| Market layer | Who acts there | What happens |

|---|---|---|

| Secondary market | Investors and traders | ETF shares change hands between buyers and sellers |

| Primary market | Issuer and APs | New shares are created or existing shares are redeemed |

| Custody layer | Custodian | Underlying assets are held securely for the fund |

| Admin layer | Fund administrator | NAV and fund operations are maintained |

For crypto ETFs, this architecture also intersects with tokenization of real-world assets, institutional DeFi experiments, and AI-driven market surveillance. The product may look old-world, but the strategic significance is very Web3.

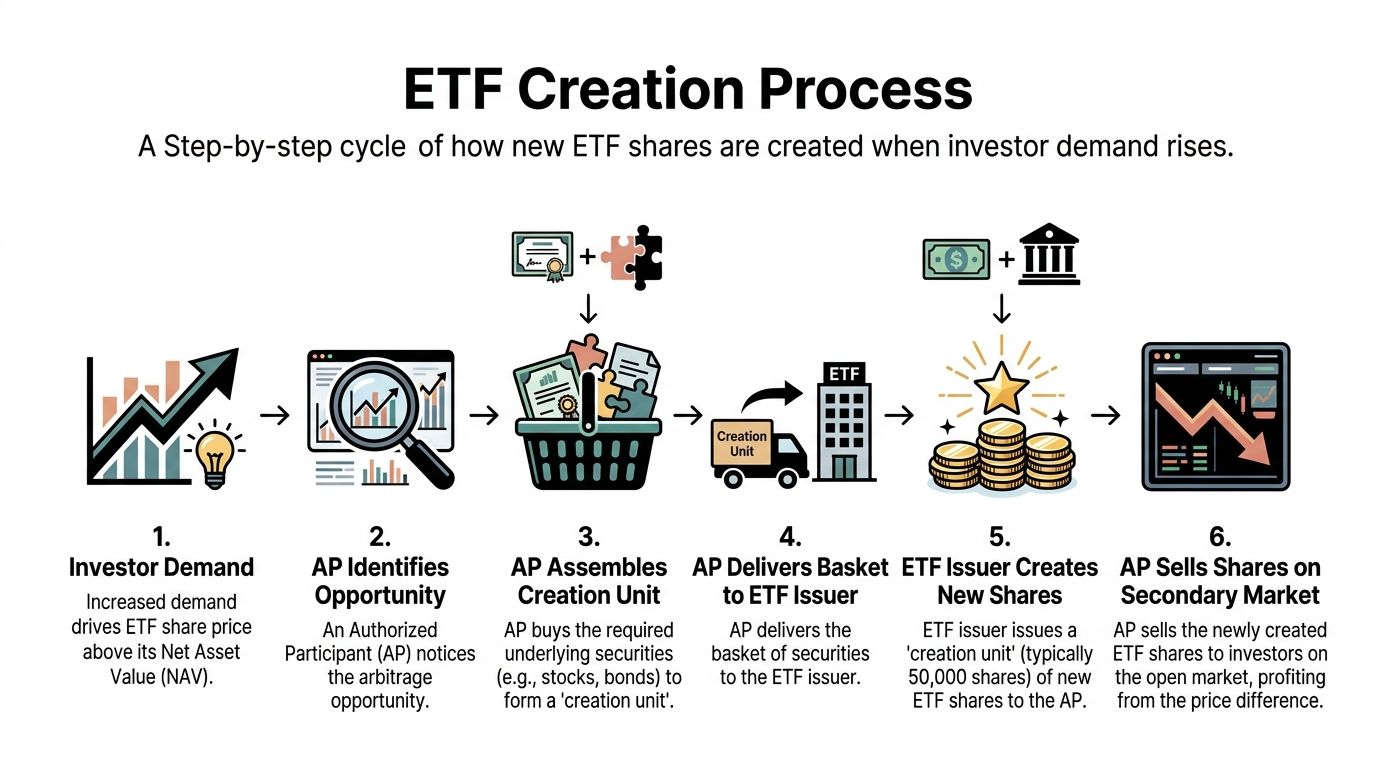

The Creation Cycle How New ETF Shares Are Born

A bitcoin ETF suddenly starts trading above the value of the bitcoin it is supposed to represent. Buyers keep hitting the offer, but the number of ETF shares on the exchange has not changed yet. If nothing corrected that imbalance, the ETF could drift away from its underlying holdings and become a less reliable wrapper.

Creation is the mechanism that restocks inventory.

