Cryptocurrency ramblings

What Is Terra? Understanding LUNA, UST, and Terra 2.0

A beginner searching “What is Terra?” can land in three completely different worlds: a NASA satellite, a Roman-root word for earth, or one of crypto's most consequential case studies. In digital assets, that ambiguity matters because Terra wasn't just another blockchain. It became a symbol of how fast an ecosystem can rise, how violently flawed tokenomics can break, and how difficult it is to rebuild after trust collapses.

Table of Contents

- Untangling the Name Terra

- The Original Vision Behind the Terra Blockchain

- The Rise of a DeFi Behemoth and the Anchor Effect

- The Great De-Peg The Anatomy of a Crypto Collapse

- Terra 2.0 vs Terra Classic Understanding the Fork

- What Is the Terra Ecosystem Today

- Lessons Learned and How to Approach Terra Safely

Untangling the Name Terra

Why the name creates instant confusion

The first problem with “what is Terra” isn't technical. It's linguistic.

“Terra” can mean earth or land in general language, and it also names NASA's Terra satellite, a flagship Earth Observing System mission launched on 18 December 1999 that has delivered long-term climate, land, ocean, and atmosphere records for more than two decades, according to NASA's Terra mission overview. That satellite matters because its multi-decade continuity helps researchers study interannual variability and decadal trends, which short observation windows can't reveal.

For crypto readers, that overlap creates a search problem. A beginner may type “what is Terra” and expect a blockchain explainer, but search results often blend the satellite, the word itself, and the crypto ecosystem into one muddy definition.

Why crypto readers need a sharper definition

In blockchain, Terra refers to the ecosystem built around LUNA and, historically, TerraUSD (UST). That distinction matters because there are really two separate questions hidden inside one search query:

- What was Terra? The original stablecoin-centric network built around UST and LUNA.

- What is Terra now? The post-collapse proof-of-stake chain that kept the Terra name but dropped the old algorithmic stablecoin model.

- What are people asking? Often, they're trying to resolve uncertainty left behind by the 2022 collapse rather than learn a simple definition.

The hard part of understanding Terra isn't learning a new token ticker. It's separating an old economic design from the chain that exists today.

That's why Terra remains such an important case study in Web3 and DeFi. Most blockchain projects are remembered for what they built. Terra is remembered for both what it built and what it broke. The result is a knowledge gap that still confuses retail users, developers, and even experienced market participants when they encounter LUNA, LUNC, UST, or USTC on exchanges and wallets.

