Cryptocurrency ramblings

RWA Tokenization News: 2026 Insights & Analysis

The most important number in RWA tokenization news isn't the headline-grabbing market size. It's the gap between who can access the market and who can't.

On one side, tokenized real-world assets have moved from $158 million at the beginning of 2022 to over $30 billion in total assets under management by early 2026, according to Interexy's summary of DeFi Llama-based RWA growth data. On the other, much of that expansion has flowed into structures built for institutions first, not for everyday investors.

That's why this cycle matters. RWA tokenization isn't just another Web3 narrative competing with memes, Layer 2 adoption, or AI-powered crypto products. It's an attempt to rebuild financial distribution itself through blockchain rails, smart contracts, and programmable compliance. The promise is huge. The accessibility is not.

Table of Contents

- The Trillion-Dollar Bridge Between DeFi and Traditional Finance

- How RWA Tokenization Actually Works

- Market Growth and the Latest RWA Tokenization News

- Leading RWA Platforms and Projects to Watch

- The Shifting Regulatory and Market Implications

- Investor Risks and the Retail Access Paradox

- The Future of RWAs and Your Next Steps

The Trillion-Dollar Bridge Between DeFi and Traditional Finance

RWA tokenization turns ownership rights in traditional assets into blockchain-based tokens. That sounds technical, but the economic idea is simple. A Treasury fund, a private credit vehicle, a gold position, or a property interest can be represented on-chain and managed through smart contracts instead of only through siloed legacy systems.

That makes RWA tokenization one of the clearest bridges between DeFi and traditional finance. Crypto has always been strong at building open settlement layers. Traditional finance has always held the deeper asset base. Tokenization connects those two strengths.

Why this bridge matters

For institutions, the appeal is operational. Blockchain rails can combine distribution, trading, clearing, settlement, and safekeeping in a more unified stack than most legacy financial workflows. For crypto-native users, the appeal is different. They gain exposure to instruments that historically lived behind brokerage, private banking, or fund administration walls.

A useful mental model is tokenized real estate. Instead of treating a property interest as a paperwork-heavy asset that moves slowly, tokenization can turn it into a digitally issued instrument with compliance rules embedded into the asset itself. That's the core logic behind many projects in tokenized real estate markets.

Main takeaway: RWA tokenization isn't trying to replace finance. It's trying to repackage finance onto more efficient rails.

Why the headline story is incomplete

The bullish narrative says tokenization democratizes access. That's directionally true in theory, but not reliably true in market structure.

Most recent RWA tokenization news points to institutional traction, regulated issuance, and rapid onboarding of capital. Those are real positives. But they also reveal something more subtle. The first successful wave of adoption has centered on products that large allocators can use immediately, not on products designed for broad retail participation.

That distinction matters because it changes how investors should read the market. Growth alone doesn't prove openness. In many cases, it proves that institutions finally have a compliant path to move on-chain.

