Cryptocurrency ramblings

What Is MEV: Understanding Maximal Extractable Value

You swap on a DEX, approve the transaction, and the quote looks fine. A few seconds later the trade lands at a worse price, the pool moved against you, and someone else seems to have captured the spread with suspicious timing. That gap often gets filed under “slippage,” but for active DeFi users it's often something more specific.

That hidden layer is MEV, short for Maximal Extractable Value. If you've spent time in Ethereum, Layer 2s, on-chain perps, or token launches, you've already felt it. MEV is the invisible game around transaction ordering, where bots, builders, and validators compete to profit from what lands before your trade, after your trade, or instead of your trade.

For traders, MEV can feel like an execution tax. For developers, it's a market-structure problem. For Web3 itself, it sits at the intersection of blockchain transparency, validator incentives, DeFi design, and fairness.

Table of Contents

- The Slippery World of DeFi Trading

- What Is MEV Really

- The MEV Supply Chain Players and Roles

- Real-World MEV Examples Good Bad and Ugly

- The High Stakes Economic Impact of MEV

- Fighting Back How to Mitigate MEV

- The Future of MEV L2s AI and Beyond

The Slippery World of DeFi Trading

A common DeFi mistake isn't picking the wrong token. It's assuming the quoted price is the price you'll get.

Say you place a swap on a volatile pair during a busy market window. You allow generous slippage because you don't want the transaction to fail. The trade confirms, but the fill is worse than expected. You didn't misclick. You just entered the public arena where every pending transaction can attract attention.

Many users first meet MEV without knowing the term. They call it bad luck, bot activity, or a rough fill. In practice, it's often the result of a public mempool exposing your intent before the block is finalized. Once your order is visible, specialized actors can react before you do.

Why the mempool feels like a dark forest

The “dark forest” analogy still works because it captures the lived experience of on-chain trading. You broadcast a transaction into a transparent environment, and unseen participants scan that environment for profitable moves. If your order creates an opportunity, someone may try to capture it.

That's why understanding market depth matters just as much as reading a token chart. Thin liquidity and wide slippage settings make a trade easier to exploit. If you want a practical refresher on how pool depth changes execution quality, this guide to crypto liquidity and why it matters for trading is useful context.

MEV isn't some side quest in DeFi. It's part of how execution works on transparent blockchains.

For traders, the question isn't only “What is MEV?” It's “When does my order become prey?” Large swaps, fast-moving assets, token launches, and stressed liquidity are the obvious danger zones. But even ordinary swaps can leak value when order flow is public and competitive bots are active.

That's why MEV deserves attention now. It sits underneath DeFi growth, Layer 2 scaling, tokenized real-world assets, and AI-assisted trading systems. More on-chain activity means more visible intent, and visible intent is where the MEV game starts.