In the primary market, an authorized participant, or AP, can deliver the required basket to the fund and receive a large block of newly issued ETF shares called a creation unit. BlackRock's overview of ETF mechanics explains that creation and redemption happen in large institutional blocks rather than one share at a time, which is why retail investors do not interact with the fund this way directly, as described in BlackRock's ETF structure guide.

What triggers creation

The usual trigger is a premium. The ETF shares are trading above the value of the underlying portfolio, so an AP has an arbitrage opportunity.

The AP gathers whatever the issuer requires for that fund, which may be a basket of securities, cash, or in crypto ETFs often cash that will later be used to source bitcoin. The AP delivers that package to the issuer. The issuer then creates a new block of ETF shares and hands it back to the AP, which can sell those shares on the exchange. That extra supply pushes the ETF price back toward fair value.

For crypto-native readers, this works like a controlled mint process with human gatekeepers, legal contracts, and settlement rails standing in for smart contracts. The mint is not algorithmic. It is operational.

The step-by-step flow

Here is the cycle in plain English:

- ETF demand rises on the exchange. Buyers bid the share price above the value of the fund's holdings.

- An AP sees the spread. The trade only makes sense if the premium is large enough to cover fees, execution costs, and timing risk.

- The AP prepares the creation basket. In traditional equity ETFs, that basket is often the underlying securities. In many spot bitcoin ETF structures, the basket is cash.

- The AP delivers the basket to the fund.

- The issuer releases a creation unit of new ETF shares to the AP.

- The AP sells those shares in the secondary market. More shares in circulation usually reduce the premium.

That sounds clean on paper. In crypto ETFs, the actual process can be less direct because cash must be converted into bitcoin, the bitcoin must be custodied correctly, and each handoff introduces timing and operational risk.

A short visual helps if you want to see the sequence in motion:

Why crypto readers should care

The creation cycle is one reason an ETF can absorb fresh demand without relying only on the shares already trading in the market. That matters if you are comparing visible exchange volume with actual market depth. The difference is similar to the gap between a token's displayed order book and the broader system that can source more supply when prices move. This is the same intuition behind understanding liquidity in cryptocurrency markets.

Crypto ETFs add a twist that many basic ETF guides skip. The AP may not be delivering bitcoin directly. It may be delivering cash, then waiting for the issuer and its trading and custody partners to complete the bitcoin purchase and settlement workflow. That makes creation mechanics more dependent on banking access, custody design, and market hours than many crypto investors expect.