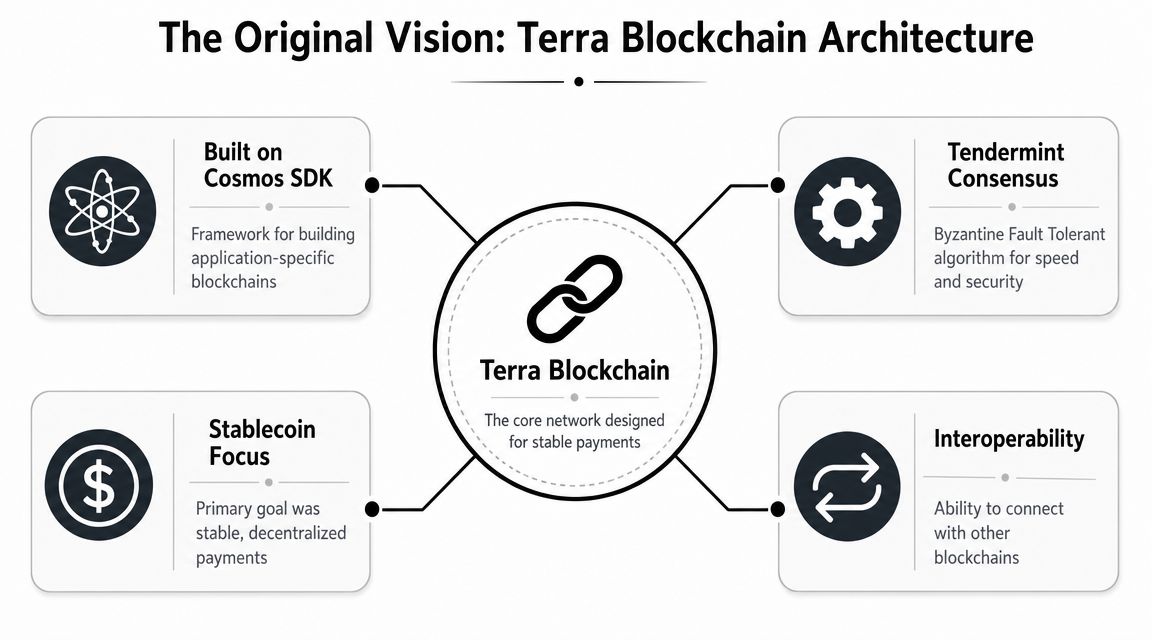

The Original Vision Behind the Terra Blockchain

The product idea that made Terra compelling

Terra began with a persuasive answer to a real crypto problem. Traders wanted an on-chain dollar they could move through applications without leaving the blockchain economy. Developers wanted a base asset for payments, lending, and trading that would not swing in value like a typical governance token.

The project's pitch was to supply that asset natively. Rather than treat stablecoins as external infrastructure imported from another chain or backed by a custodian, Terra made the stable asset the center of the network's design. That choice shaped everything around it, from tokenomics to application strategy.

That vision also matched a broader market belief at the time. Bitcoin was increasingly viewed as a store-of-value asset. Ethereum had become the main smart contract platform. Terra presented itself as a more specialized chain, built around a specific monetary use case rather than a general-purpose thesis. For readers who want more context on the underlying mechanics, this guide to blockchain technology basics explains why application-focused ecosystems once looked so credible.

How UST and LUNA worked together

At the center of the original system was a dual-token structure.

UST was meant to function as the stablecoin. LUNA was the volatile asset designed to absorb changes in demand and support the peg through an on-chain mint-and-burn relationship. If UST traded above $1, arbitrageurs had an incentive to create more UST. If it traded below $1, they could swap UST for LUNA and remove UST from circulation. In theory, those trades would pull the price back toward parity.

The mechanism was simple enough to explain and ingenious enough to attract serious attention. It offered a version of stability that did not depend on holding equivalent dollars or short-term Treasuries in reserve.

Why that design looked elegant at first

On paper, Terra solved two problems at once. It aimed to create a decentralized stablecoin while also creating demand for the network's native asset.

That was the deeper appeal. Terra was not only trying to hold a peg. It was trying to build an entire monetary system in which usage, liquidity, and token value reinforced one another. If demand for UST grew, LUNA could benefit. If LUNA remained valuable, confidence in the stabilizing mechanism could persist. In strong markets, that reflexive structure looked efficient rather than dangerous.

Analyst view: Terra's core innovation and its central weakness were the same. The system depended on market confidence remaining strong enough for arbitrage and LUNA demand to keep doing the work that hard reserves would have done in a collateral-backed model.

That distinction matters because it explains both phases of Terra's story. The original chain rose quickly because the design looked economically elegant and capital-efficient. It later failed for the same reason. Once confidence weakened, the system had far less room to absorb stress than many users assumed.

The Rise of a DeFi Behemoth and the Anchor Effect

Why capital flooded into Terra

Terra's breakout was not driven by technical design alone. It was driven by a product that gave ordinary users a simple reason to buy UST, move it on-chain, and keep it there.

That product was Anchor Protocol.

Anchor turned Terra's monetary design into a user acquisition engine. For many participants, the chain was less important than the offer. UST could be deposited into Anchor for yield, and that made Terra easier to understand than many competing Layer 1 ecosystems, which often had activity but no single application strong enough to pull in sustained capital. Terra had one.

That distinction matters. Blockchains usually grow in fragments, through developers, infrastructure, and slow liquidity formation. Terra grew through a clearer loop. Demand for UST supported activity on the chain. Activity on the chain made Terra look credible. That credibility drew in more capital.

