Tokenized Real Estate Investing: 2026 Opportunities

Real estate has always been one of the largest and hardest-to-access asset classes. Now it's being rebuilt on blockchain rails. The headline number explains why serious investors are paying attention: the global real estate tokenization market was valued at USD 3.5 Billion in 2024 and is projected to reach USD 19.4 Billion by 2033, growing at a CAGR of 21%, and by 2030, real estate is forecasted to become the largest type of tokenized asset globally according to Custom Market Insights on real estate tokenization.

That forecast matters because tokenized real estate sits at the intersection of several major crypto themes at once: Web3 ownership, smart contracts, decentralized finance, digital identity, and increasingly, Layer 2 infrastructure. It also touches a pain point traditional finance never solved well. Property is valuable, but it's slow to buy, difficult to divide, and expensive to enter.

Tokenization promises a cleaner model. Instead of buying an entire building, investors can buy digital interests tied to it. Instead of waiting through traditional settlement cycles, ownership records can move through blockchain-based systems. If you already follow crypto, RWAs, or DeFi, this isn't just another niche narrative. It's one of the most credible attempts to connect blockchain with an asset class people already understand. For a broader grounding in the ownership layer behind this shift, Coiner Blog's guide to Web3 technology fundamentals is a useful companion.

Still, this market has a hype problem. Many tokenized property pitches borrow the language of crypto liquidity while ignoring the legal and operational realities of real estate. That gap is where intelligent investing starts.

Table of Contents

- The Dawn of a New Real Estate Era

- What Is Tokenized Real Estate Actually

- The Tech and Legal Mechanics Under the Hood

- The Investor's Dilemma Benefits vs Critical Risks

- The 2026 Market Landscape Who and Where to Invest

- A Practical Guide to Due Diligence

- The Future of Real Estate on the Blockchain

The Dawn of a New Real Estate Era

Why this market matters now

Real estate tokenization is already measured in the billions, and earlier forecasts point to a steep growth curve into the next decade. More important than the headline number is what it signals. The sector has moved out of the "concept demo" phase and into a period where capital formation, compliance design, and asset servicing matter more than crypto branding.

That shift is attracting attention for a practical reason. Traditional property investing has long been constrained by high minimums, slow transactions, fragmented paperwork, and limited access to deals outside an investor's local network. Tokenization tries to reduce those frictions by turning a property interest into a digital security or similar on-chain representation that can be issued, tracked, and in some cases transferred more efficiently.

The pitch is straightforward. Lower minimums, broader access, faster settlement, and a cleaner ownership record.

In practice, it is more uneven.

In strong offerings, tokenization improves distribution and administration. It can widen the investor base for a property vehicle, automate parts of compliance, and make cap table management less manual. For readers who want context on the broader infrastructure behind these systems, a basic understanding of how Web3 technology works helps explain why tokenized assets are structured as programmable records rather than static database entries.

But serious investors should separate access from liquidity. A token can be easy to buy and still hard to sell at a fair price. Secondary markets for tokenized property often look better in marketing materials than they do in live trading conditions, where thin order books, transfer restrictions, and limited buyer depth can leave holders with paper liquidity rather than usable liquidity.

What changed from old real estate investing

The change is not that buildings became digital. The ownership layer became more modular.

That distinction shapes the investment case. Tokenized real estate still depends on property managers, local law, tax treatment, tenant performance, insurance coverage, and physical maintenance. Blockchain can improve recordkeeping and transaction logic, but it does not repair a roof, resolve a zoning dispute, or fill a vacant unit.

For investors comparing shared ownership models outside crypto-native platforms, the Pie Assets fractional real estate overview is a useful reference point. It shows how fractional participation is framed in conventional property investing, which helps clarify what tokenization changes and what it does not.

A more accurate way to frame the shift is operational:

- Access broadens: Smaller check sizes can open deals to investors who would never buy an entire property or commit to a private real estate fund.

- Ownership can be divided more precisely: Issuers can structure many smaller interests instead of one large, illiquid position.

- Administration can be automated: Transfers, investor eligibility checks, and cash distribution workflows can be handled with coded rules and integrated service providers.

- Cross-border interest becomes more plausible: Investors can review offerings beyond their immediate geography, although securities rules and platform restrictions still apply.

Tokenization changes the interface to real estate. It does not remove the cost, legal burden, or operational messiness of owning it.