What Is MEV Really

A simple definition that actually helps

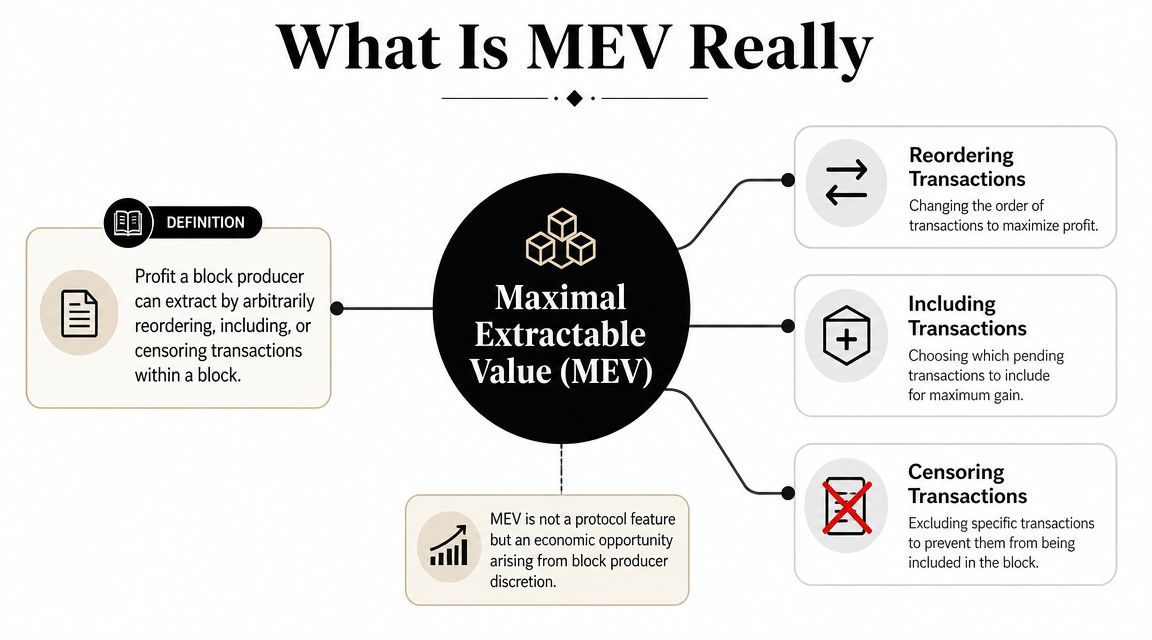

MEV is the profit a block producer can extract by choosing how transactions are ordered, included, or excluded inside a block. That's the clean definition, but it becomes easier when you picture a newspaper editor deciding which stories run first on the front page. The editor controls placement. In blockchains, that placement power can create profit.

This is why “what is MEV” is really a question about ordering rights. The blockchain doesn't just record transactions. Someone decides sequence, and sequence changes outcomes in DeFi. On an AMM, one trade moves price for the next. On a lending protocol, one liquidation can happen before another. On a mint or token launch, early placement can mean the difference between profit and a miss.

If you want the underlying system basics behind blocks, validators, and transaction flow, it helps to revisit blockchain technology basics.

A useful way to think about MEV is this:

| Mechanism | What happens | Who benefits |

|---|---|---|

| Reordering | A transaction gets moved ahead of or behind another | Searchers, builders, proposers |

| Including | A profitable transaction or bundle gets inserted into a block | Actors who found the opportunity |

| Excluding | A transaction is delayed or left out | Actors who gain from that delay |

The scale is not trivial. The Chainlink education overview of MEV notes that the Bank for International Settlements estimated total MEV volume at roughly $550 million to $650 million since 2020, and that after Ethereum's move to proof of stake, Flashbots data showed realized extractable value on Ethereum at 526,207 ETH between September 2022 and early June 2025.

A short explainer helps if you want another visual pass on the concept.

Why the name changed from miner to maximal

Originally, people called it Miner Extractable Value because miners controlled block ordering in proof-of-work systems. Ethereum's transition to proof of stake in September 2022 changed the cast. Validators, builders, and other block producers now shape transaction ordering, so the term broadened to Maximal Extractable Value.

That change matters because it tells you MEV isn't tied to one consensus era. It's a property of any blockchain system where someone can profit from sequencing transactions. The mechanism survives architecture changes. The actors change. The incentives remain.

Practical rule: If a chain has transparent pending order flow and someone controls ordering, MEV will exist in some form.

