Cryptocurrency ramblings

What Is Arbitrage Trading: 2026 Crypto Profits Guide

You open two trading apps and spot the same coin at slightly different prices. One screen shows a cheaper market. The other shows a richer one. At first glance, it looks like free money.

That moment hooks a lot of people into crypto arbitrage.

It also misleads them.

In theory, arbitrage looks simple. Buy where the asset is cheaper, sell where it's more expensive, do both fast, collect the spread. In practice, crypto adds friction everywhere. Centralized exchanges have different order books, withdrawal policies, and fee schedules. DeFi adds gas, smart contract routing, MEV pressure, and liquidity depth issues. Cross-chain transfers can stall. A spread that looks attractive on your screen can disappear before your second leg fills.

That's why what is arbitrage trading is the wrong beginner question if you stop at the textbook definition. The better question is whether the spread survives contact with reality.

Crypto is a perfect environment for this discussion because it's fragmented, global, always on, and full of separate liquidity pools. Those conditions create price gaps. They also punish sloppy execution. If you've been watching exchange prices drift apart and wondering whether that “glitch” is tradable, you're looking at the same problem pros stare at all day.

Table of Contents

- Introduction The Glitch in Crypto's Price Matrix

- The Core Concept of Arbitrage Trading

- Key Types of Crypto Arbitrage with Examples

- The Mechanics of a Crypto Arbitrage Trade

- What Makes Crypto Arbitrage Profitable

- Popular Arbitrage Strategies and Tools

- The Real Risks of Crypto Arbitrage and Next Steps

Introduction The Glitch in Crypto's Price Matrix

A lot of traders first notice arbitrage by accident. You check Bitcoin on one exchange, flip to another tab, and the price doesn't match. The gap may be small, but it's enough to make you think the market is broken.

It isn't broken. It's fragmented.

Crypto trades across centralized exchanges, decentralized exchanges, Layer 2 networks, perpetual venues, and bridge-connected ecosystems that don't always sync instantly. Each venue has its own liquidity, user flow, and matching mechanics. If you want a cleaner feel for why those differences matter, it helps to understand the liquidity of cryptocurrency markets before assuming every visible spread is tradable.

Arbitrage has been around far longer than crypto. Scholarly work describes it as one of the oldest ideas in finance and commerce, with opportunities existing even in ancient trade through the movement of goods across long distances, while modern fragmented markets make those gaps tiny and fleeting enough that traders lean on speed, low fees, and automation (historical overview of arbitrage development).

That old logic fits Web3 surprisingly well. In earlier markets, traders moved goods. In crypto, traders move capital, inventory, and information across exchanges, DEX pools, and chains. The principle hasn't changed. The infrastructure has.

Why identical assets drift apart

On paper, a token should trade at the same value everywhere. In live markets, that rarely holds for long. One exchange may have a wave of aggressive buyers. Another may have thin books. A DEX pool may be temporarily skewed by a large swap. A bridge delay may isolate one side of the market.

These dislocations are the “glitches” arbitrageurs hunt.

Arbitrage is less about predicting where a coin will go next and more about spotting when two venues disagree right now.

The appeal and the trap

Beginners tend to get overconfident. They see a discrepancy and assume the market is handing them a spread. Veterans know the visible gap is only the first checkpoint.

A real arbitrage setup has to survive fees, slippage, latency, transfer constraints, and liquidity limits. In crypto, especially across DeFi and CEXs, the spread can look healthy on a chart and still be worthless by execution time.