That context explains why the sector is drawing attention in 2026. Investors are looking for blockchain use cases tied to recognizable cash flows and legally enforceable claims. Tokenized property fits that demand better than many speculative crypto products. At the same time, the strongest opportunities will likely come from platforms that solve the unglamorous problems: who approves repairs, how reserves are funded, how fees stack up, and what exit options exist once the initial sale is over.

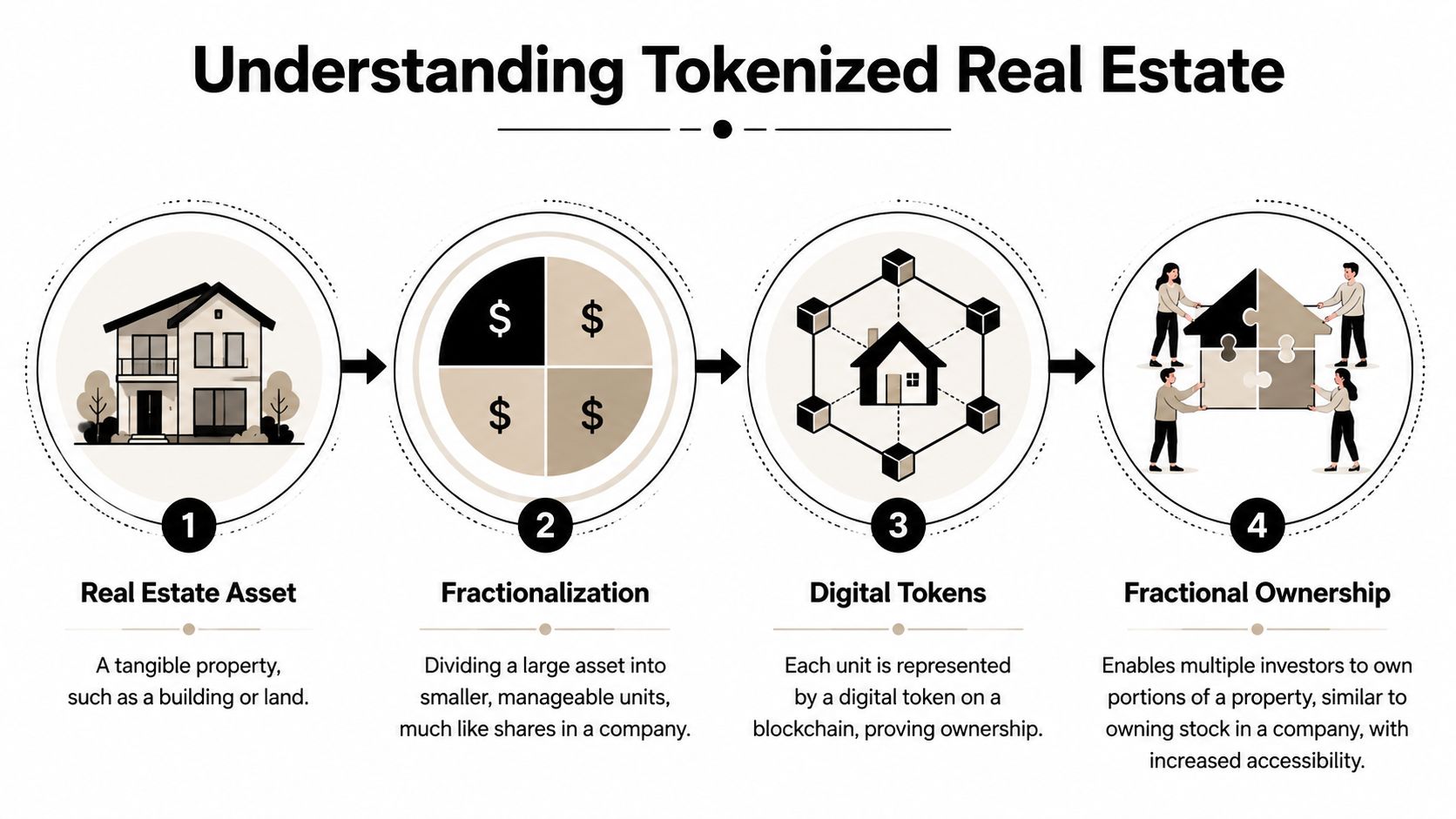

What Is Tokenized Real Estate Actually

Tokenized real estate converts a real-world property interest into digital tokens recorded on a blockchain. For investors, the key question is not whether the asset is on-chain. It is what legal and economic claim each token gives you.