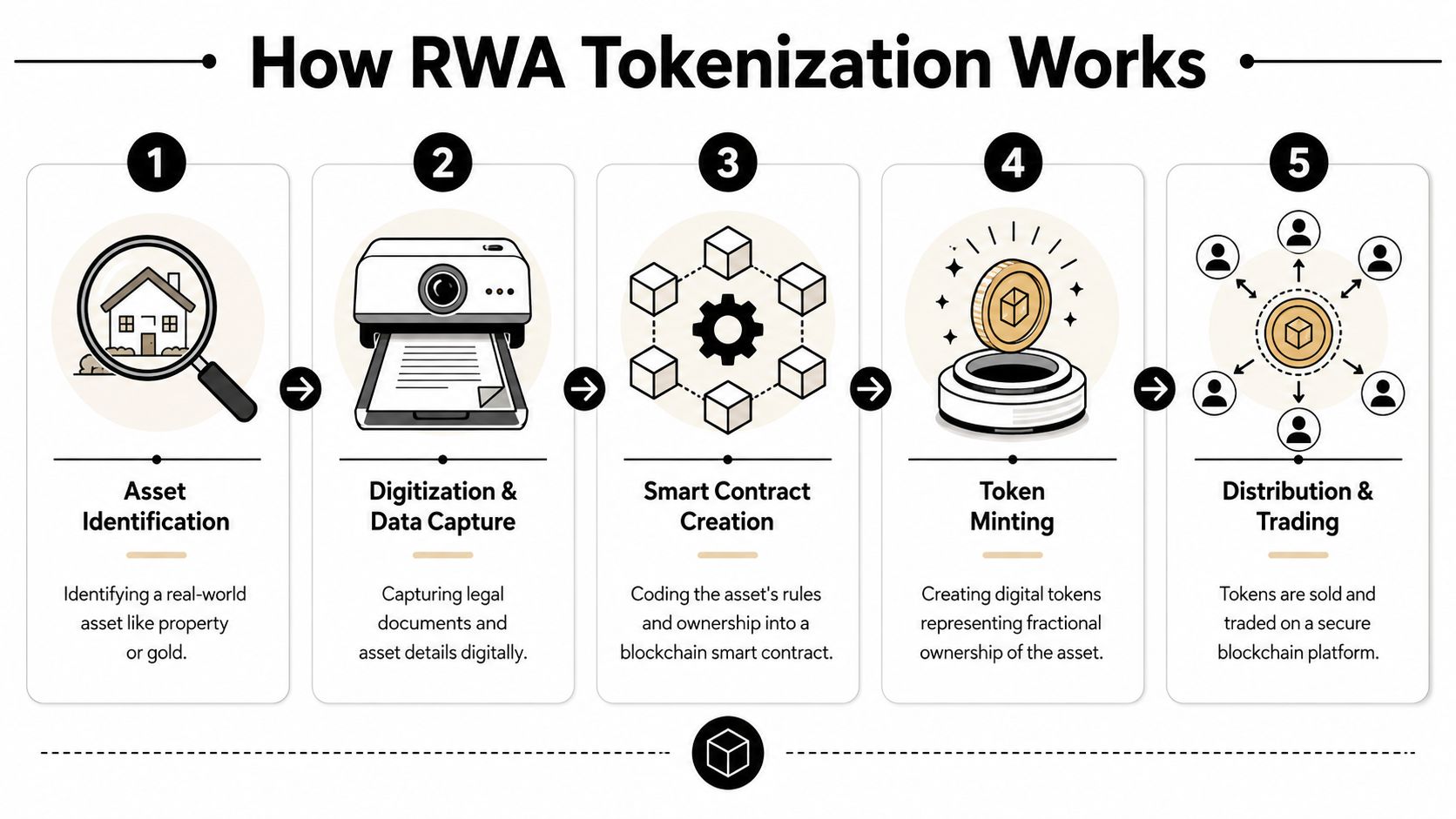

How RWA Tokenization Actually Works

Tokenization sounds abstract until you map the process. Think of it as converting a legal asset into a blockchain-based wrapper that can be issued, tracked, and transferred under explicit rules.

The easiest analogy is a building. You don't move the building onto Ethereum. You move the ownership logic and transfer rules into a legally connected digital format.

From legal asset to on-chain token

Most tokenization flows follow five practical steps.

Asset selection

An issuer starts with an asset that can be clearly identified and legally documented. That could be debt, real estate, commodities, fund interests, or receivables.Legal packaging

The issuer defines what token holders own. In many structures, the token represents a claim on an entity, trust, note, or managed vehicle rather than direct title to the underlying asset itself.Data digitization

Key documents, ownership records, eligibility rules, and compliance requirements are converted into machine-readable workflows. With this conversion, a tokenized product stops being a concept and becomes operational.

If you want a broader primer on the concept itself, this guide to crypto tokenization is a useful companion.