The MEV Supply Chain Players and Roles

Who does what inside the block auction

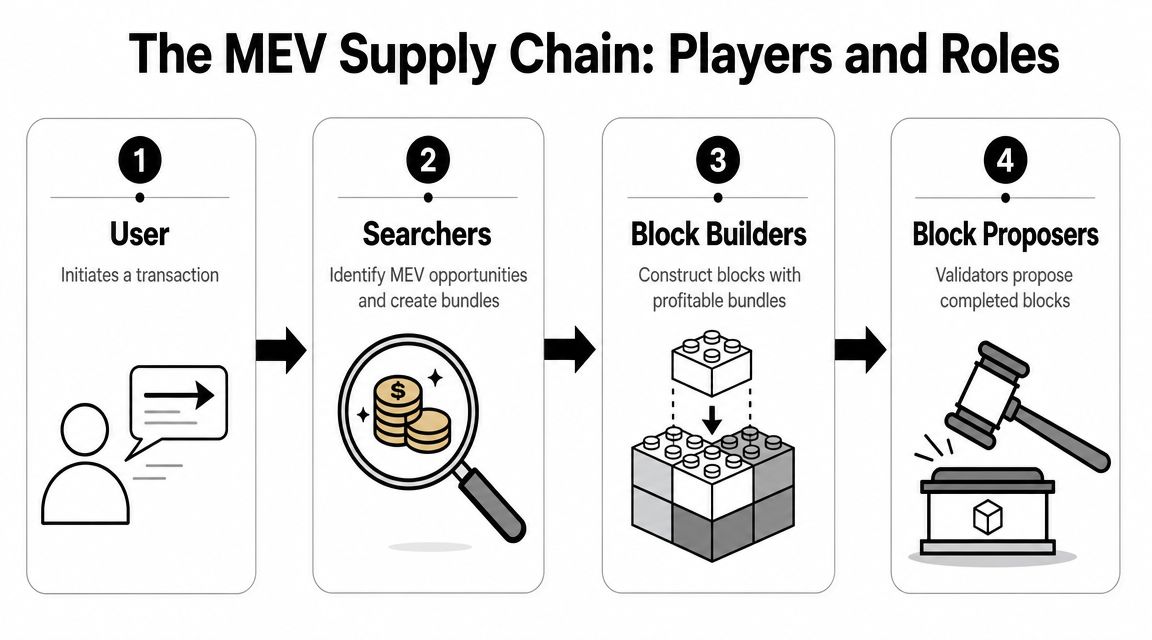

MEV sounds abstract until you see the assembly line. A user submits a transaction. Then several specialized actors start working around it.

Searchers are the hunters. They scan pending transactions and state changes for profit opportunities such as arbitrage, liquidations, or sandwich setups. In practice, these are usually automated systems, not humans clicking buttons.

Builders take raw transaction opportunities and package them into optimized blocks. Their job is to produce the most profitable block they can, often by combining ordinary user transactions with searcher bundles.

Relayers act as intermediaries in some workflows. They pass block data between builders and validators, helping coordinate the market for blocks without exposing every detail to every participant.

Proposers, which in Ethereum are validators, pick the block and commit it to the chain. They sit at the final checkpoint. Without proposer acceptance, the opportunity doesn't become on-chain profit.

Why this became a business, not just a bot trick

This supply chain exists because DeFi created repeatable, machine-readable opportunities. Arbitrage across pools. Liquidations in lending markets. Price gaps between venues. These aren't rare events. They're structural features of smart contract markets.

The CoW Protocol explainer on MEV notes that MEV became highly lucrative as DeFi expanded, with arbitrage and liquidations as major categories. It also cites Galaxy's report that miners and operators earned about $730 million in MEV profit on Ethereum in 2021 by monitoring the mempool and using gas bidding or transaction bundles to secure profitable positions in a block.

That single fact explains why the ecosystem professionalized. Once there's meaningful revenue in ordering power, participants specialize.

Here's the flow in plain English:

A user broadcasts intent.

A swap, liquidation call, bridge transfer, or mint hits public view.Searchers model the opportunity.

They estimate whether reordering around that transaction creates profit after fees.Builders assemble a candidate block.

They rank bundles and ordinary transactions by total value.The proposer chooses the winning block.

The chain finalizes one version of reality.

The modern MEV market is less like a random pack of bots and more like a supply chain for monetizing transaction order.

That's why the topic now touches protocol design, validator economics, and even censorship concerns. As the Web3 stack matures, the invisible game gets more institutionalized.