Mirror and other applications added breadth, but Anchor supplied the gravitational center. It gave the ecosystem a flagship use case and helped create the impression that Terra was becoming a full financial system rather than a chain with an interesting stablecoin experiment attached to it.

The flywheel that made Terra feel unstoppable

At its peak, Terra looked large enough to be permanent. Market trackers such as CoinGecko's TerraUSD page captured how much capital had accumulated around UST before the collapse, while LUNA had also become one of the market's most watched assets. The combined scale mattered less as a headline number than as a signal. Terra had crossed from niche protocol to systemically visible crypto ecosystem.

The flywheel was easy to describe and hard to stop while sentiment remained positive:

- UST demand rose because Anchor gave users a concrete reason to hold the stablecoin.

- LUNA gained reflexive support because it sat underneath the mint and burn structure and absorbed part of the ecosystem's growth narrative.

- On-chain activity and trading depth improved, which made Terra appear stronger to traders watching the liquidity of cryptocurrency across major ecosystems.

- Confidence spread outward as rising usage, rising valuations, and rising attention all appeared to confirm one another.

This is why Terra became such an important case study. The system did not grow only because users believed in algorithmic stablecoins. It grew because yield, liquidity, token appreciation, and social proof lined up at the same time.

That combination can look like product-market fit even when part of the demand is incentive-dependent.

Analyst view: Terra's rise showed how quickly a blockchain can scale when its core financial product is legible to users and profitable in the short term. It also showed that adoption built on a narrow demand base can be mistaken for resilience.

Many participants treated the flywheel as evidence that Terra had solved stablecoin design. A more careful reading is that Terra had solved distribution. Those are very different achievements. Distribution can produce extraordinary growth. It cannot, by itself, guarantee that the system can survive stress.

The Great De-Peg The Anatomy of a Crypto Collapse

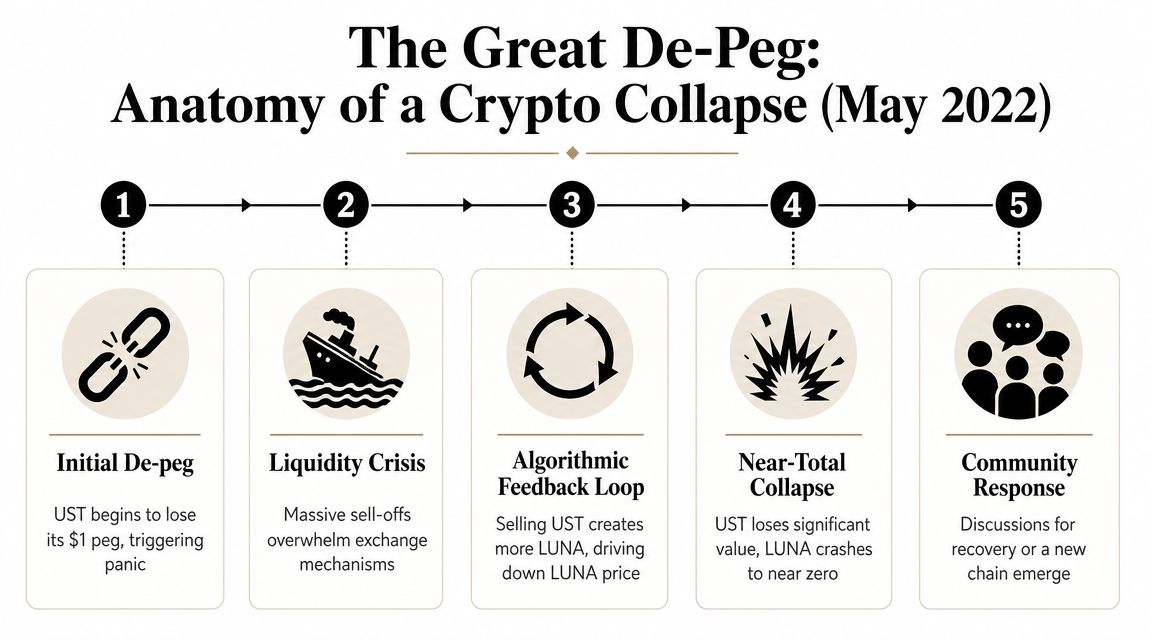

How the de-peg turned into a death spiral

For a period, Terra looked like one of crypto's cleanest stories. Then the mechanism at the center of that story reversed direction. The same mint and burn design that had supported expansion became the channel through which confidence left the system.