In most offerings, the token represents a fractional interest in a property-owning structure or a right to receive part of the income that structure generates. The token is the delivery mechanism. The investment case still depends on the property's rent roll, vacancy risk, financing terms, operating costs, and the quality of the manager making day-to-day decisions.

That distinction matters because tokenization can make ownership easier to divide without making the underlying asset simpler to run. A leaking roof still needs cash. A delinquent tenant still hurts yield. A local regulator can still delay permits or raise compliance costs. Serious investors should read a tokenized deal the same way they would read any small private real estate offering, then add blockchain-specific questions on top.

For readers comparing structures, the Pie Assets fractional real estate overview is a useful baseline for understanding shared property exposure outside crypto-native packaging. It helps separate ordinary fractional real estate from the narrower case where ownership records, transfers, and investor servicing are wrapped in token infrastructure.

What the token changes, and what it does not

Tokenization changes how interests are issued, tracked, and sometimes transferred. It can also lower minimum investment sizes and widen distribution. That is the commercial pitch.

What it does not change is the operating burden sitting underneath the asset.

If a building needs repairs, someone still has to approve the work, fund reserves, oversee contractors, and absorb any budget overrun. In a fully owned property, that responsibility is obvious. In fractional structures, it can be diffuse. The practical answer usually sits in the issuer documents: the sponsor or property manager controls operations, expenses are paid from property cash flow or reserves, and investors have limited say unless governance rights are explicitly written in. That is one of the least glamorous parts of tokenized real estate, and one of the most important.

A simple process usually looks like this:

- A property or property-backed entity is selected

- Economic interests are divided into digital units

- Tokens are issued through blockchain-based infrastructure

- Investors purchase those tokens through a platform, subject to offering terms and transfer rules

That process can look cleaner on-screen than it feels in practice. A secondary market may exist, but depth is often thin, trading windows may be restricted, and buyers may need to meet eligibility rules before a transfer can clear. The result is a liquidity illusion. The asset appears more tradable than traditional private real estate, yet selling at a fair price on short notice can still be difficult.

For a broader explanation of how token issuance connects with financial infrastructure beyond property, Coiner Blog's piece on how tokenization is used in payments systems is a helpful reference. The shared thread is not the asset class itself. It is the use of digital representations to manage ownership records, transfer rules, and settlement workflows more efficiently.

Why investors keep getting this wrong

A tokenized property offering can look more transparent because balances, transfers, and distributions are presented through a dashboard or wallet interface. That presentation can hide the harder questions. Who controls the bank accounts. Who sets reserve policy. Who decides whether to refinance, sell, or delay maintenance. What rights do token holders have if the sponsor underperforms.

Those questions determine the investment more than the token standard does.

This is why tokenized real estate sits in a strange middle ground. It borrows the language of crypto, but its risk profile is still driven by old-fashioned real estate operations and private-market governance. The strongest offerings are usually the ones that make those mechanics plain, instead of selling fractional access as if it solved illiquidity, execution risk, and property management by itself.