Why smart contracts and oracles matter

The blockchain layer handles the automation. Smart contracts define what can happen to the token. They can restrict transfers, manage issuance and redemption, route distributions, and enforce compliance conditions such as whitelisting.

Oracles handle the connection between off-chain facts and on-chain actions. If a token references yield, maturity events, asset valuations, or reserve confirmations, the smart contract needs a trusted data input. That's the oracle's role.

Here's the practical split:

| Component | What it does |

|---|---|

| Legal structure | Defines the enforceable rights behind the token |

| Smart contract | Automates issuance, ownership rules, and transfers |

| Oracle layer | Brings external data on-chain |

| Blockchain network | Records transactions and settlement |

| Custody and compliance systems | Control who can hold or move the asset |

A token is only as strong as the legal claim, the compliance design, and the data feeds behind it.

This is why RWA infrastructure often looks more conservative than pure DeFi. The goal isn't maximum openness at any cost. It's to make a regulated asset programmable without breaking the legal framework that gives it value in the first place.

Market Growth and the Latest RWA Tokenization News

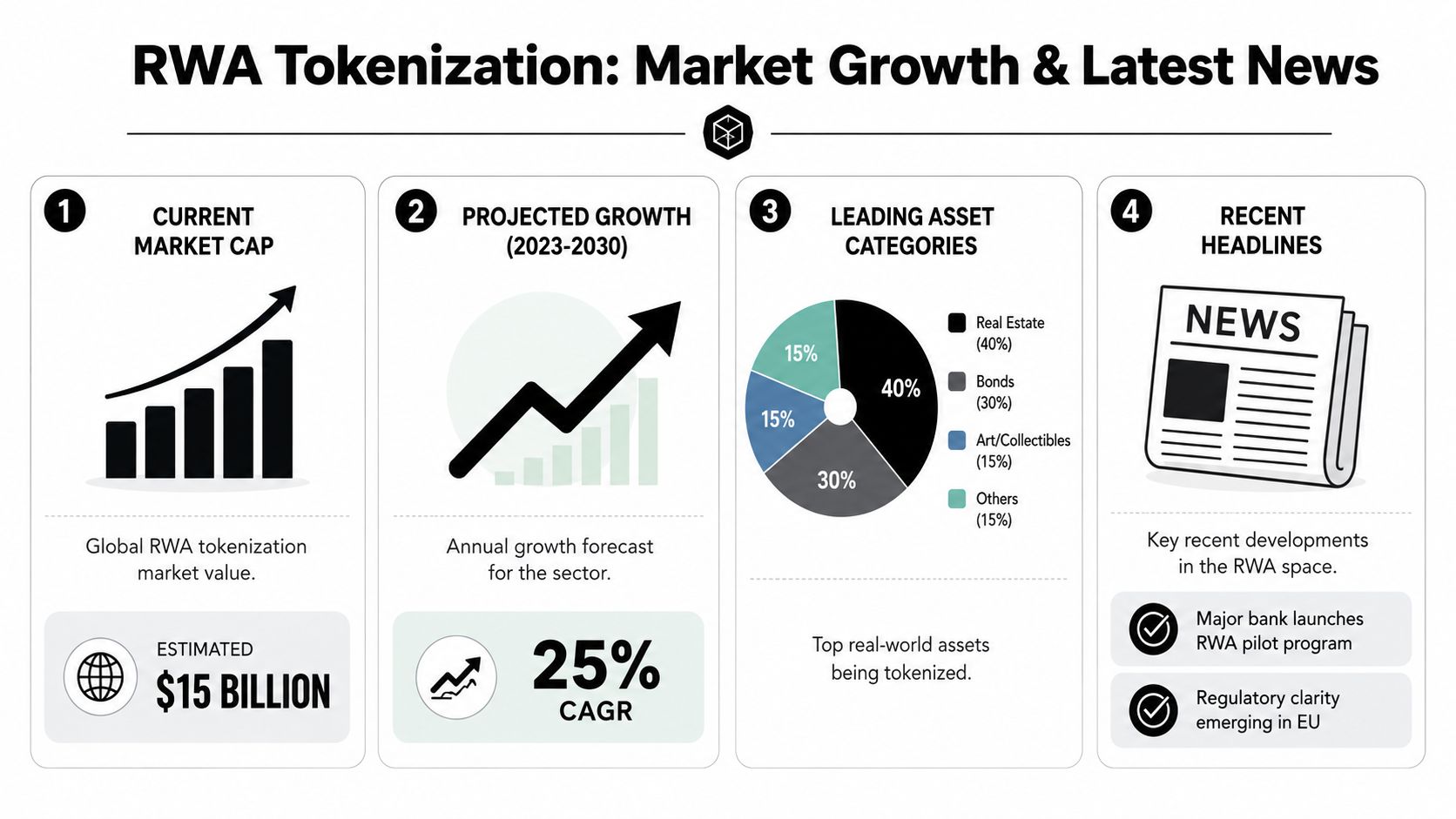

More than 40% of the on-chain RWA market now sits in tokenized US Treasuries, a concentration that says as much about who this market serves as how fast it is growing. The headline growth is real. Access is still narrow.

Recent RWA tokenization market coverage points to the same pattern. Capital is moving on-chain first through assets that institutions already understand, can price daily, and can fit inside existing compliance processes. That is why Treasury products and private credit have advanced faster than tokenized real estate or consumer-facing alternatives.

The growth curve also changed in quality, not just size. Early issuance focused on proving that off-chain claims could be represented on-chain. The current phase is about distribution, settlement efficiency, and regulated wrappers that make tokenized products acceptable to funds, fintechs, and corporate treasury desks. For investors, that distinction matters. Markets usually scale once the operational friction falls for large allocators, not when media attention peaks.