UST depended on market incentives, not conventional dollar reserves, to hold its peg, as noted earlier. That distinction mattered most when holders no longer wanted to wait for the mechanism to work.

The collapse followed a sequence that was simple in structure and brutal in effect:

- UST traded below $1. A stablecoin can survive small deviations. It struggles once users begin to treat the deviation as a warning instead of a short-lived pricing gap.

- Redemptions and market selling accelerated. Some holders sold UST on the open market. Others used the protocol design to exit through LUNA.

- LUNA supply expanded quickly. New issuance was supposed to absorb stress. In practice, it increased the amount of LUNA the market had to price during a panic.

- LUNA lost value as supply rose and confidence weakened. That reduced faith in LUNA's ability to act as the system's shock absorber.

- The arbitrage loop stopped stabilizing the peg. As confidence fell in both assets, each round of redemptions produced more selling pressure rather than relief.

This was a bank run translated into token mechanics.

The broader cryptocurrency bear market behavior of that period made the situation worse. Risk appetite was already falling across digital assets, so Terra faced stress in a market less willing to fund recovery attempts or give complex designs the benefit of the doubt.

Why the mechanism failed under stress

The failure was not a mystery of code. It was a failure of assumptions.

Algorithmic stabilization depends on traders believing the asset received in redemption will retain enough value to make the trade rational. Once that belief breaks, arbitrage no longer looks like a low-risk profit opportunity. It looks like catching a falling asset in exchange for one that has already lost its peg.

That is what made Terra different from an ordinary market drawdown. The system's defense required confidence in LUNA at the exact moment confidence in LUNA was disappearing. As more UST sought exit, more LUNA was created. As more LUNA was created, the market assigned it a lower value. That weakened the very backstop meant to restore UST.

Practical rule: A stablecoin mechanism holds only as long as the market is willing to own the asset that absorbs redemptions.

The episode became a defining case study in stablecoin design because it exposed a hard limit. Reflexive systems can expand quickly when demand is rising, but they can contract faster than expected when confidence, liquidity, and market depth deteriorate together.

For a visual breakdown of the collapse sequence, this video summarizes the event timeline:

What the market learned in real time

Terra changed the standard for crypto due diligence. Before the collapse, many participants focused on growth, yield, and adoption metrics. After it, the more serious question became whether the system could survive a coordinated exit.

That shift led investors, developers, and regulators to ask better questions:

- What supports the peg if traders refuse to hold the balancing asset?

- Who carries losses when redemptions spike?

- Is demand broad-based, or does it depend heavily on one product or one incentive?

- Can governance and token design still function during a crisis, not just during expansion?

Those questions still shape how the market evaluates algorithmic stablecoins and high-growth crypto ecosystems. Terra's collapse did not end experimentation. It separated fast adoption from durable design, which is the distinction needed to understand both the original Terra and the chain that exists today.