The Core Concept of Arbitrage Trading

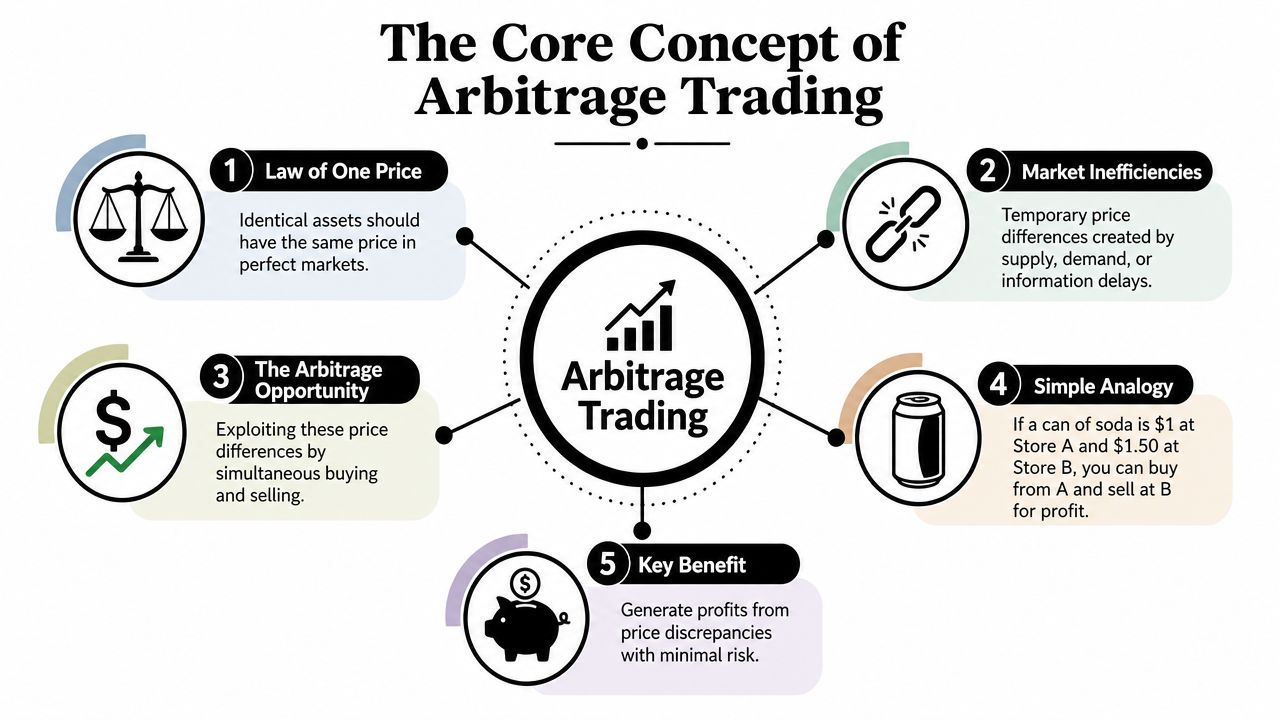

Arbitrage trading starts with a simple economic idea. If the same thing is sold in two places, it shouldn't keep carrying two different prices forever.

A basic analogy works better than most finance jargon. If a can of soda is cheaper in Store A and more expensive in Store B, a trader can buy from A and sell to B. The opportunity exists because the same item is priced inconsistently. In efficient markets, traders keep exploiting that mismatch until the prices move closer together.

Why identical assets drift apart

Finance formalizes that idea through the law of one price. If identical assets trade at different prices, arbitrageurs buy the cheaper one and sell the more expensive one until the spread narrows. The key detail is that simultaneous execution is central to the definition, which is why arbitrage is not the same as buying low and hoping to sell higher later (law of one price and simultaneous execution).

In crypto, this gets more interesting because the market isn't one market. It's a patchwork of order books, AMMs, bridges, Layer 2s, and smart contract venues. That fragmentation creates more mismatches than many traditional markets, but it also creates more ways to lose the edge.

If you've spent time reading about MEV, you've already seen a related version of this battle for price discrepancies and transaction ordering in this guide to what MEV is.

What counts as real arbitrage

The cleanest definition is this: you buy the asset where it's cheap and sell the same or closely related asset where it's expensive, with both legs tied together tightly enough that you're targeting the spread, not the market's future direction.

That distinction matters. A lot of people say they're doing arbitrage when they're speculating. If you buy on one exchange and wait to transfer before selling later, you've added market exposure. You might still profit, but you're no longer in pure textbook arbitrage.

Here's the practical filter traders use:

- Same asset or close substitute: The instruments must be close enough that the spread is meaningful.