A useful benchmark comes from MetaMask's 2026 RWA overview, which notes that the on-chain RWA market value stood at $14.1 billion by the start of 2026. The same report says tokenized US Treasuries reached $12.88 billion in April 2026. In practice, that means the category is being defined by short-duration, yield-bearing instruments rather than by broad retail ownership of diverse real-world assets.

That concentration has two implications.

First, the market is maturing around products with low narrative risk and familiar legal treatment. Treasury exposure is easier to structure, easier to audit, and easier to explain than fractional claims on property, art, or small-business cash flows. Second, the retail investor paradox is becoming harder to ignore. The larger the RWA market gets, the more it resembles a digital upgrade for institutional distribution rather than an open investment rail for everyone.

This helps explain why so much recent infrastructure spending has centered on issuer tooling, compliance controls, and investor onboarding rather than permissionless access. Firms backed by top blockchain US investors are often building for regulated capital first because that is where demand, fees, and legal clarity are strongest.

This video gives helpful context on the broader trend:

Ethereum remains central for many of these products because issuers still value its custody integrations, token standards, and liquidity connections. But scale will depend on more than chain selection. If tokenized assets keep growing, the competitive edge will come from which platforms can combine compliance, secondary liquidity, and acceptable retail pathways without weakening the legal claim behind the token.

Leading RWA Platforms and Projects to Watch

The easiest way to understand the market is to watch the projects solving real distribution problems. Each major platform is taking a different route into tokenized finance. Some focus on private credit. Others concentrate on tokenized Treasuries, on-chain funds, or institutional lending rails.

Projects solving different market problems

Centrifuge has become one of the clearest examples of bringing private credit on-chain. Its relevance comes from translating off-chain receivables and credit exposures into structures DeFi can interact with more efficiently. It sits close to the part of the market where institutional underwriting and blockchain-based funding start to overlap.

Ondo Finance is often discussed as a gateway for tokenized Treasury exposure. That category matters because Treasury products are the cleanest bridge between crypto capital and traditional yield. The more demand shifts toward stable, regulated, cash-like instruments, the more platforms with Treasury-focused tokenomics gain strategic importance.