The Tech and Legal Mechanics Under the Hood

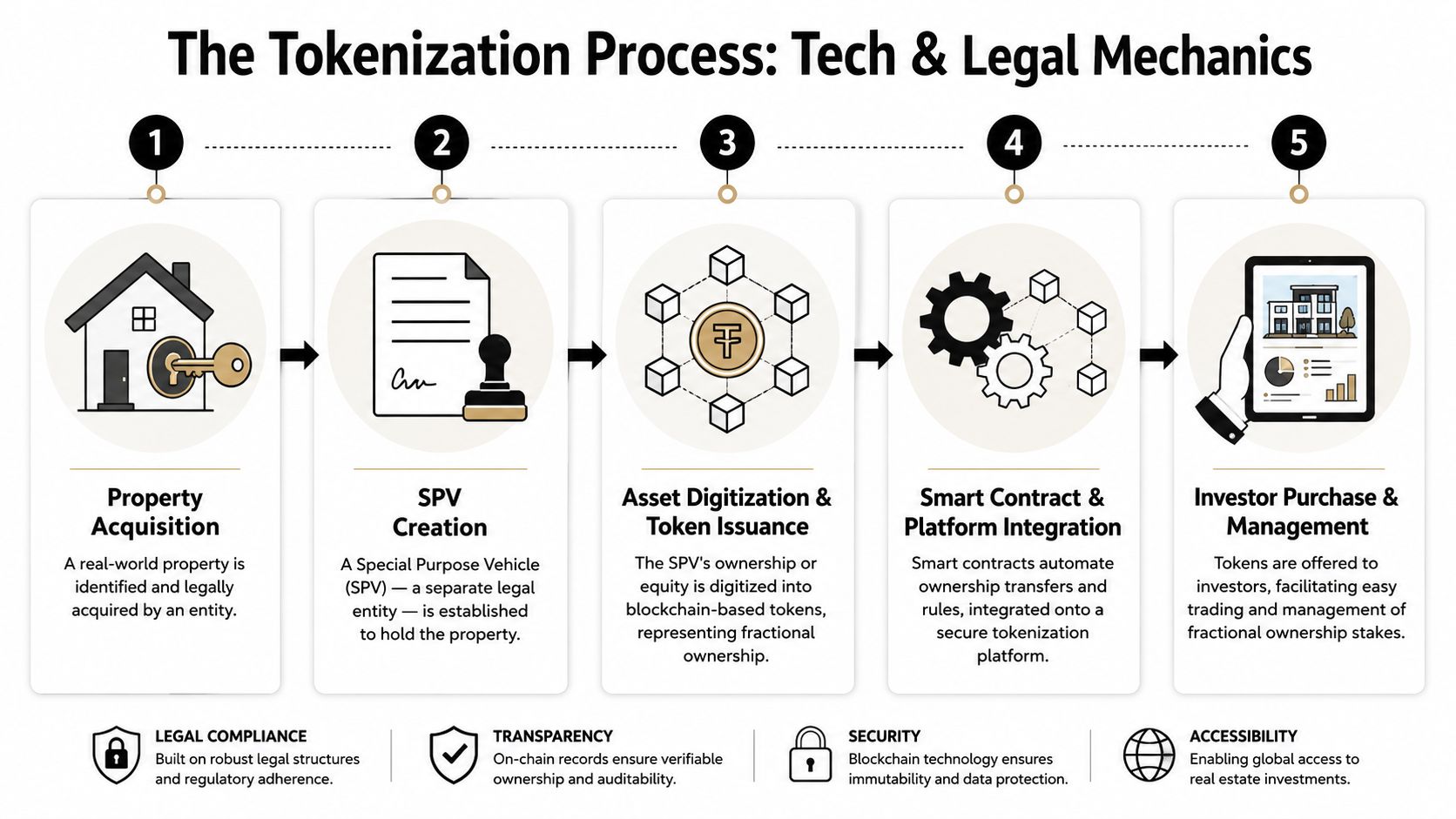

Why the SPV matters more than the token

The legal entity determines the investment. The token is only the delivery mechanism.

According to KPMG's real estate tokenization framework, a property is commonly placed inside a Special Purpose Vehicle, or SPV, so fractional interests can be issued in a legally defined way. Investors usually receive security tokens tied to equity or economic rights in that SPV, not direct title to the land or building.

That distinction sounds technical, but it drives nearly every outcome that matters. Cash distributions flow through the entity. Voting rights are defined in its operating agreement or shareholder documents. Liability sits at the property and SPV level. If the sponsor misses maintenance, delays repairs, refinances aggressively, or sells at the wrong time, token holders are relying on legal rights against an issuer structure, not direct control over a building.

This is also where many offerings create a liquidity illusion. A token can trade faster than a traditional private real estate interest, but only if transfer restrictions, securities laws, platform rules, and actual buyer demand allow it. In many cases, the blockchain record updates instantly while the actual exit remains sporadic.

For investors trying to understand how property firms are digitizing operations more broadly, digital transformation strategies for investors provide useful context on why real estate businesses are adopting new digital systems beyond token issuance alone.

How smart contracts handle ownership and cash flow

Once the legal structure is in place, smart contracts handle the administrative layer. They can enforce issuance rules, restrict transfers to approved wallets, record ownership changes, and automate parts of distribution processing.