- Near-simultaneous execution: Both sides have to happen together, or close enough that market risk stays limited.

- Spread-focused profit goal: The trade wins because the price gap exists, not because the asset trends upward.

- Post-cost viability: The edge must remain after every fee and execution drag.

Practical rule: If your trade thesis depends on “the price should still be there when my transfer clears,” you've already moved away from pure arbitrage and toward a riskier convergence bet.

That's the conceptual backbone. Everything else in crypto arbitrage is execution.

Key Types of Crypto Arbitrage with Examples

Crypto traders usually run into three broad arbitrage styles. They sound similar on the surface, but the mechanics differ a lot. One lives across exchanges, one lives inside a single venue, and one lives inside DeFi's smart contract maze.

Spatial arbitrage across exchanges

This is often the first version that comes to mind. A token trades lower on one centralized exchange and higher on another. The trader buys on the cheaper venue and sells on the more expensive one.

A simple example helps. Suppose ETH appears cheaper on Exchange A and richer on Exchange B at the same moment. The theoretical trade is obvious: buy on A, sell on B, and capture the spread. The main difficulty is inventory management. If you need to move coins or stablecoins between venues after opening the trade, the delay can wipe out the edge.

This is why better operators often pre-fund both exchanges. They keep stablecoins on one side and the asset on the other so they can hit both legs immediately, then rebalance later when conditions are calmer.

Triangular arbitrage inside one venue

Triangular arbitrage stays on one exchange and works through three related trading pairs. Instead of comparing two venues, you compare the implied prices across pairs.

For example, a trader might cycle through BTC/USDT, ETH/BTC, and ETH/USDT. If the math implied by the first two pairs doesn't line up with the direct ETH/USDT market, the loop may offer a spread. This style avoids cross-exchange transfer risk, which is a major advantage.

Its downside is competition. On liquid venues, these inefficiencies don't stay open long. Bots chew through them fast.

DeFi arbitrage across pools and protocols

DeFi arbitrage is where the space gets both creative and unforgiving. You might see the same token priced differently on Uniswap, Curve, Balancer, or a DEX aggregator route. A trader can buy from the cheaper liquidity pool and sell into the richer one, often in a single atomic transaction if the setup allows it.

That atomic nature is powerful. If the full trade can't execute profitably, the transaction can fail rather than leaving you half-exposed. This is one reason DeFi attracts advanced arbitrage systems and MEV searchers.

Still, DeFi adds its own killers:

- Gas costs: A profitable idea on paper can die on-chain if network fees spike.

- Pool depth: AMM pricing changes as you trade through liquidity.

- Routing complexity: The best route may involve multiple pools and smart contracts.

- Competition: If another bot lands first, your expected spread may vanish.

For traders comparing approaches, crypto trading strategy comparisons can help frame where arbitrage fits relative to momentum, swing trading, and market making.

Crypto Arbitrage Types Compared

| Arbitrage Type | Mechanic | Example | Complexity | Key Requirement |

|---|---|---|---|---|

| Spatial arbitrage | Buy on one exchange and sell on another | Token cheaper on one CEX and richer on another | Medium | Fast execution and funded accounts on multiple venues |

| Triangular arbitrage | Exploit pricing inconsistency across three pairs on one venue | Cycling through BTC, ETH, and a stablecoin pair | High | Fast calculation and order placement |

| DeFi arbitrage | Trade between mispriced pools or routes across protocols | Buying from one DEX pool and selling into another | High | Gas awareness, smart contract tooling, and route optimization |

The best arbitrage style isn't the one that looks smartest on paper. It's the one you can execute reliably with your capital, tooling, and risk controls.

The Mechanics of a Crypto Arbitrage Trade

A trader spots ETH at a better price on one venue and a richer price on another. On paper, the spread looks clean. In practice, that trade only works if both legs fill at the expected price, the fees stay under control, and the window stays open long enough to finish the job.

That gap between a visible spread and a bankable spread is where arbitrage lives or dies.