Maple Finance has built around on-chain credit markets and institutional borrower relationships. That makes it useful for watching how reputation, underwriting, and crypto-native infrastructure combine. It's less about the token itself and more about the architecture of a lending venue that can host real financial activity.

Goldfinch has long been relevant because it pushed beyond overcollateralized crypto lending and explored models linked to off-chain economic activity. In RWA terms, that's important. It forces the market to deal with actual borrower quality, legal recourse, and asset performance rather than purely on-chain collateral loops.

What to look for beyond the brand name

The strongest signal in this sector isn't social buzz. It's whether a platform can operate inside real institutional workflows. According to Dmitry Fedotov's analysis of recent RWA developments, over 15 operational pilots across six different currencies have been completed, and Ethereum wallet data showed a spike in new addresses created specifically to hold tokenized assets throughout late 2025 and early 2026.

That matters because it suggests RWA adoption is moving from pilot rhetoric into repeatable deployment.

When you evaluate projects, focus on:

- Asset quality: What exactly backs the token, and who verifies it?

- Legal enforceability: Does the token map cleanly to a real legal claim?

- Distribution model: Is the product built for institutions, accredited investors, or broader markets?

- Composability: Can the token interact with DeFi, custodians, and Layer 2 infrastructure?

- Backers and governance: A platform's network often shapes who can issue, distribute, and scale.

For readers tracking the capital networks behind these ecosystems, this directory of top blockchain US investors is useful context. It helps map which venture and strategic players are repeatedly showing up around tokenization infrastructure.

A broader stream of ecosystem coverage is also available through RWA tokenization analysis and updates.

The Shifting Regulatory and Market Implications

Technology got RWA tokenization started. Regulation is what made it credible to larger pools of capital.

The key policy shift in recent RWA tokenization news is that institutions no longer have to view blockchain rails as legally undefined territory. The market reached approximately $30 billion in AUM by mid-2026, with acceleration after the GENIUS Act in July 2025 established a federal framework for payment stablecoins and provided regulatory clarity, according to Chainalysis.

Why regulation became the unlock

That regulatory change mattered for two reasons.

First, settlement infrastructure became easier to standardize. Stablecoins are the cash leg of many tokenized transactions. Once that layer becomes clearer, issuers and allocators can structure products with less uncertainty around movement of value.

Second, legal clarity changed boardroom behavior. Institutions don't just care about blockchain efficiency. They care about whether compliance teams, auditors, and counterparties can support the process without creating new operational risk.

The emerging global standard is same risk, same regulation. In plain English, that means a tokenized Treasury or tokenized credit instrument shouldn't escape oversight only because it lives on-chain. If the economic risk resembles a traditional asset, regulators increasingly expect the same protections and supervisory perimeter.

Regulatory progress didn't make RWAs less financial. It made them more recognizably financial.

What changes in market structure

Once tokenized assets sit inside the regulatory perimeter, market design starts to change.

Traditional finance often separates distribution, execution, clearing, settlement, and custody across multiple firms and time windows. Tokenization can compress much of that activity into one programmable environment. That's why institutions care about 24/7 market access, near-instant settlement, reduced intermediary costs, and smart-contract-based compliance.

But better market plumbing doesn't remove all friction. It shifts the bottlenecks. Public blockchains still face scalability limits if tokenized markets grow much larger, and many institutions will still prefer permissioned environments for privacy, control, and governance.

For investors, this means regulation is no longer just a threat variable. It's now a key adoption variable. If you want a parallel lens on the infrastructure side of digital finance, crypto-friendly banks offer another way to think about how regulated and on-chain systems are converging.