The same KPMG report notes that tokenized real estate uses blockchain-based records to support verifiable ownership history and immutable transaction logs. That improves auditability, but investors should not confuse cleaner records with cleaner economics. Rent collection, tax payments, insurance claims, vacancy management, and repair decisions still happen off-chain.

A credible platform should explain at least four operating mechanics clearly:

- Investor onboarding: KYC, accreditation checks, and jurisdiction screening before tokens are issued

- Transfer controls: Rules on who can buy, hold, or resell the token, and when

- Distribution process: How rental income moves from property accounts to the SPV, then to token holders after fees, reserves, and expenses

- Governance triggers: What happens when the property needs capital, major repairs, refinancing, or a sale vote

The fourth point is often underexplained. Fractional ownership sounds efficient until the roof fails, a tenant leaves, or insurance covers less than expected. Someone has to approve the budget, hold reserves, and decide whether investors absorb lower distributions or contribute more capital. If the documents are vague on that question, the token structure has not solved the hard part of real estate investing.

Practical rule: If a platform describes the token standard in detail but is unclear about entity documents, reserve policy, servicing responsibilities, and dispute resolution, treat that as a serious diligence issue.

The blockchain layer still matters. Wallet control, settlement logic, and smart contract permissions shape how these assets move and who can interact with them. For a quick refresher on those mechanics, Coiner Blog's guide to blockchain technology basics is a useful reference.

Fungible tokens and NFTs serve different jobs

Token format follows ownership design.

As noted earlier in the KPMG framework, fungible tokens are generally used for fractional interests, while NFT-style structures fit single-asset representation better. The choice affects administration, transferability, and how investors should interpret what they own.

| Token format | Best fit | Investor implication |

|---|---|---|

| Fungible token | Fractional ownership | Easier to divide one asset into standardized units for many holders |

| NFT | Whole property representation | Better for singular ownership records or asset-level identification |

Income-focused offerings usually use fungible tokens because distributions, cap table management, and small minimum investments are easier to structure that way.

Still, the token standard is rarely the main risk. A polished ERC implementation can sit on top of weak governance, narrow voting rights, sponsor-controlled bank accounts, or redemption terms that leave holders stuck. In tokenized real estate, technical elegance is easy to market. Operational accountability is harder to build, and far more important.