Real-World MEV Examples Good Bad and Ugly

The ugly sandwich attack

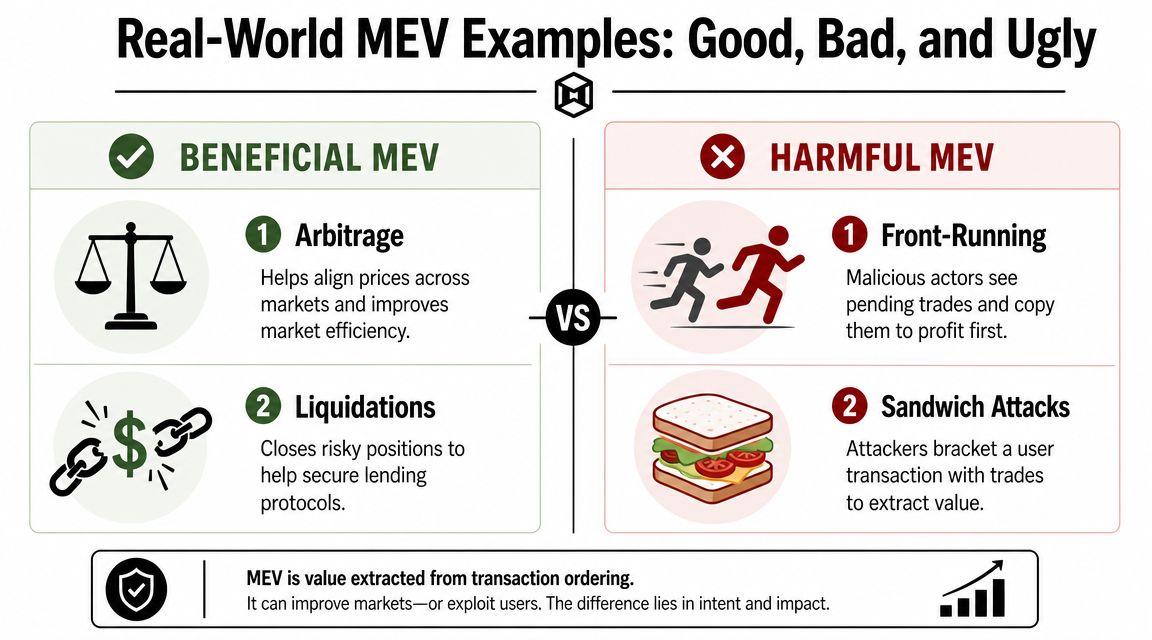

A sandwich attack is the example most traders should care about first because it directly hurts execution quality.

You submit a swap on a DEX. A searcher sees it sitting in the mempool. The bot sends one trade before yours and one after yours. The first trade pushes price against you. Your trade executes at the worse level. The second trade closes the position and captures the spread you effectively created for them.

Nothing about your wallet interface may say “you were sandwiched.” You'll just notice the fill was bad. This is why people often confuse MEV with ordinary slippage.

The CoinMarketCap glossary entry on miner extractable value describes MEV as a multi-billion-dollar phenomenon that acts like a hidden execution tax on traders. It also notes that Ethereum validators have received over $247 million in MEV-related payments since late 2020, while the actual cost often lands on users through tactics like sandwich attacks, especially on large orders with wide slippage settings.

If you trade volatile pairs often, it's worth reviewing broader crypto trading strategies and execution habits because the best setup on paper can still underperform if your entry gets picked apart in the mempool.

The bad but useful liquidation race

Liquidations feel hostile when you're on the wrong side of them, but they serve a function. In lending protocols, undercollateralized positions need to be closed so bad debt doesn't spread through the system. Searchers race to execute those liquidations because they're profitable.

That competition is still MEV, because ordering determines who captures the opportunity. It can create gas wars and uneven outcomes, but without liquidation incentives many lending systems would be less safe. This is why some MEV is harmful to users while some is tied to protocol health.

The good arbitrage loop

Arbitrage is the cleanest case for constructive MEV. Suppose the same token pair trades at meaningfully different prices across two pools or venues. A searcher buys where the asset is cheaper and sells where it's richer. The trader profits, but the ecosystem also benefits because prices converge.

That's not charity. It's still value extraction. But unlike sandwiching, arbitrage often improves market efficiency and keeps DeFi pricing tighter across venues.

A quick comparison helps:

| Type | Who usually gains | Who usually loses | Net effect |

|---|---|---|---|

| Sandwiching | Searcher and sometimes builder/proposer | The user being bracketed | Harmful execution |

| Liquidations | Liquidator | Borrower being liquidated | Maintains protocol solvency |

| Arbitrage | Arbitrageur | Slower traders or stale pools | Improves price alignment |

Not all MEV is malicious. The key distinction is whether the extraction improves market function or simply transfers value away from an unsuspecting user.

That distinction matters for both regulation and design. A blanket “ban MEV” mindset misses the fact that some on-chain markets depend on the same ordering incentives that also create user harm.

The High Stakes Economic Impact of MEV

MEV isn't only a problem for unlucky traders. It changes the economics of entire networks.