Investor Risks and the Retail Access Paradox

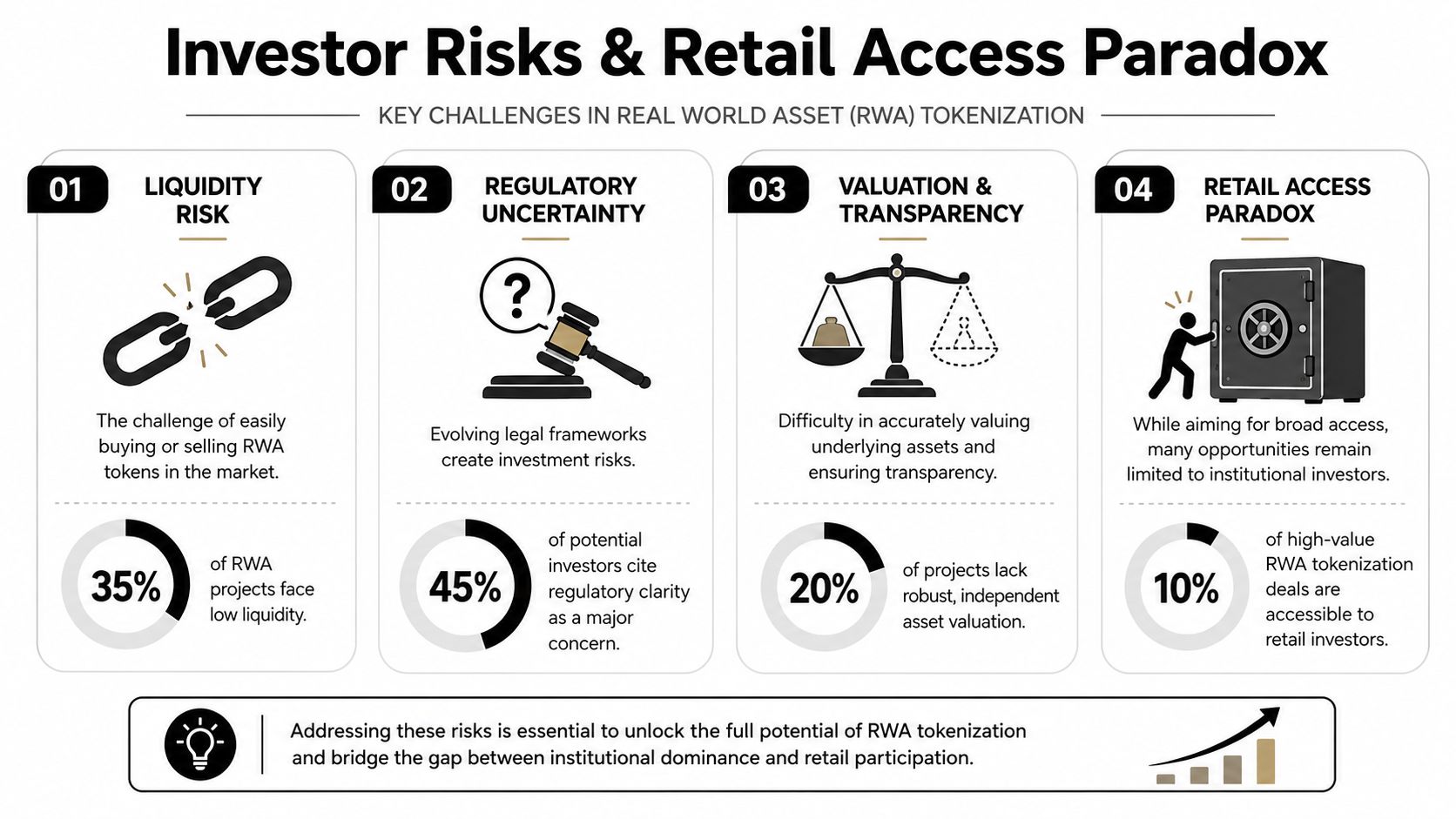

The bullish case for RWAs is strong. The market structure for retail investors is still weak.

This is the core paradox: tokenization promises fractional access and broader participation, yet much of the live market remains built around institutional onboarding, not consumer usability.

Why tokenized doesn't automatically mean liquid

A token can trade on a blockchain and still behave like an illiquid private placement.