The Investor's Dilemma Benefits vs Critical Risks

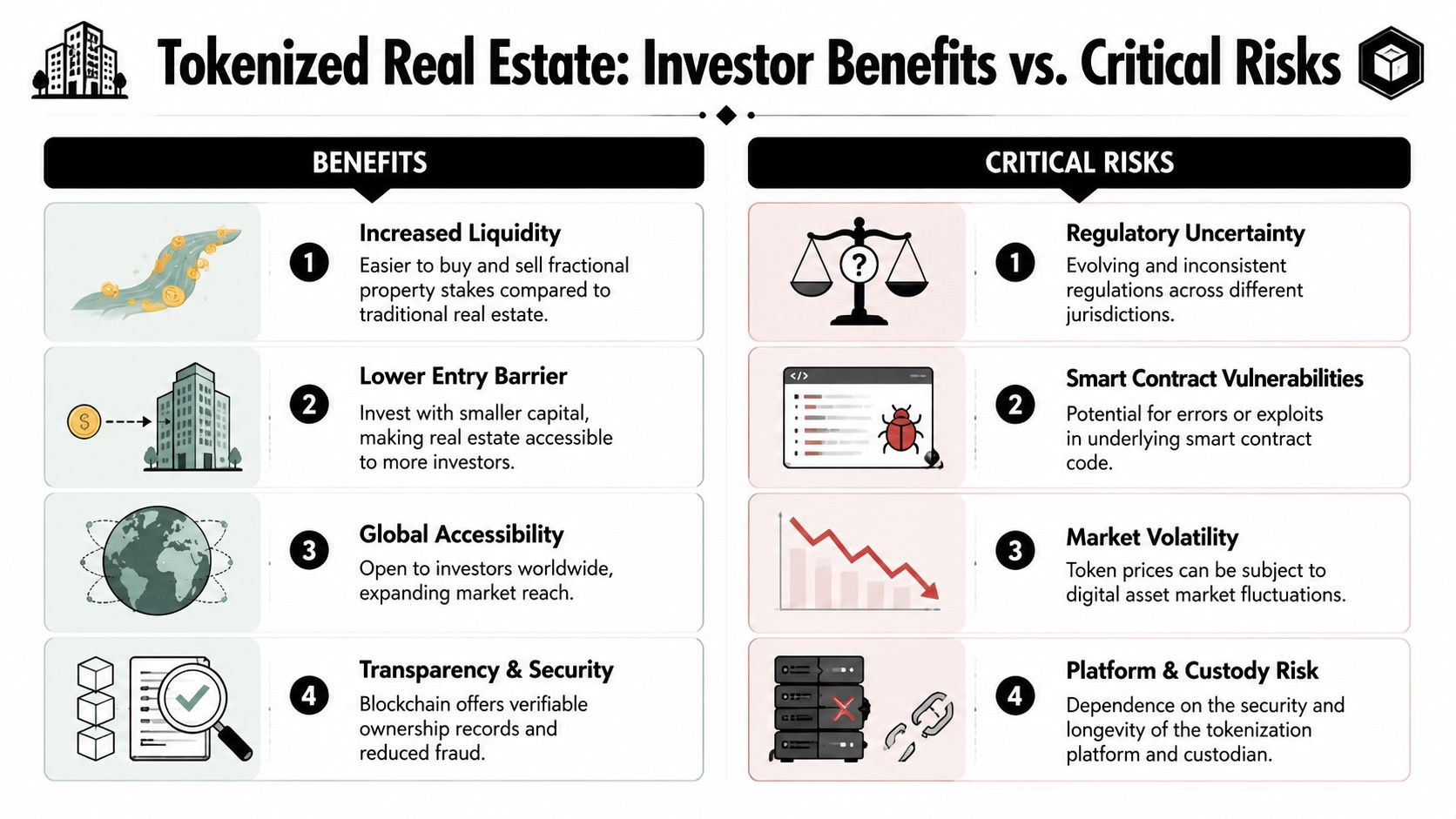

What investors like about the model

Tokenized real estate gets attention because it solves several obvious inefficiencies in one move. It can lower the entry barrier, make ownership more divisible, and create a cleaner digital layer for transfer and reporting. For investors who already hold crypto, it also offers exposure to a real-world asset class without leaving the blockchain environment entirely.

Some of the appeal is practical rather than ideological:

- Smaller ticket sizes: Investors don't need to buy an entire property to gain exposure.

- Operational transparency: Blockchain records can make holdings and transaction history easier to audit.

- Cross-border reach: Platforms can attract participants beyond a single local market, subject to compliance limits.

- Programmable ownership: Smart contracts can automate parts of administration that are slow in traditional property systems.

There's also a broader portfolio logic here. Property-backed tokens can appeal to people who want something more tangible than purely narrative-driven crypto assets. In a market where many tokens depend on sentiment, real estate offers an asset class with familiar value drivers like occupancy, rents, financing, and asset management.

The liquidity illusion is real

This is the part most marketing pages soften.

According to a discussion of security token liquidity constraints, tokenized real estate often promises liquidity, but many real estate tokens are Reg D securities that cannot be traded on major exchanges like Coinbase or Uniswap. That creates what the source describes as a “liquidity illusion”, where investors hear the language of 24/7 blockchain markets but face restricted and underdeveloped secondary venues in reality.

That difference changes the investment profile completely. A token may be technically transferable on-chain and still be practically hard to exit.

Buying a tokenized property stake is not the same as buying a liquid crypto asset. The settlement layer may be digital, but the exit path may still be narrow.

Here's the sober version of the promise-versus-reality comparison:

| Claim investors hear | What to verify |

|---|---|

| “You can trade it anytime” | Which marketplace actually supports trading, and who is eligible to use it |

| “Liquidity is unlocked” | Whether secondary demand exists beyond issuer marketing |

| “Blockchain makes it frictionless” | Whether securities rules impose holding periods or transfer restrictions |

| “It works like crypto” | Whether it behaves more like private placement paper than a native token |

Other risks most pitch decks underplay

Liquidity isn't the only issue. There are other weak points serious investors should examine before buying.

First, smart contract risk still exists. If payout logic, transfer restrictions, or wallet controls are implemented poorly, the user experience and legal enforceability can break down. This doesn't mean every project is unsafe. It means code quality matters, especially when the code governs a regulated asset.