Arbitrage is a spread-capture strategy. The spread only matters after every friction is paid for, including trading fees, network costs, transfer costs, taxes, and the price impact of your own order. The hard part is rarely spotting a mismatch. The hard part is confirming that the spread remains positive after execution costs, as explained in this overview of arbitrage trading mechanics.

The quote is only the starting point

On a centralized exchange, the price you notice is usually the best bid or ask for a small amount. If your size is larger, your order can sweep through multiple levels of the book and your average fill gets worse. On a DEX, the same problem shows up through pool depth and AMM pricing curves. A shallow pool can make a good-looking route useless the moment real size hits it.

That is why experienced arbitrage traders do not treat the top-line quote as profit. They treat it as a clue.

The cost stack adds up fast:

- Trading fees: Maker and taker fees can erase a thin edge immediately.

- Withdrawal and network costs: These matter any time capital or collateral has to move.

- Bid-ask spread: You pay it before the trade has a chance to work.

- Execution impact: Larger orders often get worse average pricing than the headline quote suggests.

A spread that works at test size can fail badly at real size.

Timing risk breaks many "easy" trades

A common beginner mistake is buying on Exchange A, sending the asset to Exchange B, and expecting the higher price to still be there on arrival. That can work in slow conditions. In crypto, slow conditions do not last long.

One burst of volatility can wipe out the spread before the transfer clears. The same thing happens on-chain. A route can look profitable when quoted, then lose money by the time the transaction lands because gas jumped, another bot took the pool first, or the pool state changed mid-block.

The practical fix is usually inventory management, not hope. Serious traders keep funds pre-positioned across multiple exchanges, wallets, and networks so they can execute both legs quickly instead of waiting on transfers. They also set minimum profit thresholds high enough to survive normal execution noise.

A simple process keeps the trade grounded:

- Check executable liquidity: Look past the first quote and estimate your real average fill.

- Price the full trade: Include exchange fees, gas, withdrawal costs, and any transfer expense.

- Map the exit before entry: If the second leg is uncertain, the trade is weak from the start.

- Use pre-funded inventory where possible: Rebalancing later is usually safer than chasing a live spread with a transfer.

- Set a kill threshold: If the edge falls below your minimum expected profit, do nothing.

To see how automation changes this workflow, the following video gives useful context on execution logic and bot-driven trading.

Why execution infrastructure matters

Manual trading is still useful for learning how spreads appear and disappear. It is a poor way to compete for them consistently. By the time a human compares venues, sizes the order, and clicks both legs, the market often has already moved.

That is why serious operators build around speed and process. They watch multiple venues at once, pre-calculate fees, track wallet balances, and automate route selection. Traders comparing software often start with lists of AI crypto trading bots for faster crypto execution, not because bots print money, but because small, short-lived spreads reward fast systems and punish hesitation.

In crypto arbitrage, the mechanics are the strategy. If execution is sloppy, the edge was never real.

What Makes Crypto Arbitrage Profitable

If you strip away the hype, profitable arbitrage rests on three things: speed, volume, and cost efficiency. Miss one, and the strategy turns from elegant to frustrating very quickly.

Speed beats theory

Crypto price gaps don't stay open because traders are lazy. They stay open briefly because markets are fragmented and participants react at different speeds. The trader who sees the spread first still loses if the order takes too long to hit.

This is why profitable arbitrage often looks less like prediction and more like engineering. Fast data feeds, low-latency execution, and pre-positioned inventory matter more than having a clever opinion on tokenomics or market sentiment.

That's also why AI is starting to matter in the workflow. Not because it creates magical edges, but because it can help with pattern detection, route selection, execution timing, and exception handling across multiple venues. In crypto, AI plus automation is often an operations advantage.

Volume only helps when liquidity is real

Tiny spreads usually need size to become worth the effort. But more size only helps if the market can absorb it. If the order book is thin or the DeFi pool is shallow, larger orders create their own slippage and destroy the opportunity.

That makes capital deployment a balancing act. Traders need enough inventory across exchanges, stablecoin rails, and wallets to move quickly, but not so much that they become stuck with idle balances or venue exposure they don't want.