Terra 2.0 vs Terra Classic Understanding the Fork

The split that defined post-collapse Terra

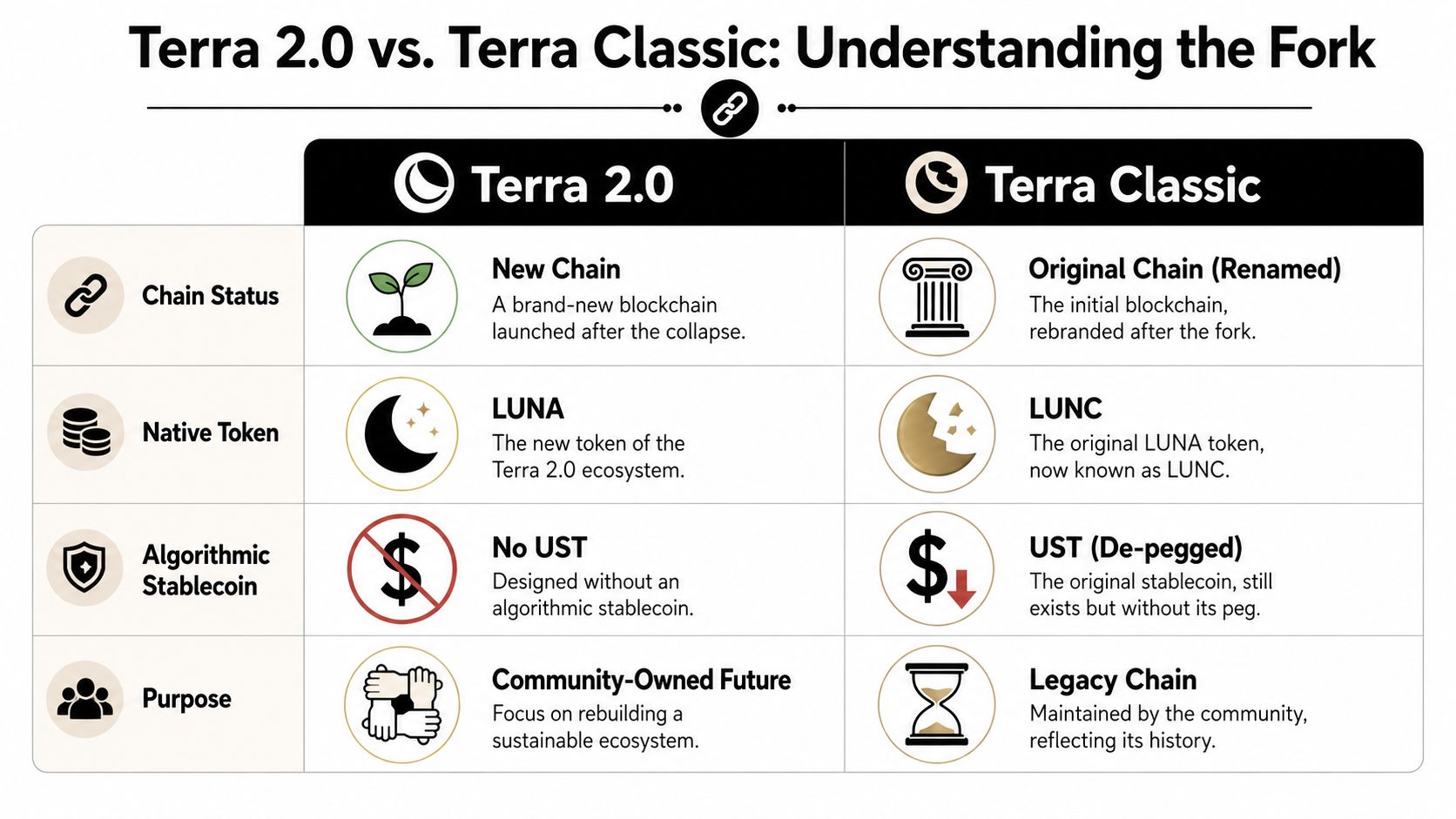

After the collapse, the Terra community faced a problem that was both technical and reputational. The original chain still existed, but the old economic design had become inseparable from failure. The answer was a fork that produced two different identities under the same broad brand memory.

That's where much of today's confusion comes from.

Terra Classic is the original chain under a new name. Its tokens were renamed, including LUNA Classic (LUNC) and TerraClassicUSD (USTC).

Terra, often called Terra 2.0 in market conversation, is the newer chain launched after the collapse. Its key distinction is straightforward: it moved away from the algorithmic stablecoin model that defined the old system.

A side-by-side comparison

| Feature | Terra 2.0 | Terra Classic |

|---|---|---|

| Chain identity | New chain | Original chain, renamed |

| Main token | LUNA | LUNC |

| Stablecoin model | No algorithmic UST-centered design | Legacy chain tied to the old stablecoin history |

| Primary narrative | Rebuild as a standard proof-of-stake ecosystem | Preserve and manage the legacy network |

That comparison clears up the surface-level confusion, but the more important insight is strategic.