Second, platform risk is often understated. Many buyers don't just depend on a token. They depend on the issuer portal, custody flow, compliance stack, reporting layer, and investor support team. If that platform fails operationally, the token alone won't save the experience.

Third, fraud and misrepresentation risk remains relevant, especially in a market where polished dashboards can hide weak fundamentals. If you need a broader checklist for recognizing low-quality crypto offers, Coiner Blog's guide on how to avoid crypto scams is highly relevant here.

The upside in tokenized real estate is real. So is the need for skepticism.

The 2026 Market Landscape Who and Where to Invest

The main platform models in the market

Tokenized real estate in 2026 is splitting into a few very different businesses, and investors who treat them as interchangeable usually misprice the risk.

One branch focuses on single-property fractional ownership. The pitch is straightforward: buy a small slice of a rental property and collect a share of the income. In practice, returns depend less on the token and more on occupancy, property management quality, maintenance reserves, and the legal claim attached to the SPV behind the offering.

Another branch targets commercial and development assets. These deals often look more complex, but they can add layers of uncertainty. Cash flow may be uneven, refinancing risk can matter more than rental yield, and investors may be exposed to project execution rather than stabilized income.

A third model is fund tokenization. Here, the token usually represents an interest in a managed vehicle that holds multiple assets. That can reduce single-asset concentration risk, but it also creates another question serious buyers should ask: are you paying for real diversification, or just another wrapper around a conventional private real estate fund?

Those differences shape the actual investment experience. They affect reporting frequency, rights to distributions, transfer restrictions, governance, and how disputes get handled when something goes wrong.

What serious investors are screening for

The strongest issuers in this market are not winning on branding alone. They are winning by making the unglamorous parts legible.

Investors with experience in private markets are screening for clear legal documentation, audited cash flow reporting, a defined servicing process, and realistic disclosure on resale options. They also want to know who handles onboarding and compliance, especially where token transfers depend on wallet screening and investor verification. Platforms that already explain their blockchain identity verification process for compliant token transfers tend to look more credible than platforms that market liquidity first and explain restrictions later.

A practical comparison framework looks like this:

| Platform Type | Primary Asset Focus | Typical Min. Investment | Secondary Market Status |

|---|---|---|---|

| Fractional residential platform | Single-family homes or small rental properties | Usually aimed at lower-ticket participation | Often thin, issuer-controlled, or subject to transfer limits |

| Commercial asset platform | Office, retail, hospitality, or larger buildings | Usually more selective and deal-specific | Depends heavily on jurisdiction, deal terms, and buyer availability |

| Tokenized real estate fund platform | Diversified fund exposure | Often tied to accreditation or qualification rules | May offer more structured transfers, but still behaves more like private securities than exchange-traded crypto |

The secondary market point deserves more skepticism than it usually gets. A listing venue is not the same thing as dependable liquidity. In many offerings, the number of actual buyers is small, spreads can be wide, and sale windows may depend on issuer approval or compliance checks. That creates a liquidity illusion. The token looks tradable on paper, while the investor still faces private-market exit conditions in practice.

Geography also matters, but not for the usual marketing reason. The issue is not merely whether a jurisdiction is "crypto-friendly." The better question is whether securities treatment, investor eligibility rules, custody expectations, and enforcement pathways are already clear. Markets with clearer rules may feel slower, yet they often produce more investable products because issuers have less room to stay vague about rights and responsibilities.

That last point becomes especially important in fractional ownership. If a property needs a new roof, a major plumbing repair, or a vacancy-driven cash injection, the token structure does not make the bill disappear. Someone still decides whether reserves cover it, whether investors are diluted, whether distributions pause, or whether the asset is sold. The platforms worth watching in 2026 are the ones that explain those mechanics before investors ask.

A Practical Guide to Due Diligence

Questions that matter before you buy

Most tokenized real estate guides spend too much time explaining blockchain and not enough time explaining what can go wrong after closing. Due diligence starts with one question: what exactly are you buying?

You need to identify whether the token gives you equity in an SPV, exposure to income, a debt-style claim, governance rights, or some combination of those. If the answer is fuzzy, stop there. Ambiguity at the rights level becomes confusion at the payout level.

A disciplined review should cover:

- Asset clarity: What property or portfolio sits underneath the token?