Bigger size doesn't automatically mean bigger arbitrage profits. If your own order moves the market, you're paying yourself with one hand and taking it back with the other.

Cost efficiency decides the outcome

Layer 2 networks become important. On Ethereum mainnet, some smaller DeFi opportunities never survive fees. On lower-cost execution environments, the same logic can become practical. That's one reason Layer 2 ecosystems matter for retail and semi-professional arbitrage. Lower transaction drag widens the set of trades worth considering.

A profitable setup usually shares a few traits:

- Pre-funded capital: You don't want to wait for deposits every time a spread appears.

- Cheap execution paths: Lower fees and efficient routes protect thin edges.

- Reliable liquidity access: Centralized books, DEX aggregators, and Layer 2 pools all matter.

- Strict trade filtering: Good systems reject marginal trades instead of forcing action.

Volatility cuts both ways here. It creates dislocations, which is good. It also increases fill risk, spread instability, and routing uncertainty, which is not. The best arbitrage traders aren't chasing every gap. They're filtering for the few that remain attractive after all the noise is stripped out.

Popular Arbitrage Strategies and Tools

A spread appears for six seconds. By the time a manual trader clicks through two tabs, checks size, and signs a wallet transaction, it is gone. That is the critical starting point for tool selection in crypto arbitrage. The question is not whether a price gap exists. The question is whether your setup can capture it before fees, latency, and routing friction erase it.

Manual monitoring still matters because it teaches pattern recognition. Traders who start by comparing exchange quotes, DEX prices, and token liquidity learn a hard lesson early. Plenty of visible spreads are fake opportunities once you factor in execution. A dashboard can show a gap between Binance and a Uniswap pool, but the pool may only support a fraction of your intended size before the quote deteriorates.

A practical manual workflow usually includes a few pieces:

- Price comparison dashboards: Fast for spotting cross-venue dislocations.

- Exchange watchlists: Useful for following pairs that frequently drift out of line.

- DEX aggregators: Better than reading one pool in isolation because routing changes the actual fill.

- Inventory tracking: Necessary if capital is split across wallets, chains, and centralized exchanges.

Manual trading is training, not a long-term edge in crowded pairs.

Automation is what turns arbitrage from observation into execution. Bots watch order books, pool states, gas costs, and route changes at the same time. Trading terminals help with centralized venue coverage, but DeFi often demands another layer of tooling because the best route is rarely the most obvious one. Aggregators such as 1inch and Matcha help traders compare paths across pools, while custom bots decide whether the spread survives after gas, expected slippage, and failed transaction risk.

The tool stack usually looks like this:

| Tool Category | Best Use | Weakness |

|---|---|---|

| Manual price trackers | Learning market behavior and screening simple spreads | Too slow for many live opportunities |

| Trading terminals | Managing orders across several CEXs | Quality depends on exchange support, latency, and order routing |

| Arbitrage bots | Executing rule-based trades at speed | Requires monitoring, tuning, and strict risk controls |

| DEX aggregators | Finding better on-chain routes | Gas costs, MEV, and pool depth can still wreck the trade |

Good traders combine tools instead of searching for one perfect platform. A terminal may handle the CEX leg, an aggregator may price the DeFi leg, and a bot may decide whether the net edge is still there. Traders building that kind of logic can get useful ideas from Finzer algorithmic trading insights, especially around rule design and execution discipline.

One tool deserves more attention than beginners usually give it. Slippage controls decide whether a trade closes near the quoted edge or bleeds it away during execution. If you need a sharper explanation of how that friction works, this guide to what slippage in trading means for execution quality is the right place to start.

Good arbitrage tooling does one job well. It helps traders reject bad spreads faster and execute the rare good ones before the market corrects itself.