What traders actually pay

For users, the cost often shows up as a mix of worse execution, failed transactions, and the need to trade more cautiously than they otherwise would. You may split orders, tighten slippage, wait for calmer conditions, or route through specific apps just to reduce exposure. That friction is a real cost even when it doesn't appear as a line item.

This is why calling MEV a hidden execution tax is useful. It frames the issue from the trader's perspective. The loss isn't always obvious, but it changes your net outcome.

Common user-facing effects include:

- Worse fills: Public intent lets others trade around your order.

- Higher fees: Congested blockspace and bidding competition can raise execution costs.

- More conservative behavior: Users avoid size, avoid volatility, or avoid certain pools entirely.

- Reduced trust: If trading feels consistently rigged, users trade less aggressively or leave.

Why networks care about this too

At the network level, MEV can pull power toward actors with better data, better infrastructure, and tighter relationships in the block-building pipeline. That raises uncomfortable questions for decentralization.

If a small set of actors repeatedly captures the best opportunities, they gain more resources to improve their edge. Over time, that can harden into concentration around builders, validators, or infrastructure providers. It can also create incentives for transaction censorship or preferential treatment if a given order flow is more valuable than another.

A concentration dynamic appears in summarized Ethereum research discussed in the earlier Chainlink-linked material. One study cited there found that 20% of MEV operations accounted for 72% of total revenues between September 2022 and May 2023. Even without repeating the source link here, the takeaway is clear. MEV tends to cluster.

A blockchain can remain open at the protocol level while becoming economically uneven at the ordering layer.

That's why this debate now overlaps with market structure, not just DeFi mechanics. As tokenization, on-chain treasuries, AI agents, and more real-world financial activity move on-chain, transaction ordering becomes a governance and fairness issue. The chain may be neutral in theory, yet still produce systematically better outcomes for participants with the fastest path into block construction.

Fighting Back How to Mitigate MEV

The goal isn't to eliminate every form of MEV. It's to reduce the kinds that extract value from users while preserving the parts that help markets clear.

The Paradigm essay on key neutrality in base-layer markets argues that the mitigation debate has shifted toward reducing harmful extraction without breaking validator incentives. It points to defenses such as proposer-builder separation, private transaction pools, batch auctions, and stricter slippage controls.

What everyday users can do today

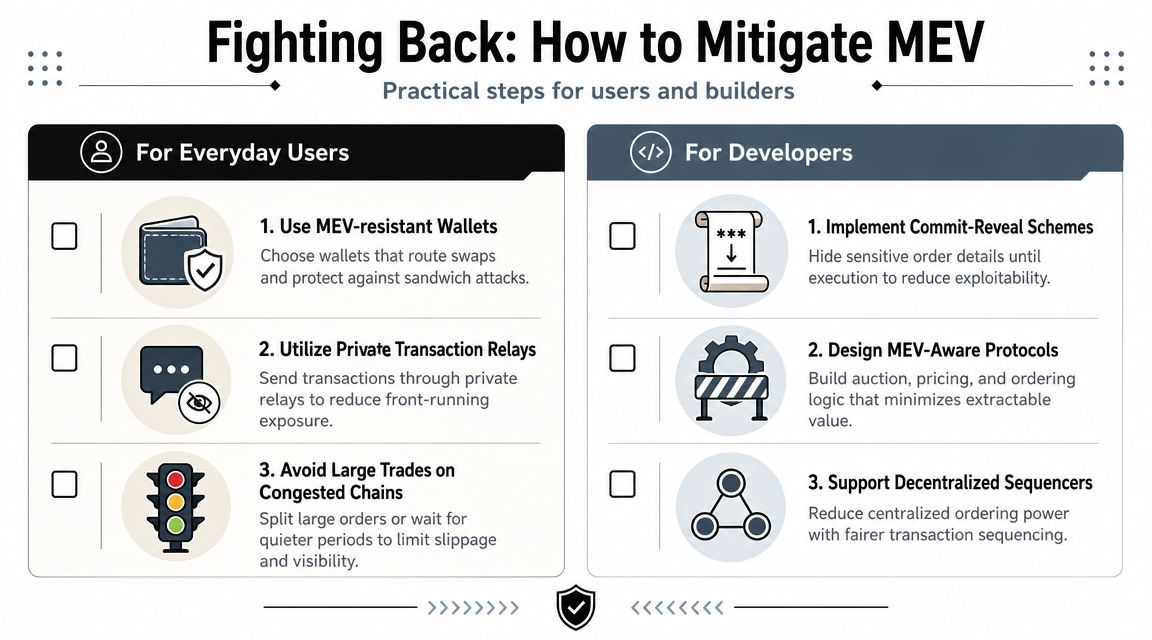

Retail users don't need to become block engineers, but they do need better habits.