- Valuation method: How is the underlying asset priced, and how often is that view updated?

- Issuer credibility: Who operates the platform, who manages the property, and what legal framework governs the deal?

- Transfer rules: Can holders resell, and under what restrictions?

- Distribution mechanics: How are proceeds routed, and what gets deducted before investors receive anything?

The repairs and fee problem nobody wants to lead with

One of the most important unresolved issues in the sector is refreshingly simple: who pays when the roof leaks?

A real estate finance discussion highlighting operational ambiguity points directly to the investor concern many platforms avoid. The recurring question is “who pays for repairs, taxes, and management fees?” The same discussion notes a lack of standardized frameworks for distributing these costs among fractional holders, creating legal ambiguity and the possibility of unexpected liability.

That isn't a minor detail. It's central to expected returns.

If a platform advertises rental income but doesn't clearly explain maintenance reserves, taxes, insurance, and management deductions, you do not yet understand the investment.

The operational stack in tokenized real estate still depends on off-chain execution. Tenants still pay rent. Contractors still fix things. Property managers still invoice someone. Tokenization doesn't remove these realities. It only changes how claims on the economics are packaged and distributed.

What a solid offering should make easy to verify

The best issuers reduce guesswork. They provide documents that spell out who controls the SPV, how rights are allocated, what fees come off the top, what events can trigger changes, and how investor identity is verified.

Identity and compliance aren't side topics here. They're central to whether the asset can operate legally at scale. For readers exploring that infrastructure layer, Coiner Blog's explainer on blockchain identity verification is useful background because compliant RWA markets depend heavily on wallet-level eligibility controls.

A practical due diligence checklist looks like this:

- Read the legal documents first. Marketing copy is not the investment.

- Map the cash flow path. Know where rent or proceeds go before they reach token holders.

- Inspect fee language carefully. Acquisition, servicing, management, and maintenance costs can materially alter outcomes.

- Test the exit assumptions. If the platform mentions secondary trading, verify how that works in reality.

- Check the operational counterparties. Property managers, custodians, and administrators matter as much as the token contract.

Most investors lose money in complex products for ordinary reasons. They misunderstand rights, fees, or liquidity. Tokenized real estate isn't exempt from that rule.

The Future of Real Estate on the Blockchain

AI Layer 2 and DeFi will reshape the category

The next phase of tokenized real estate probably won't be driven by better marketing. It'll be driven by better infrastructure.

AI will likely play a growing role in property analysis, document review, risk flagging, and predictive maintenance workflows. That doesn't mean AI can magically price every building perfectly. It means platforms can use AI-assisted systems to improve underwriting consistency and operational monitoring around real assets.

Layer 2 networks matter for a different reason. If tokenized real estate is going to support more frequent transfers, lower-cost settlement, and broader investor participation, transaction efficiency becomes important. Layer 2 infrastructure can make that environment more usable without abandoning the security assumptions of larger blockchain ecosystems.

DeFi is the final piece, though it has to be handled carefully. The most interesting long-term outcome is composability. A property-linked token that is legally sound, identity-gated, and technically interoperable could become collateral, treasury inventory, or part of structured on-chain credit products. That would move tokenized property from static holding vehicle to active financial primitive.

What tokenized property could become

The strongest long-term case for this sector isn't that every building will trade like a memecoin. It's that real estate ownership and administration can become more modular, more transparent, and easier to integrate into digital finance.

There's already evidence that the market sees that direction. Deloitte's tokenized real estate outlook projects tokenized real estate could reach $4 trillion by 2035, and that private real estate funds alone could reach US$1 trillion by 2035 with 8.5% market penetration within asset management. Those are projections, not guarantees. But they show how seriously mainstream finance is taking the category.

The winners won't be the platforms that promise frictionless magic. They'll be the ones that solve the hard parts: compliance, rights enforcement, cash flow transparency, and credible secondary market structure.

Tokenized real estate is one of the clearest examples of where blockchain becomes useful when it stops trying to replace reality and starts organizing it better.

Coiner Blog covers the part of crypto that matters most to serious readers: where blockchain meets actual utility, real markets, and real risk. If you want more grounded analysis on RWAs, DeFi, Web3 infrastructure, AI integration, and the mechanics behind emerging digital asset sectors, explore the latest insights on Coiner Blog.

2 Comments