The Real Risks of Crypto Arbitrage and Next Steps

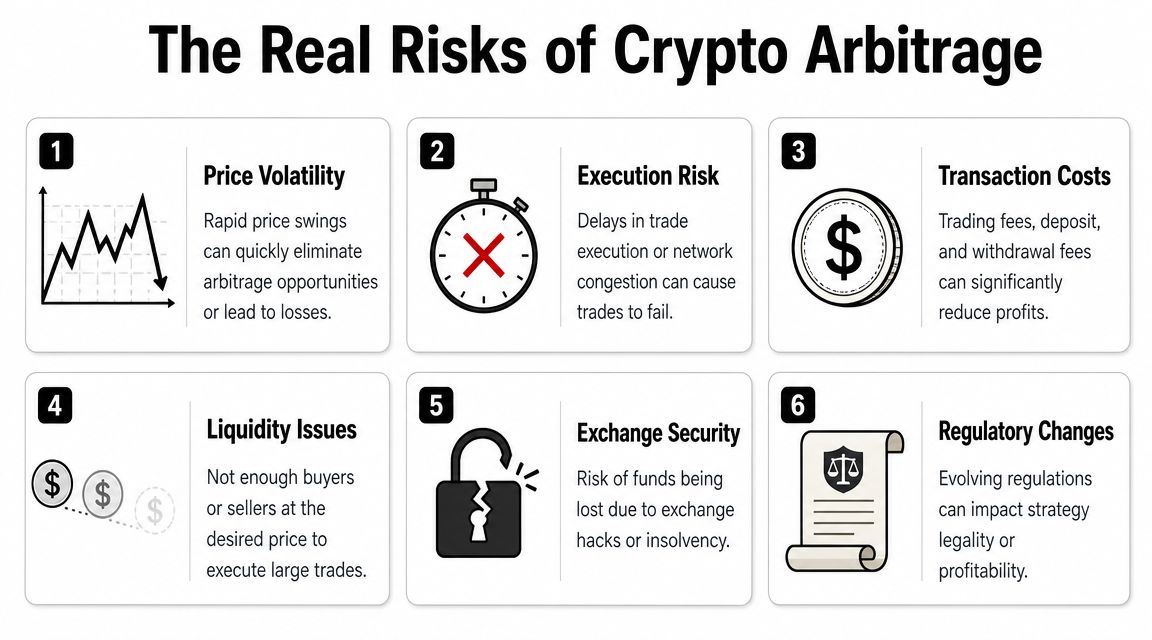

The phrase “risk-free arbitrage” survives because the theory is neat. Crypto reality is not.

Mainstream crypto explainers note that arbitrage is not entirely risk-free in practice because traders still face execution risk, liquidity risk, transfer delays, and fee or slippage drag. The important question isn't what arbitrage is in theory, but when it still works after costs (crypto arbitrage risk in practice).

Why risk-free is the wrong mental model

Execution risk hits first. You buy the cheap leg, but the expensive leg moves before you sell. Liquidity risk shows up when the market looks tradable at the top level but can't absorb your real size. Counterparty risk enters when a centralized exchange slows withdrawals, changes rules, or suffers operational stress.

Then come the external constraints. Tax treatment can complicate high-frequency trading. Regulations can shift. Smart contract risk exists in DeFi. Bridge risk exists across chains. None of those problems care that the spread looked clean in a spreadsheet.

Practical next steps before you trade

If you're serious about exploring arbitrage, don't start by firing capital at the first discrepancy you see. Start by building process.

A sensible path looks like this:

- Track spreads without trading: Watch how often they vanish before you could realistically execute.

- Paper trade your logic: Simulate entries, exits, fees, and transfers.

- Map every cost: Include gas, exchange fees, and rebalancing friction.

- Study risk management: Resources on how to protect your trading capital are more useful at this stage than another list of “top arbitrage coins.”

- Start small if you go live: The first goal is operational competence, not aggressive returns.

Crypto arbitrage still matters even if most traders never run it professionally. It helps prices converge across fragmented venues. It exposes where liquidity is weak. It teaches you how markets function under stress. That alone makes it worth understanding.

If you want more grounded crypto analysis without the usual fluff, explore Coiner Blog. It's a strong place to follow practical guides on DeFi, Web3, Layer 2s, tokenomics, AI and crypto, plus the underlying mechanics behind trading and blockchain markets.

1 Comment