Terra 2.0 isn't just a software fork. It's an attempt to separate brand continuity from economic continuity. The network kept the name recognition of Terra while trying to leave behind the exact design that made the original ecosystem famous.

The fork created two realities. One chain preserved the historical record. The other tried to preserve developer and community momentum without preserving the old stablecoin thesis.

That distinction matters if you're scanning exchange listings, evaluating governance proposals, or deciding whether current LUNA activity reflects a fresh Layer 1 story or a residual meme around a historic collapse. In practice, many retail users still confuse the two, and that confusion remains one of the biggest barriers to serious ecosystem recovery.

What Is the Terra Ecosystem Today

What the new Terra actually is

Today, Terra presents itself as an open-source proof-of-stake blockchain where LUNA is used for staking, governance, and transaction-fee rewards, according to Terra protocol documentation. That's the cleanest answer to the present-tense version of “what is Terra.”

In other words, the current Terra isn't primarily a stablecoin experiment. It's trying to operate like a more conventional Layer 1 network inside the broader Cosmos-oriented blockchain ecosystem. The emphasis now is utility, validator participation, governance, and application development rather than defending a synthetic dollar peg.

For readers mapping this onto broader industry themes, that places Terra closer to the usual Web3 playbook of on-chain apps, staking economics, and community governance. A broader explainer on what Web3 technology means helps frame why that repositioning matters.

The real challenge is identity not technology

The hard part isn't defining the chain's current mechanics. The hard part is convincing the market to judge those mechanics separately from the old collapse.

That's why Terra remains such an unusual case study. Many blockchain rebrands try to signal progress. Terra has to argue for discontinuity while using the same name. That creates a persistent credibility gap for anyone evaluating whether the chain is “different now.”

A practical way to think about current Terra is through three lenses:

- As infrastructure: It now resembles a standard proof-of-stake network more than a stablecoin machine.

- As governance: LUNA's role is tied to participation, validator incentives, and chain-level decisions.

- As reputation: The 2022 collapse still shadows every product, partnership, and market narrative attached to the name.

The new Terra's central problem isn't a lack of category. It fits a familiar Layer 1 template. Its problem is that the market remembers the previous category more vividly than the current one.

That also affects how Terra competes in newer narratives. AI and crypto integration, Layer 2 scaling, and tokenization of real-world assets are all attracting attention across the industry, but Terra can't participate in those conversations on equal footing unless it first solves the trust issue. In blockchain markets, technical recovery is possible. Narrative recovery is slower.

Lessons Learned and How to Approach Terra Safely

A practical checklist for users and investors

Terra taught the crypto market a blunt lesson: don't confuse elegant tokenomics with resilient tokenomics.

If you're evaluating Terra today, or any DeFi ecosystem with ambitious financial design, focus on process over story.

- Separate the chain from its history: Know whether you're looking at LUNA, LUNC, USTC, or older Terra content that still describes the pre-collapse model.

- Check the current utility: Ask what the token does now. Staking, governance, and fees are different from stablecoin defense mechanisms.

- Examine governance risk: A proof-of-stake chain still carries validator, treasury, and proposal risk even without the old UST design.

- Be cautious with custody: If you use ecosystem tools such as Terra Station or other supported wallets, treat self-custody as an operational responsibility, not a convenience feature.

- Pressure-test the pitch: If a project depends on sustained optimism, one dominant app, or unclear token demand, slow down.

- Study the downside first: A practical guide on how to avoid crypto scams pairs well with Terra's history because many losses in crypto start with weak due diligence, not just malicious fraud.

The deeper lesson goes beyond Terra. In DeFi, the most dangerous risk often hides inside the mechanism users describe as novel.

If you want more grounded crypto analysis, beginner-friendly explainers, and deeper breakdowns of Web3, DeFi, tokenomics, and market risk, visit Coiner Blog. It's a useful place to keep learning without losing sight of the practical side of crypto.