That's already visible in the data. According to reporting summarized by Yahoo Finance, over 90% of tokenized assets remain illiquid, despite the growth narrative around the sector. The practical reason is straightforward. Many tokenized products have limited secondary markets, fragmented venues, unclear cross-border treatment, or buyer eligibility restrictions that shrink the pool of counterparties.

So when people hear “fractionalized” and assume “easily tradable,” they're often mixing up two separate things:

- Divisibility means an asset can be split into smaller units.

- Liquidity means someone is reliably there to buy from you when you want to exit.

Those aren't the same.

If your exit depends on a tiny whitelisted buyer pool, the blockchain wrapper doesn't solve your liquidity problem.

Why retail still sits outside the gate

The retail barrier is even sharper. The same Yahoo Finance reporting notes that over 85% of RWA tokens are held by fewer than 200 institutional addresses. That concentration reflects strict KYC and AML controls, geographic limitations, and high minimum investment thresholds in many live offerings.

This is the part of RWA tokenization news that deserves more scrutiny. Institutions are gaining access to cleaner settlement and programmable ownership, while retail investors are often left with the narrative rather than the product.

A realistic risk checklist looks like this:

| Risk area | Why it matters to investors |

|---|---|

| Liquidity risk | You may not have a functional secondary market |

| Compliance gating | Access can disappear by jurisdiction or investor status |

| Asset opacity | Token design may be clearer than asset quality |

| Valuation mismatch | On-chain representation doesn't guarantee clean price discovery |

| Platform dependence | Issuer, custodian, or venue problems can affect your rights |

The result is a two-speed market. Institutions get bespoke access to high-quality tokenized products. Retail users often get either no access or exposure to thinner, less proven offerings.

That's why due diligence matters more here than in many crypto narratives. Before touching any product, review the legal wrapper, redemption rules, transfer restrictions, and who controls the cap table. The same discipline that helps with avoiding crypto scams also applies to tokenized securities and quasi-securities. New wrappers don't eliminate old risks.

The Future of RWAs and Your Next Steps

The long-term outlook remains hard to ignore. According to FIBREE's market outlook, the global market for tokenized real-world assets is projected to reach $24 trillion by 2030, representing more than 7,000% growth from its 2024 valuation.

What the long view suggests

That projection doesn't guarantee a straight line upward. It does suggest that tokenization is moving toward a durable role in financial infrastructure.

The likely path forward looks uneven. Institutional products should keep leading. Layer 2 scaling solutions and more specialized settlement rails will matter more as throughput and compliance demands rise. AI plus crypto integration will likely improve reporting, risk monitoring, and operational automation around tokenized portfolios. DeFi protocols will keep trying to absorb parts of this market, especially where smart contracts can add efficiency without creating legal confusion.

The biggest open question isn't whether tokenization has a future. It's whether the next phase broadens access or makes capital markets more efficient for the same incumbent participants.

A practical checklist before you allocate

If you're following RWA tokenization news as an investor, use a stricter framework than you might use for a typical altcoin narrative.

- Check the legal claim: Know whether the token represents direct ownership, a fund interest, a note, or a contractual right.

- Study redemption mechanics: Find out how holders exit, who approves transfers, and whether secondary markets function.

- Review the asset base: Treasury exposure, private credit, commodities, and real estate all carry different risk profiles.

- Watch the infrastructure stack: Network choice, Layer 2 support, custody model, and oracle design all affect usability.

- Separate institutional success from retail opportunity: A strong market headline doesn't mean you can access the best products on fair terms.

RWA tokenization is becoming one of the most consequential themes in Web3. But the best opportunities won't go to the people who merely buy the story. They'll go to the people who understand the structure.

Coiner Blog is built for readers who want that kind of structure-first analysis. If you want more clear-eyed coverage of crypto, DeFi, tokenization, Layer 2 infrastructure, AI and blockchain, and the risks that get ignored in hype cycles, explore Coiner Blog.