- Use tighter slippage settings: Wide slippage gives searchers more room to profit from your tolerance band. If a trade only clears with very loose slippage, reconsider the trade size or venue.

- Prefer private order flow when available: Tools such as private transaction relays or wallet-level protection can reduce exposure to public mempools.

- Break up oversized trades: One large order on a thin pool is easier to target than a better-planned execution path.

- Be selective about timing: Congested periods and hype-driven launches tend to be harsher environments for ordinary users.

- Choose routing tools carefully: Some wallets, aggregators, and intent-based systems are designed to reduce visible exploitability.

A practical user checklist looks like this:

| Situation | Better move | Why it helps |

|---|---|---|

| Thin liquidity pair | Trade smaller or wait | Low depth increases impact |

| Volatile market | Tighten slippage | Reduces room for sandwiching |

| Large swap | Split execution | Lowers visibility of one big target |

| Public routing only | Seek private flow option | Reduces mempool exposure |

Small execution tweaks can matter more than a perfect token thesis. A good trade idea with poor execution is still a poor trade.

For readers who want to follow how cryptography, privacy, and protocol design may reshape this problem, Coiner Blog's coverage of the future of cryptography in blockchain systems is relevant background.

What developers and protocol teams should build

Protocol designers have more advantage than individual traders.

Some of the strongest approaches are architectural. Proposer-builder separation (PBS) aims to separate block construction from final proposal, which can reduce some centralizing pressure while still allowing a competitive block market. Private transaction pools can hide user intent before execution. Batch auctions can reduce the advantage of racing to a single visible trade. Stricter protocol-level execution rules can also limit how much value can be extracted from ordering alone.

Developers should weigh trade-offs, not slogans:

- Fairness: Does the design reduce predatory ordering?

- Censorship resistance: Does it create new trusted intermediaries?

- Latency: Does better fairness come with slower execution?

- Validator revenue: Does it remove incentives the chain still relies on?

The hardest truth is that some “MEV protection” doesn't eliminate extraction. It just moves it to a different layer, actor, or venue. Good design starts by asking which behavior you're suppressing and what replaces it.

The Future of MEV L2s AI and Beyond

MEV doesn't disappear on Layer 2

Layer 2 scaling changes MEV more than it erases it. Rollups, appchains, and alternative execution environments can reduce costs or alter sequencing rules, but they still create ordering rights somewhere in the stack. The question becomes who controls sequencing and how transparent pending order flow remains.

That matters for the next wave of Web3 applications, including tokenized real-world assets, on-chain gaming economies, and app-specific networks. If value moves on-chain, actors will compete to sequence it. For builders exploring the broader application layer, this overview of Web3 application development fits the bigger picture.

AI will likely sharpen the search game

AI and crypto are increasingly converging in analytics, agents, and automated execution. In the MEV context, better models could improve opportunity detection, routing, and cross-domain strategy selection. That likely makes searchers faster and more adaptive, not less relevant.

The deeper question is philosophical. Is MEV a bug, a necessary evil, or a legitimate feature of open markets? The honest answer is that it can be all three depending on the form it takes. Arbitrage and liquidations can help DeFi function. Sandwiching can subtly punish ordinary users. The future of MEV will turn on whether blockchain architecture can preserve open competition without letting invisible extraction define the user experience.

Coiner Blog publishes practical crypto education for readers trying to understand how blockchain mechanics affect real decisions, from DeFi execution and Layer 2 design to Web3 infrastructure, tokenomics, and emerging trends like AI-integrated crypto systems. If you want more breakdowns like this, browse Coiner Blog.

1 Comment