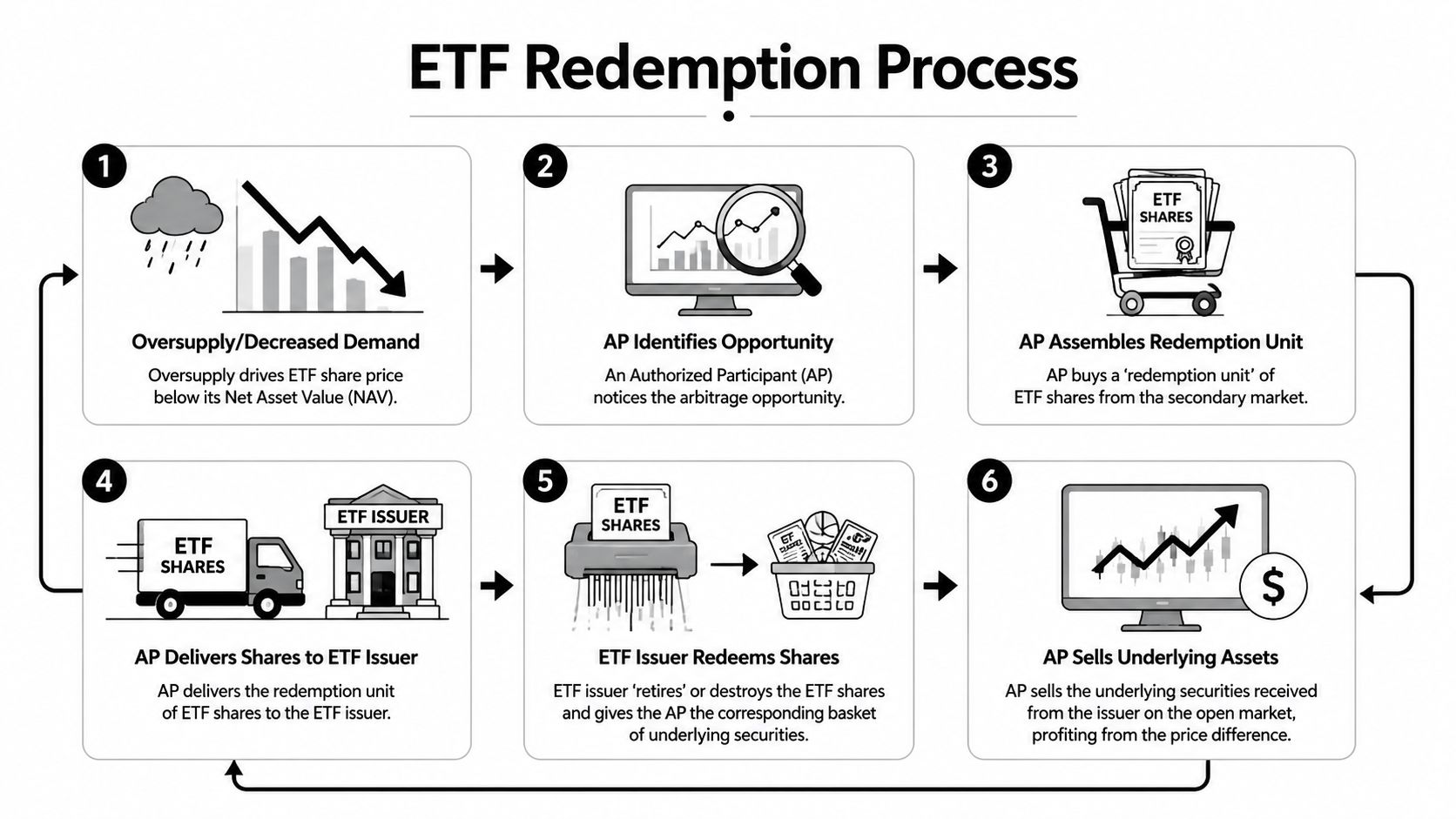

The Redemption Cycle How ETF Shares Are Retired

Creation adds supply. Redemption removes it.

When redemption starts

Redemption usually becomes attractive when the ETF trades below the value of its underlying portfolio. In plain English, ETF shares are now cheaper than what the fund's holdings imply they should be.

An AP can exploit that difference. It buys ETF shares in the secondary market, gathers enough to form a redemption unit, returns that block to the issuer, and receives the underlying assets or cash back. That shrinks share supply in the market.

Exegy notes that redemption units generally range between 10,000 and 50,000 shares, and that this mechanism is vital for liquidity because it helps eliminate discounts when an ETF trades below NAV. As ETF shares are removed from the market, pricing inefficiencies are arbitraged away quickly, according to Exegy's breakdown of the process.

How the unwind works

The redemption cycle works like this:

- Step one: The AP sees ETF shares trading at a discount.

- Step two: It buys enough shares on the exchange to form a redemption unit.

- Step three: It delivers that block to the issuer in the primary market.

- Step four: The issuer retires those ETF shares.

- Step five: The AP receives the underlying asset basket or cash equivalent.

- Step six: The AP can then sell those assets in the open market.

This is the deflation valve of the system. Fewer ETF shares circulate on the exchange, which helps the market price move back toward underlying value.

Redemption is where ETF structure shows its discipline. The product doesn't rely only on hope that prices reconnect. It gives institutions a reason to force the reconnect.

For crypto-native readers, this should resemble a controlled burn. But again, the analogy only goes so far. In a token system, burns may be governance-driven or automated by smart contracts. In an ETF, the reduction in supply depends on regulated counterparties acting when economics make sense.

That distinction becomes especially important during market stress. In volatile conditions, AP behavior, custody friction, trading halts, and the practical ease of handling the underlying asset all shape how smoothly redemption works.

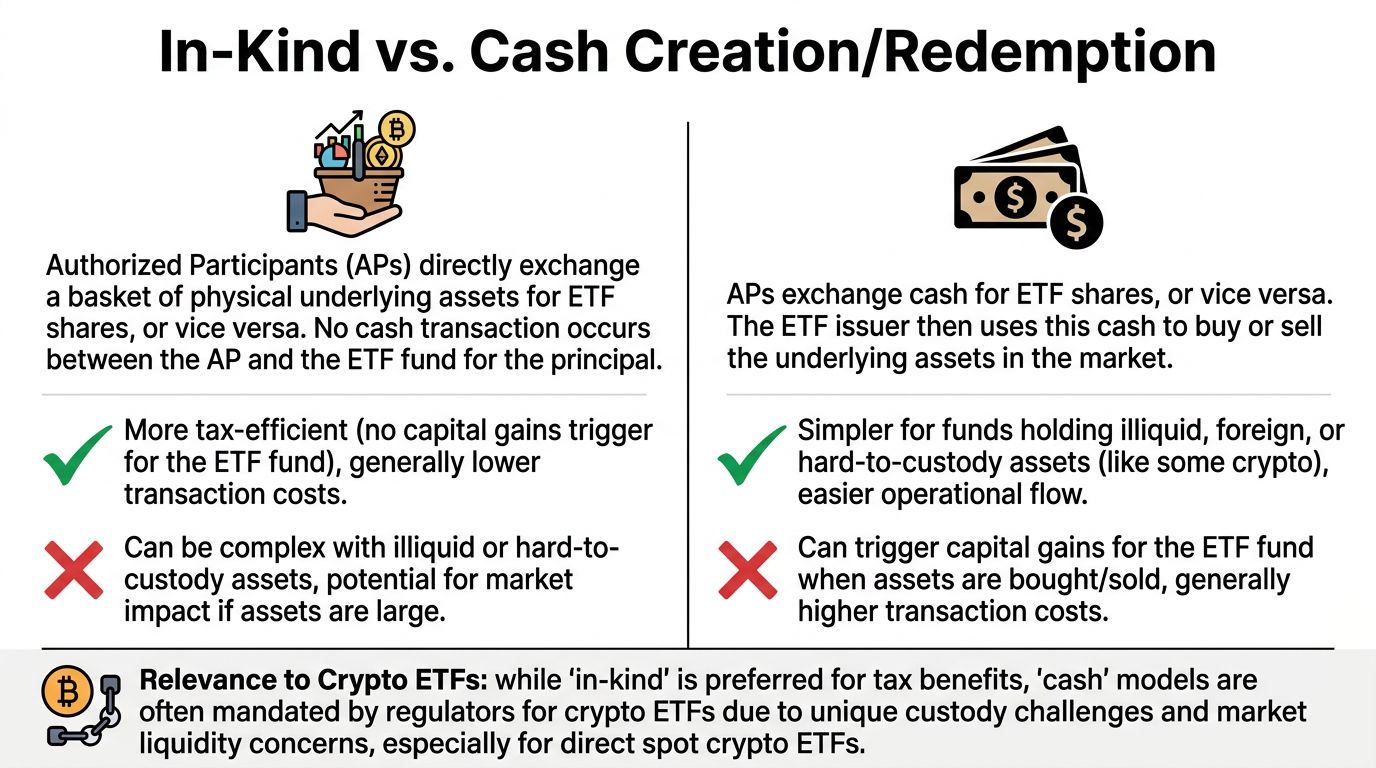

In-Kind vs Cash Creates The Big Debate for Crypto ETFs

Traditional ETF theory meets crypto market reality.

The side-by-side difference

In a classic in-kind model, the AP exchanges the actual underlying assets for ETF shares, or does the reverse in redemption. That structure is prized in TradFi because the fund can avoid selling assets itself, which tends to reduce internal friction and improve tax efficiency.

In a cash model, the AP sends cash to the issuer for creations, and the issuer buys the underlying assets. For redemptions, the process reverses. Operationally, this can be simpler when assets are difficult to transfer or custody directly.

Here's the clean comparison:

| Model | What gets exchanged | Main advantage | Main trade-off |

|---|---|---|---|

| In-kind | Underlying assets for ETF shares | Better tax efficiency and lower trading friction inside the fund | Harder when the underlying asset is operationally complex |

| Cash | Cash for ETF shares | Simpler workflow for difficult-to-handle assets | The fund may need to buy or sell assets directly, which can be less efficient |

Why crypto ETFs became a special case

Crypto complicates the idealized in-kind model. The underlying asset may be liquid globally, but that doesn't mean every regulated participant can handle it the same way. Custody standards, wallet controls, compliance, counterparty risk, surveillance expectations, and the operational challenge of moving digital assets under regulated fund rules all shape the outcome.

That's why the debate around spot crypto ETFs has centered so heavily on cash creates. For a crypto reader used to permissionless transfer, that can feel clunky. But in a regulated product, clunky often means auditable.

There's also a tax angle. The standard ETF framework often favors in-kind exchange because it can minimize fund-level realization events. SEC Rule 6c-11 enabled in-kind transfers in the ETF structure, and that's one reason traditional equity ETFs are often admired for tax efficiency. Crypto products, however, have had to proceed along a more constrained path because regulation tends to prioritize control, surveillance, and custody discipline over elegant market design.

In crypto, the best technical design doesn't always win first. The structure that regulators will permit usually arrives before the structure engineers would prefer.

That trade-off matters for investors. A cash-create model can be easier for regulators and service providers to supervise, but it may introduce extra trading steps, extra operational exposure, and less graceful tax handling than the in-kind ideal.

The long-term direction is worth watching. As tokenization grows and TradFi rails move closer to onchain settlement, future ETF-like products may borrow more from smart contracts, real-time attestations, and programmable custody logic. For now, crypto ETFs still run on a heavily intermediated model.

The Arbitrage Flywheel Keeping ETF Prices Honest

The whole structure works because APs have an incentive to act when the ETF price and the value of the underlying portfolio diverge.

What APs are actually chasing

An ETF has a market price and a net asset value, or NAV. The market price is what shares trade for on an exchange. NAV is the value of the assets inside the fund.

If the ETF trades above NAV, creation can make sense. If it trades below NAV, redemption can make sense. APs pursue that spread. Their trading helps close the gap.

This is the self-correcting loop at the heart of the ETF creation redemption process:

- Premium to NAV: APs create shares and sell them.

- Discount to NAV: APs redeem shares and remove them.

- Result: Supply adjusts, and price tends to move back toward underlying value.

If you already follow arbitrage trading in crypto markets, the intuition is similar. Price differences create opportunity. The key distinction is that ETF APs can interact with the issuer in the primary market, which gives them a structural tool most crypto traders don't have.

The arbitrage engine doesn't eliminate risk. It reduces persistent mispricing when institutions are willing and able to act.

Why this matters in volatile markets

This mechanism is one reason ETF liquidity can be deeper than the tape alone suggests. What you see on-screen is only part of the story. Behind it sits an institutional process that can create or retire inventory.

That doesn't mean ETFs are invincible. If the underlying asset becomes hard to trade, custody gets constrained, or market stress widens spreads, the mechanism can get less smooth. That's why serious investors pair structure analysis with execution discipline and broader reading on managing crypto trading risk.

For crypto ETFs, the arbitrage flywheel is powerful, but it's still bounded by regulation, custody design, and settlement realities. In other words, elegant market structure still has to survive practical realities.

Crypto Custody Settlement and Investor Takeaways

Crypto ETFs don't just wrap an asset. They wrap a custody model, a settlement model, and a regulatory compromise.

Who holds the coins

In a spot crypto ETF, investors don't hold the underlying coins directly. The fund does, through a custody arrangement built for regulated products. That's convenient for investors who want exposure without handling wallets, but it also changes the ownership experience completely.

The core trade-off is simple. Self-custody gives control. ETF ownership gives convenience, brokerage integration, and institutional administration. Those are not the same thing, and the old crypto principle behind not your keys, not your coin still matters when you evaluate what kind of exposure you want.

A crypto ETF can be the right tool for some portfolios. It just shouldn't be confused with direct onchain ownership.

The settlement detail most guides skip

One under-discussed issue is settlement timing during rebalancing. According to Sound Capital Solutions' discussion of ETF settlement timing, standard creations settle on T+1, while custom rebalance redemptions can create a 48-hour window because the redemption settles on T+1 and the accompanying standard creation settles on T+2. That timing can defer capital gains rather than realizing them immediately at the fund level. The same source notes that 78% of ETF advisors in an ICI survey cited this timing as a top client concern, yet few public guides explain it.

That sounds obscure until you remember what crypto investors already know. Settlement details often decide who bears friction, who bears tax timing, and who carries interim exposure. In DeFi, smart contracts make many of those rules visible. In ETFs, they're embedded in legal and operational procedures that many investors never read.

Settlement isn't clerical. It's economic design wearing back-office clothing.

What to look for before you buy

If you're comparing crypto ETFs, focus on these questions:

- Creation model: Is the fund using cash creates or an in-kind style structure where permitted?

- Custody setup: Who is holding the assets, and how transparent is the arrangement?

- Operational complexity: Does the product rely on many intermediaries between investor and asset?

- Tax and rebalancing mechanics: Are there custom redemption features that may affect how gains are managed?

- Fit for purpose: Do you want price exposure in a brokerage account, or do you want actual onchain utility in Web3, DeFi, staking, or smart contract ecosystems?

The future may push these products closer to tokenized fund shares, onchain transfer rails, AI-assisted compliance, and real-time attestations of reserves. Layer 2 infrastructure and tokenization of real-world assets are already nudging financial markets in that direction. But for now, crypto ETFs remain a hybrid. Part blockchain narrative, part old-world market plumbing.

If you want more clear-eyed crypto analysis that connects Bitcoin, ETFs, DeFi, AI, tokenization, Layer 2s, and market structure without the usual hype, visit Coiner Blog. It's built for readers who want to understand how the system works before they put capital at risk.

1 Comment